Record Central Bank Buying and Gold Above $4,400/oz Are Expanding Gold Project Valuations

Central banks hit a 58-year gold accumulation record in 2025, anchoring a price floor that 2026 feasibility completions are set to formally re-rate.

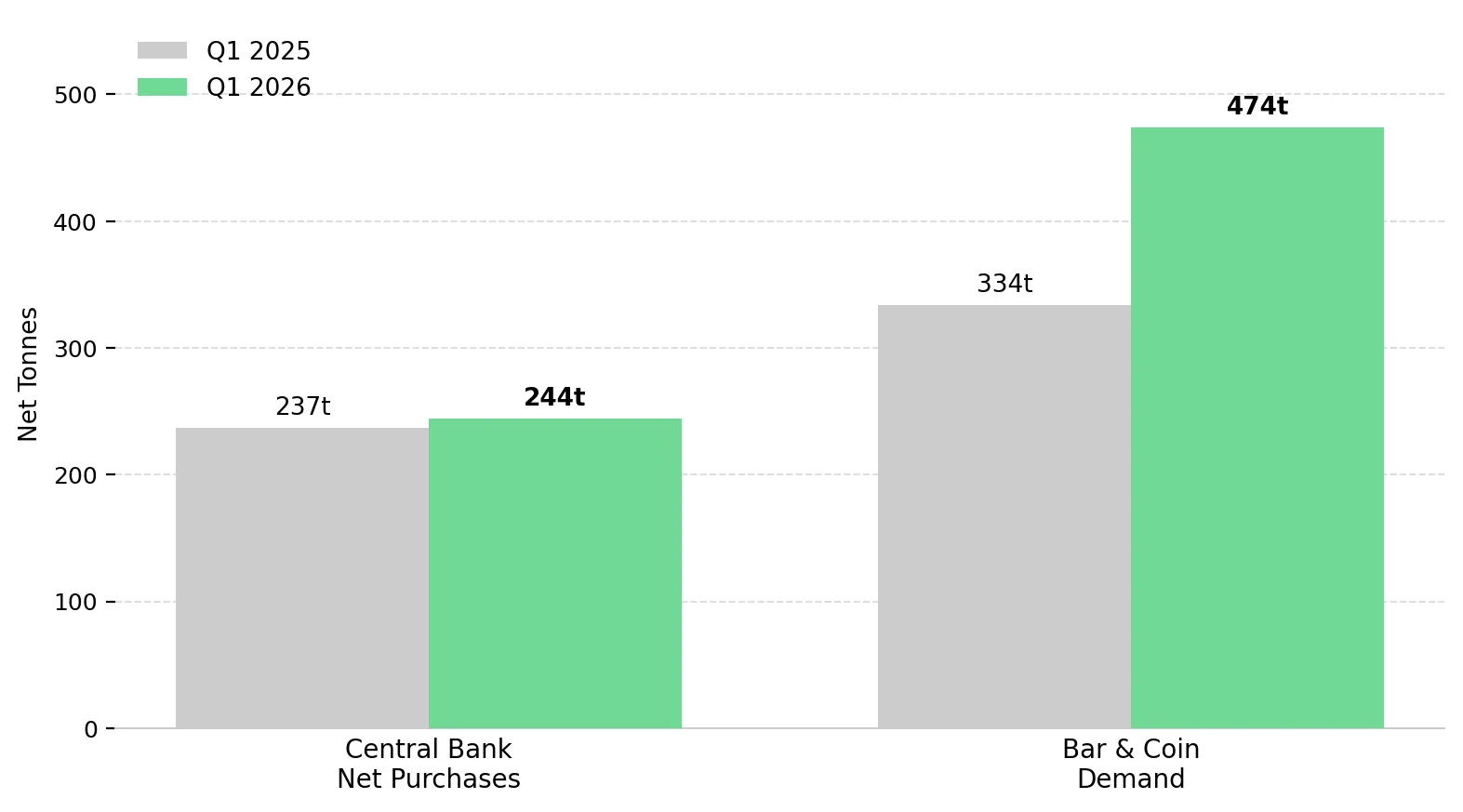

- Central banks purchased 244 tonnes of gold net in Q1 2026, exceeding the five-year quarterly average and extending the strongest sovereign buying cycle since 1967, supporting gold prices despite higher US rate expectations.

