Rising Nuclear Fuel Demand & $150/lb Uranium Contracts Drive Re-Rating Across Uranium Equities

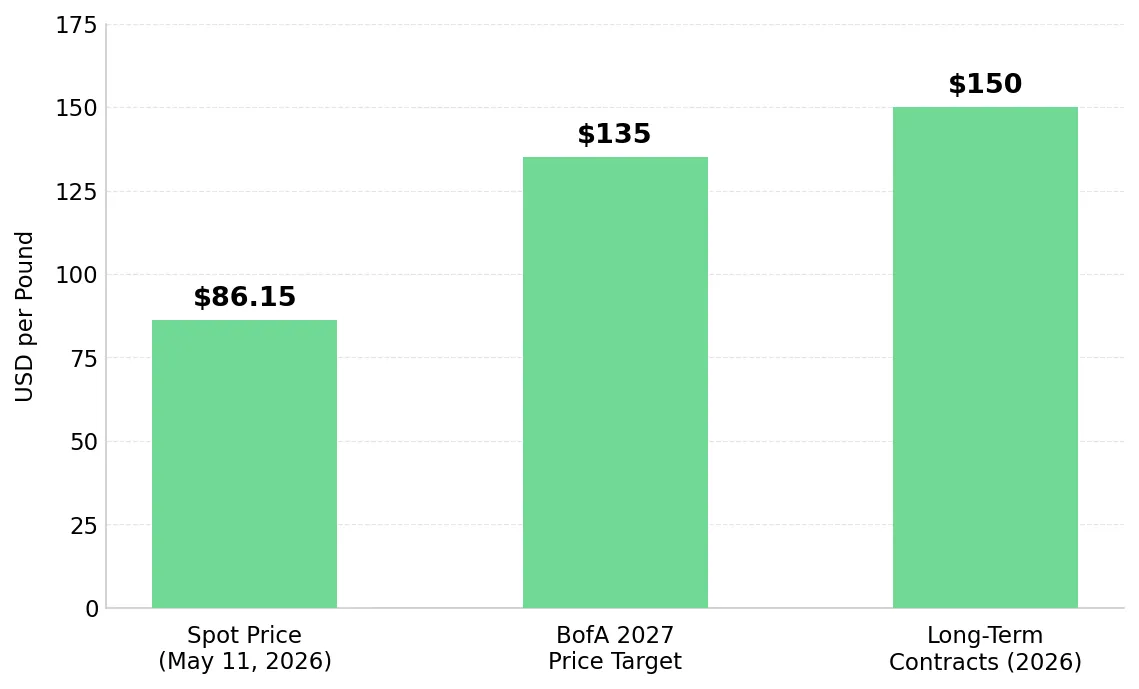

Iran's oil shock and Kazatomprom's supply cut have pushed uranium's long-term contract price to $150 per pound, $64 above spot, signaling a supply deficit.

- Iran's blockade of the Strait of Hormuz, through which roughly 20% of global oil supply flows, has been described by the International Energy Agency as the largest oil supply disruption in market history, reinforcing energy security arguments for nuclear expansion across more than 40 countries

- Kazatomprom, which controls approximately 43% of global primary uranium supply, cut its 2026 output by roughly 8 million pounds as a deliberate decision to prioritize pricing over production growth, limiting the market’s ability to respond quickly to higher uranium prices.

- Long-term uranium supply contracts are being signed at prices approaching $150 per pound against a spot price of $86.15, a $64-per-pound gap that reflects utilities securing future fuel supply amid tightening market conditions.

- The US Fed has backed nuclear expansion with a $26.5 billion Department of Energy loan to Southern Company, an 18-month cap on reactor licensing timelines, and a ban on Russian uranium imports, supporting long-term demand for domestic uranium producers.

- Uranium producers, developers, and exploration companies carry different risk and return profiles, with term uranium prices now high enough to support the economics of building new mines.