- Western gold exchange-traded funds recorded their largest quarterly outflow since 2023 in Q1 2026, while bar and coin demand rose 42% year-on-year to 474 tonnes, the second-highest quarterly total on record, indicating that physical buyers are offsetting Western investment selling.

- Development-stage gold projects publishing feasibility studies in 2026 are using $4,400 to $4,800 per ounce gold assumptions, doubling or more than doubling net present values versus prior base-case models without changing project fundamentals.

- Metallurgical confirmation of commercially viable recovery rates removes a key technical risk that has historically prevented institutional investors from funding development-stage gold projects.

- The geopolitical drivers behind sovereign gold buying are also increasing government support and investor interest in allied-nation critical minerals projects outside Chinese-controlled supply chains.

Gold's 16% Correction Has Not Weakened Sovereign & Physical Demand

Gold fell approximately 16% from its January 2026 all-time high of $5,405 per ounce to $4,483 per ounce by May 18, 2026. The decline followed an oil-price shock after the US-Iran conflict disrupted shipping through the Strait of Hormuz, pushing oil above $100 per barrel and lifting April 2026 US inflation to 3.8% year-on-year, with energy accounting for 40% of the increase. Higher inflation increases the risk of Fed rate hikes, raising the opportunity cost of holding non-yielding assets like gold.

Sovereign and physical gold demand remained strong despite the price correction. Central banks purchased 244 tonnes of gold net in Q1 2026, exceeding the five-year quarterly average, while bar and coin demand rose 42% year-on-year to 474 tonnes, supporting physical demand despite Western ETF outflows. Sustained sovereign and physical buying reduces the risk that lower Western investment demand will trigger a prolonged decline in gold prices, supporting feasibility-stage project valuations.

Sovereign & Physical Gold Demand Are Offsetting Western ETF Outflows

Central banks added more than 700 tonnes to gold reserves in 2025, the largest annual net addition since 1967, and continued buying in Q1 2026 with 244 tonnes in net purchases, up 3% year-on-year and above the five-year quarterly average. Poland, China, and Brazil remained active gold buyers between 2022 and 2026, indicating that reserve diversification is not limited to a single region or policy cycle. Gold represented approximately 2.8% of global financial assets as of Q3 2025, which JPMorgan identified as below levels consistent with diversified reserve allocations. Governments are increasing gold reserves to reduce exposure to US dollar assets that could be frozen or sanctioned during geopolitical conflicts, making sovereign gold demand less sensitive to Fed policy changes.

US-backed gold exchange-traded funds recorded their largest quarterly outflow since 2023 in Q1 2026, with March redemptions erasing January and February inflows. With the fed funds rate at 3.50% to 3.75%, higher bond yields increased the opportunity cost of holding gold, contributing to ETF outflows. Bar and coin demand rose 42% year-on-year to 474 tonnes, the second-highest quarterly total on record, led by Asian physical buyers. Total gold demand value reached a record $193 billion at an average quarterly LBMA gold price of $4,873 per ounce. Physical and sovereign buyers are providing more stable demand support for gold prices than in previous Fed-driven cycles.

Sovereign Gold Buying Is Supporting Development-Stage Project Valuations

Sustained sovereign gold buying reduces the risk that development-stage projects become uneconomic during a commodity price downturn. Projects publishing feasibility studies at $4,400 to $4,800 per ounce gold are using price assumptions that would have been considered bullish only a few years ago.

U.S. Gold Corp. CK Gold Project NPV Expansion at $4,500 Gold

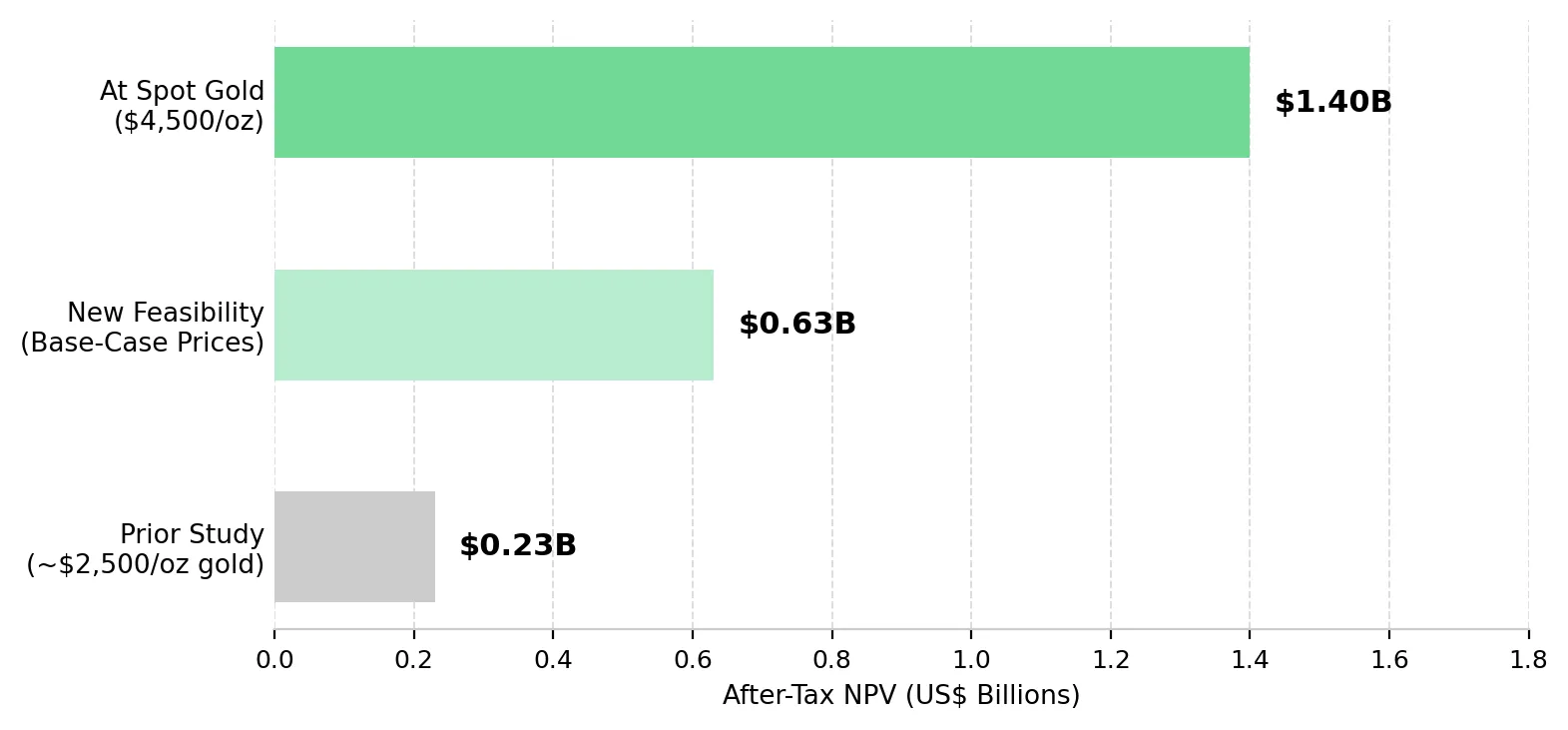

U.S. Gold Corp. reported that the March 30, 2026 S-K 1300 feasibility study for its CK Gold Project generated an after-tax NPV of $632 million at base-case metal prices and $1.30 billion at recent spot prices.