Strait of Hormuz Disruption & Accelerating Capital Flows Into Domestic Supply

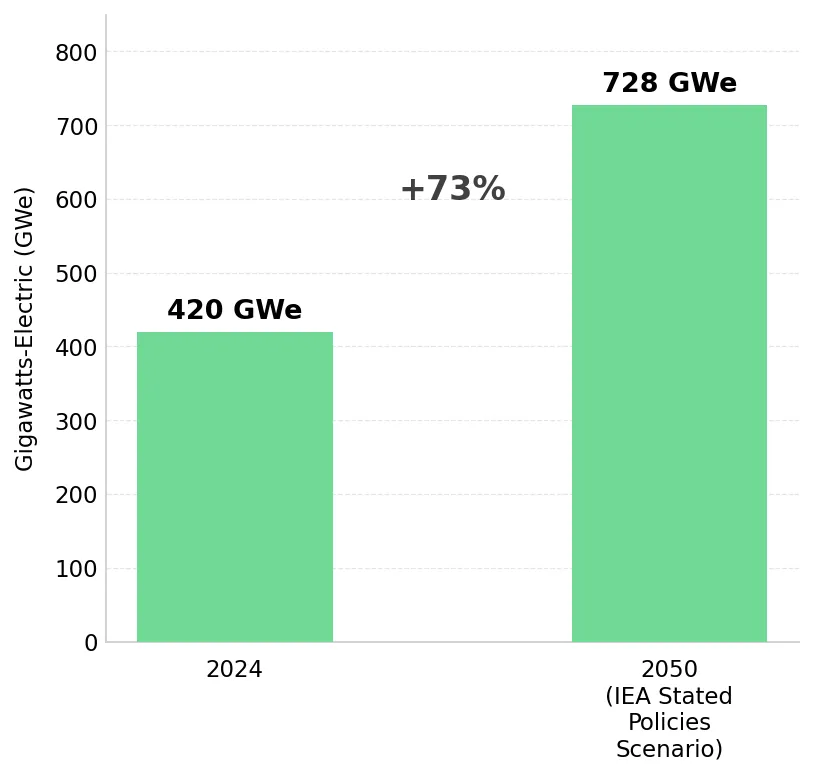

The Strait of Hormuz blockade disrupted nearly one billion barrels of oil supply, driving Brent crude above $120 per barrel and forcing QatarEnergy to suspend some delivery contracts. The IEA described the disruption as the largest supply shock in the history of the global oil market. More than 40 countries now include nuclear power in their energy strategies, with the IEA projecting global nuclear capacity to grow from 420 gigawatts in 2024 to 728 gigawatts by 2050, increasing long-term uranium demand.

For US uranium producers, import restrictions and energy security policy support stronger contract pricing for domestic supply. Mark Chalmers, former Chief Executive Officer of Energy Fuels, describes improving financing conditions for uranium producers:

“We're pushing a billion dollars of deployable capital. They see the $2 billion. They see our market cap at $5 billion. They see how strong the market is in terms of raising money right now.”

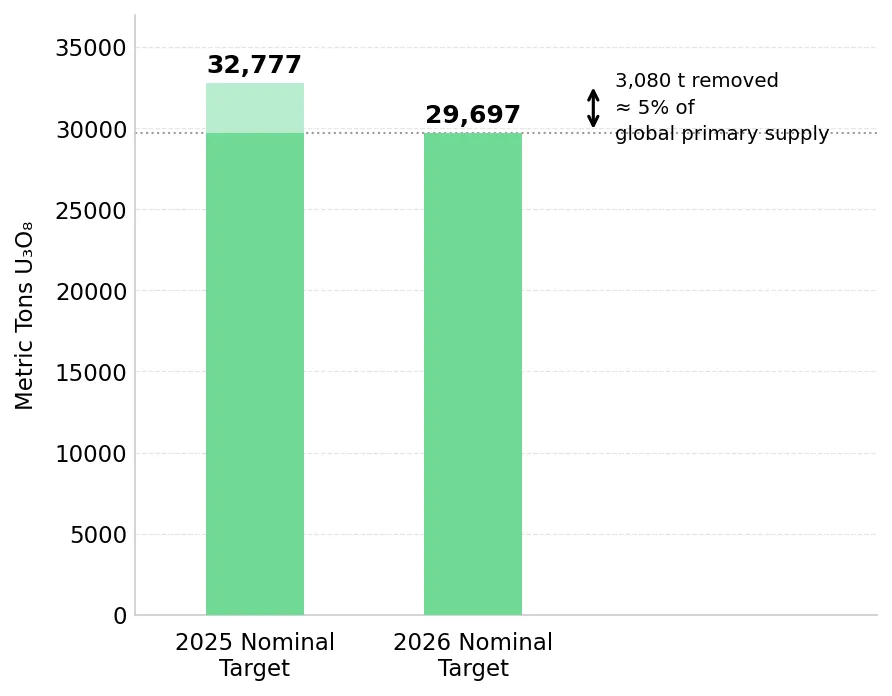

Kazatomprom's 8 Million Pound Production Cut & Tightening Uranium Supply

Kazatomprom reduced its 2026 output target from 32,777 to 29,697 metric tons of U3O8, removing roughly 8 million pounds, or 5% of global primary uranium supply. The reduction was not caused by equipment failures or supply shortages, with sulfuric acid availability in Kazakhstan remaining stable for 2026. The Company's 4Q25 Operations and Trading Update said the production cut was intended to support uranium prices rather than maximize output.