Luke Norman, Chairman of U.S. Gold Corp., quantifies the gold price sensitivity embedded in the project economics:

"Even at $4,500 gold, you are dealing with a $1.4 billion NPV and an internal rate of return of just under 50%. Realistically, $4,500 gold is where we are looking right now and below spot."

Hycroft Mining Project Economics & the Developer Valuation Gap

Hycroft Mining Holding Corporation stated that its shares trade at a 40% to 50% discount to comparable developers because the company has not yet published updated project economics. Its bulk sulfide Preliminary Economic Assessment, targeting completion in 2026, will provide updated economics for 16.4 million measured and indicated ounces of gold and 562.6 million measured and indicated ounces of silver. The company also reported $189 million in cash and no debt.

Diane Garrett, President and Chief Executive Officer of Hycroft Mining Holding Corporation, frames the infrastructure position underpinning the pending re-rating:

"We have permits for heap leach milling. The infrastructure we have on site today would cost over a billion dollars to build. Combined with being a brownfields property with so much infrastructure and permits in hand, we will start trading more in line with our peers."

Metallurgical Results Are Supporting Formal Economic Evaluation of Gold Projects

Between a resource estimate and a bankable feasibility study is proof that the ore can be processed at recovery rates that support commercial production. Until metallurgical recovery is confirmed, project economics remain unverified and many institutional investors cannot invest.

Treaty Creek Preliminary Economic Assessment & Demonstrated Project Economics

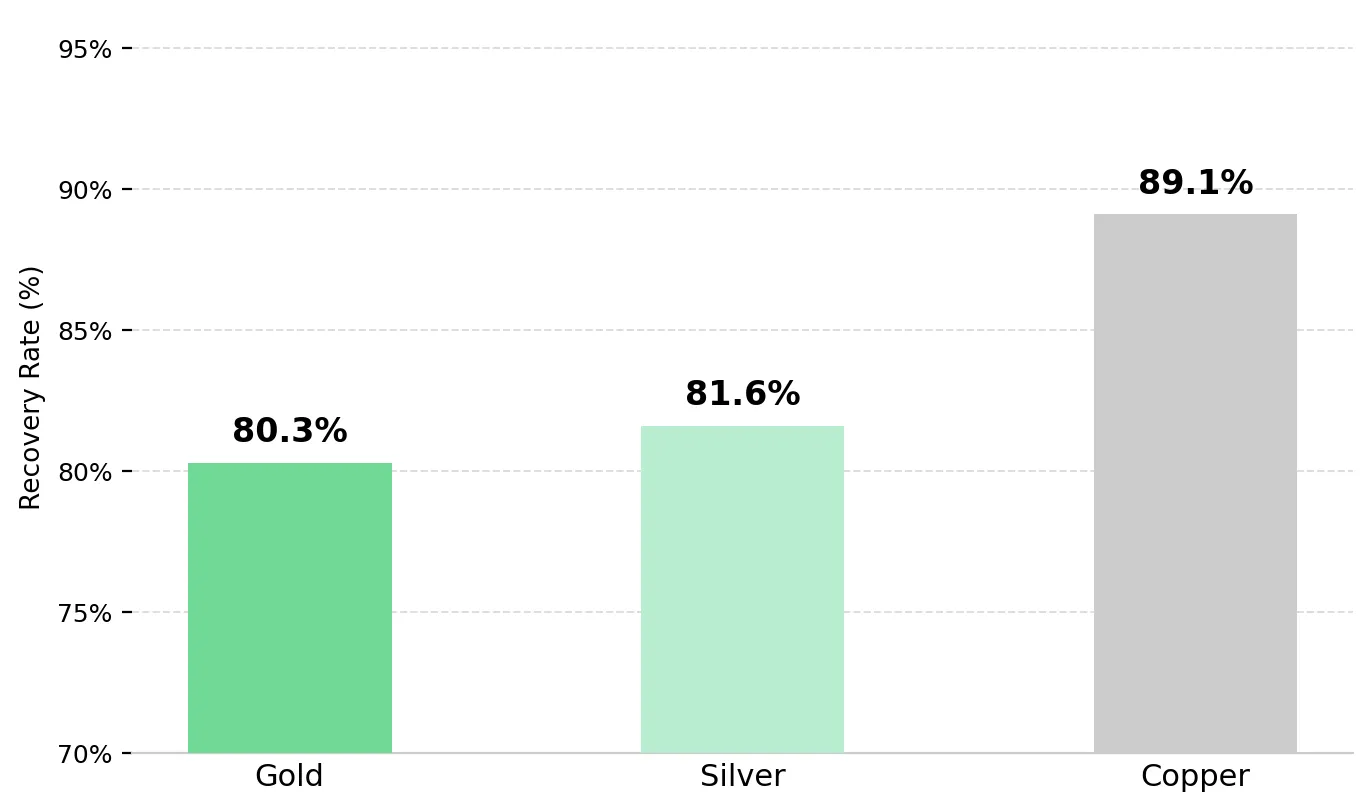

Tudor Gold’s metallurgical test results for all three zones of the Goldstorm Deposit at Treaty Creek in British Columbia's Golden Triangle, confirming recoveries under simulated processing conditions. A blended composite from all three zones returned recoveries of 80.3% gold, 81.6% silver, and 89.1% copper using conventional flotation at a 120-micron primary grind. Tudor Gold is targeting completion of a Preliminary Economic Assessment in Q3 2026 for the Treaty Creek deposit, which contains 24.9 million Indicated ounces of gold, 148.7 million ounces of silver, and 3.048 billion pounds of copper.

Joseph Ovsenek, President and Chief Executive Officer of Tudor Gold, describes what the forthcoming economic assessment will formally establish:

"The big one for us is getting that preliminary economic assessment. Show people that Treaty Creek is not just a big gold discovery, but actually it is going to be a mine. The first step on that always is getting a preliminary economic assessment completed to show there are economics here."

Sovereign Gold Demand Is Increasing the Value of High-Grade Resource Expansion

Sustained sovereign gold demand supports higher valuations for high-grade discoveries in politically stable jurisdictions. Lower downside risk for gold prices increases the value investors assign to exploration upside beyond the current audited resource base.

Queensway & Cuiú Cuiú Drilling Are Expanding Resource & Development Potential

New Found Gold reported Phase 1 open pit infill drilling results from the Queensway Gold Project in Newfoundland and Labrador, including 9.51 grams per tonne gold over 19.85 meters from 64.15 meters depth in hole NFGC-25-2618. Below-pit step-out drilling at Phase 2 Iceberg also returned 14.1 grams per tonne gold over 2.40 meters outside the current resource outline, with four drill rigs active ahead of an updated resource targeting H2 2026. Cabral Gold reported 10.2 meters grading 8.7 grams per tonne gold at Jerimum Cima in Brazil's Tapajós Region, outside the current resource base of 666,300 Indicated ounces and 525,700 Inferred ounces. The planned Phase 1 heap leach startup in Q4 2026 is the company’s key near-term development milestone

Keith Boyle, Chief Executive Officer of New Found Gold, discusses the development scenario under the company’s current studies:

"The first couple of years we are looking at about 100,000 ounces a year at an all-in sustaining cost of about $1,300. That is over $300 million of cash flow a year."

Alan Carter, President and Chief Executive Officer of Cabral Gold, describes how the initial oxide-stage project could support broader district expansion:

"What we want to do is develop an initial project to mine the near-surface oxide material. That will provide a significant amount of cash to develop the larger district, grow the global resource base within the Cuiú Cuiú district, and ultimately demonstrate the economic viability of the much larger phase two project."

Geopolitical Supply-Chain Risk Is Supporting Allied-Jurisdiction Minerals Projects

Governments increasing gold reserves are also directing capital toward mineral projects in allied jurisdictions with lower geopolitical supply-chain risk. Cobra Resources is advancing copper-gold and rare earth projects in South Australia, including the Boland Ionic Rare Earth Project and the Manihill copper project. Recent drilling at Manihill returned broad shallow copper-gold intersections, supporting the company’s view that the project may sit within a larger porphyry system. Cobra Resources is also advancing in situ recovery studies at Boland ahead of future economic evaluation.