Mine supply accounts for approximately 90% of global uranium demand, with the remaining 10% coming from secondary sources such as reprocessed material and military stockpiles. These secondary supplies are finite and in long-term decline. As secondary supplies shrink, utilities become more reliant on new uranium mines, which often take years to permit, finance, and build.

Uranium's $64-Per-Pound Term Premium & Tightening Utility Supply

Long-term uranium contracts are trading near $150 per pound while the spot price sits at $86.15 because the term and spot markets serve different buyers. The spot market, which accounts for roughly 10 to 15% of uranium transactions, is dominated by traders managing short-term positions.

The term market is where nuclear utilities buy uranium for delivery 3 to 10 years in the future. Utilities cannot operate nuclear plants without uranium, so term contracting decisions are driven by long-term fuel security rather than short-term price movements. At the March 2026 Prospectors and Developers Association of Canada convention, Cameco COO Grant Isaac said the volume of uncontracted utility fuel demand "has never been bigger." Bank of America published a uranium price target of $135 per pound by 2027, citing rising nuclear investment tied to decarbonization and energy security goals. Long-term uranium contracts are already being signed roughly $15 above Bank of America's 2027 price target, indicating tighter physical supply than many financial forecasts currently assume.

For uranium developers with large defined resources, higher term prices support selling future production into long-term contracts rather than at current spot prices. Phil Williams, Chief Executive Officer of IsoEnergy Ltd., describes how institutional capital is increasingly positioning for long-term uranium supply shortages:

"Earlier this year, we went out to raise $50 million. There was over $300 million in demand in that book. It was a global set of institutional investors with very large appetites looking to write very large checks into our company and into the sector "

US Nuclear Policy & Rising Demand for Domestic Uranium

In February 2026, Georgia Power and Alabama Power received up to $26.5 billion in Department of Energy financing to expand and extend the life of existing nuclear power plants. In November 2025, Constellation Energy received a $1 billion Fed loan to restart Three Mile Island Unit 1 after the reactor had been shut down.

Executive orders signed in May 2025 directed the Nuclear Regulatory Commission to cap new reactor licensing reviews at 18 months, down from 5 to 10 years previously, reducing one of the largest regulatory obstacles to nuclear expansion identified by the International Energy Agency. A separate ban on Russian uranium imports removed a major supply source for US utilities, forcing buyers to secure uranium from domestic or allied producers.

For in-situ recovery uranium producers already operating in the US, the Russian import ban creates an immediate supply gap that domestic producers must fill. William Sheriff, Executive Chairman of enCore Energy, describes financing advantages of larger-scale uranium production:

"In terms of the ISR business, you're going to have producers that produce more than a million pounds a year. Your credit ratings go up, so your cost of capital goes down. Your ability to deal on more favorable terms with nuclear utilities increases as a larger-scale company."

Lower Interest Rates & Rising Uranium Project Valuations

For uranium development projects, interest rates directly affect NPV, which measures what future mine cash flows are worth today. A 100-basis-point rate reduction applied to a project using a 10% discount rate can increase NPV by approximately 15 to 25%, depending on mine life and project scale. Developers with long mine lives and completed feasibility studies are typically more sensitive to lower interest rates, which can increase asset valuations.

Rising Uranium Prices & Investment Opportunities Across the Supply Chain

Constrained uranium supply, growing energy security demand, and term prices near $150 per pound are improving economics for producers, developers, and exploration companies across the uranium sector.

Higher Uranium Spot Prices & Expanding Producer Margins

Energy Fuels produced 790,000 pounds of uranium oxide at the White Mesa Mill in Q1 2026 at an all-in cost of approximately $36 per pound against spot prices of $95.88 per pound, implying margins of roughly $60 per pound. Energy Fuels held $956.6 million in working capital at March 31, 2026, including $108.4 million in cash and $802.2 million in marketable securities. A pending acquisition of Australian Strategic Materials, targeting closure as early as July 2026, would expand Energy Fuels' exposure from uranium into rare earth materials used in electric motors and defense systems.

enCore Energy operates the Alta Mesa and Rosita in-situ recovery uranium plants in South Texas, both of which are running below designed capacity. Increasing production requires drilling additional wells rather than building new processing facilities, reducing the capital cost of output growth. More than half of the Company's planned future production remains uncontracted, giving investors exposure to future uranium price increases.

Higher Uranium Term Prices & Improving Development Project Economics

IsoEnergy's Hurricane Deposit in Saskatchewan's Athabasca Basin is the world's highest-grade indicated uranium resource at 34.5% U3O8 across 48.6 million pounds. On May 12, 2026, IsoEnergy reported drill results from the Hurricane South Trend, including 4.21% uranium oxide over 3.5 meters and 11.61% over 1.0 metre. Higher uranium grades reduce the amount of rock that must be mined per pound produced, lowering mining costs and project capital requirements.

Atomic Eagle's Muntanga Uranium Project in Zambia contains an independently verified uranium resource of 58.8 million pounds. A 2025 feasibility study confirmed a viable 12-year heap leach operation, but included only part of the total resource. Phil Hoskins, Chief Executive Officer of Atomic Eagle, discusses Muntanga's recent resource growth and development profile:

“We recently increased the resource 24% to 58.8 million pounds at 309 ppm. It has a feasibility study. If you were to include all of that in the mine plan without finding another pound, you'd have mine life at 3.9 million pounds per annum. ”

Exploration Companies Expanding Future Uranium Supply

ATHA Energy holds 6.8 million acres across Canada's major uranium regions and began its 2026 Angilak Exploration Program on May 1, 2026, with three drill rigs targeting 20,000 meters, funded by a CAD $63 million financing completed in February 2026. Troy Boisjoli, Chief Executive Officer of ATHA Energy, describes how consistent mineralization across the RIB Corridor could support future uranium resource growth:

“In the RIB area, we drilled 13 contiguous holes over about 14 kilometers, and every hole was mineralized. The best result was over 34 m of mineralization, including 13 meters of continuous mineralization grading over 0.5%, with grades above 8% within that interval.”

The Investment Thesis for Uranium

- The International Energy Agency projects global nuclear capacity to grow from 420 to 728 gigawatts by 2050 under its Stated Policies Scenario, a 73% increase that would require significantly higher long-term uranium purchasing even without additional demand from the current energy crisis.

- The world's largest uranium producer cut 5% of global primary supply as a deliberate commercial decision, limiting the market's ability to increase production quickly even as uranium prices rise.

- The $64-per-pound gap between spot uranium prices and long-term contracts reflects utilities securing future fuel supply, and similar gaps have historically been followed by higher spot prices.

- US support for nuclear power, including Department of Energy financing, faster reactor licensing, and a Russian uranium import ban, supports long-term uranium demand and reduces reliance on volatile spot market cycles.

- Producers operating below designed capacity can increase output without building new processing facilities, reducing the capital required for production growth.

- Development-stage uranium projects with completed feasibility studies and large verified resources could increase in value as higher term prices improve mine economics, particularly if the Fed lowers interest rates.

- Exploration companies with funded multi-year drilling programs and successful discovery histories in Canada's major uranium regions could benefit from rising demand for new uranium supply, which the International Energy Agency says will require sustained mine investment.

The uranium market was driven by rising energy security demand across more than 40 countries and deliberate supply cuts from the world's largest uranium producer.. Utilities signing long-term uranium contracts are pricing in tighter future supply than current spot market prices suggest.

Iran's blockade of the Strait of Hormuz increased government focus on energy security and alternative sources of reliable power. At the same time, Kazatomprom, which controls approximately 43% of global primary uranium supply, reaffirmed plans to produce 8 million fewer pounds in 2026 than previously planned. Together, tighter energy security policy and constrained uranium supply are driving a $64-per-pound gap between uranium's spot price and long-term contract market.

TL;DR

Iran's blockade of the Strait of Hormuz disrupted global oil supply routes, pushing more than 40 countries to expand nuclear energy plans to strengthen energy security. At the same time, Kazatomprom cut 8 million pounds from its 2026 uranium output as a deliberate commercial decision rather than an equipment failure, removing the assumption that uranium supply rises with price. Together, these forces have pushed long-term uranium contract prices to $150 per pound, $64 above the current spot price, a gap that has historically preceded higher spot uranium prices. US fed financing support and a ban on Russian uranium imports are increasing long-term demand for domestic uranium supply, benefiting producers, developers, and exploration companies differently across the uranium sector.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

%20(1).png)

Stay Informed