Rupert Verco, Managing Director of Cobra Resources, outlines the economic potential emerging from recent drilling:

"We're seeing broad widths of mineralization, strong grades, and shallow intersections. From an economic standpoint, those are encouraging signs for something much larger underneath."

US Mining Jurisdictions Are Supporting Higher Developer Valuations

Bureau of Land Management permitted projects in Nevada generally receive higher valuations than comparable projects in jurisdictions with less predictable permitting timelines. Resolving permitting risk reduces development uncertainty and lowers the discount rates investors apply to future project cash flows.

Nevada Permitting & Resource Growth Are Supporting the Gabbs Feasibility Study

P2 Gold is advancing the Gabbs gold-copper project on Nevada's Walker Lane Trend toward a feasibility study targeting Q4 2026. P2 Gold is also targeting approximately $11.625 million in gross proceeds through a private placement of 15.5 million units at $0.75 per unit, including a 10 million-unit commitment from Quaternary Group Limited.

Joe Ovsenek, President and Chief Executive Officer of P2 Gold, discuss the scale of the project being evaluated in the feasibility study:

"We're advancing our Gabbs project in Nevada through feasibility. We have a strong preliminary economic assessment and are looking to increase the size of the resource base that will support that feasibility study."

The Investment Thesis for Gold

- Central banks purchased 244 tonnes of gold net in Q1 2026, above the five-year quarterly average, supporting gold prices despite higher Fed rate expectations and short-term monetary pressure.

- Developers publishing audited feasibility studies in 2026 are using $4,400 to $4,800 per ounce gold assumptions, increasing project valuations without requiring further gains in the gold price.

- Metallurgical confirmation of commercially viable recovery rates using conventional flotation reduces a key technical risk that has historically limited institutional investment in development-stage mining projects.

- Brownfields developers with cash funding, permitted infrastructure, and no production royalty in established US mining jurisdictions face lower financing risk and shorter timelines to production than greenfield projects, supporting higher project valuations.

- The geopolitical drivers supporting gold are also increasing government support for dysprosium and terbium projects in allied nations using non-Chinese supply chains and processing routes.

- Exploration-stage gold-copper developers with royalty-free projects and near-term feasibility milestones can benefit from higher gold prices without requiring immediate construction financing in a high-interest-rate environment.

Development and exploration-stage companies completing feasibility studies in 2026 are publishing project economics based on $4,400 to $4,800 per ounce gold assumptions. Those updated feasibility assumptions can materially increase project valuations. The valuation uplift does not require further gains in the gold price. It depends on audited feasibility studies, confirmed metallurgical performance, and resource bases in established mining jurisdictions.

Gold corrected to $4,483 per ounce by May 15, 2026 as energy-driven inflation reached 3.8% year-on-year, lifting CME FedWatch rate-hike expectations to 39% and increasing the opportunity cost of holding gold at a fed funds rate of 3.50% to 3.75%. These monetary pressures are shorter-term than the geopolitical drivers behind the strongest sovereign gold-buying cycle since 1967.

TL;DR

Central banks added more than 700 tonnes to gold reserves in 2025, the largest net annual addition since 1967, and extended that pace into Q1 2026 with 244 tonnes in purchases, anchoring a price floor driven by sovereign demand rather than speculative positioning. Development-stage gold projects completing feasibility studies in 2026 are entering formal economic evaluation at $4,400 to $4,800 per ounce, producing net present value uplifts of 100% or more over prior models with no change in geology or infrastructure. Metallurgical confirmation and brownfields infrastructure in Tier-1 US jurisdictions are removing the barriers that have prevented professional capital from entering development-stage positions, while the same geopolitical forces driving gold accumulation are repricing critical minerals projects in allied nations.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed