The Great Uranium Squeeze: Why Nuclear Fuel Just Became Wall Street's Next Hottest Bet

Uranium market surges to $72/lb as supply constraints meet rising nuclear demand. Critical infrastructure bottlenecks and high-grade discoveries reshape investment landscape.

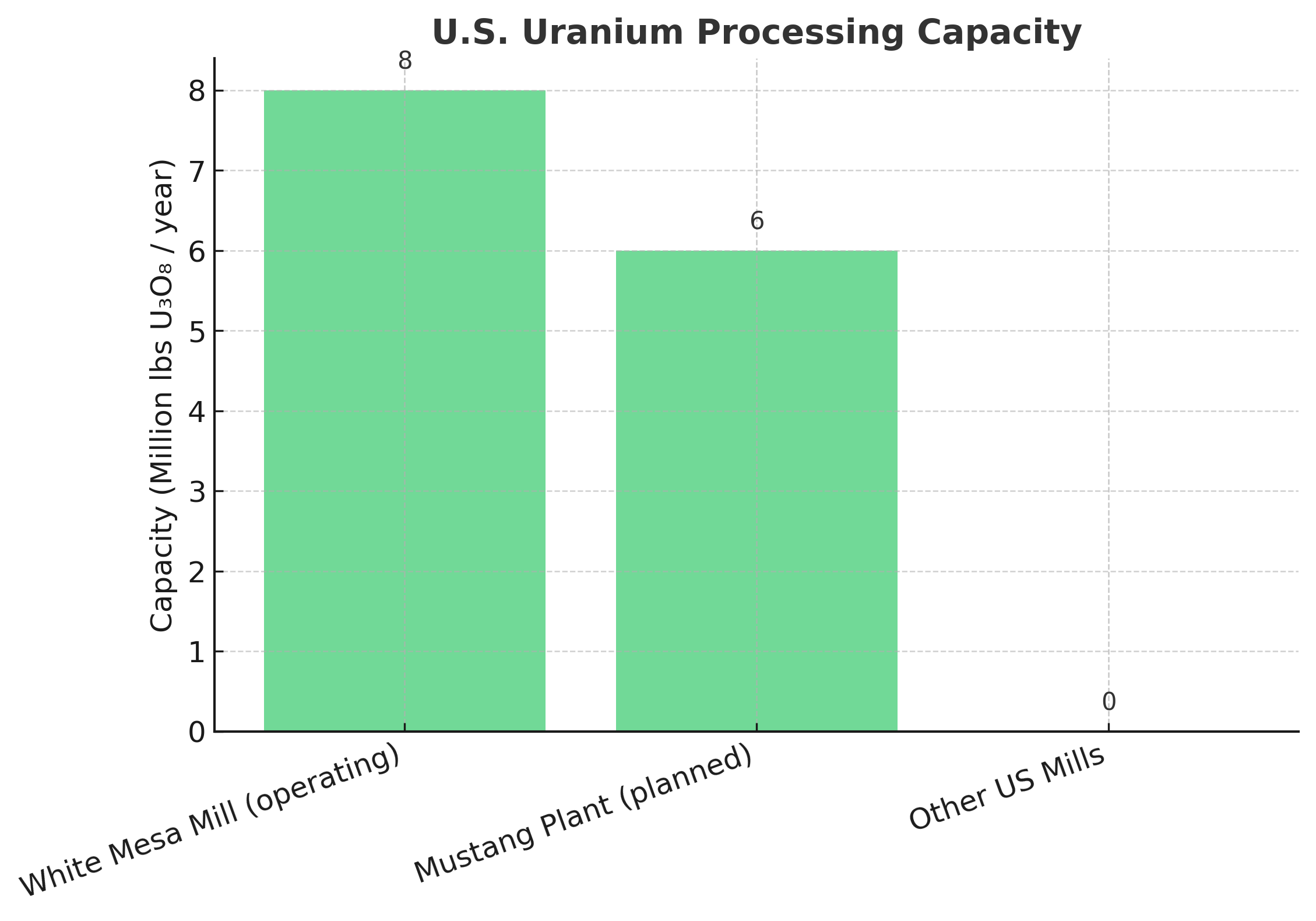

- Critical infrastructure bottlenecks are constraining global uranium supply, with the White Mesa mill in Utah representing the sole operational conventional uranium processing facility in the United States, creating a strategic chokepoint that highlights the urgent need for expanded processing capacity.

- High-grade uranium discoveries in premier jurisdictions are driving exploration activity, particularly in Canada's Athabasca Basin, where deposits such as Hurricane contain 48.6 million pounds at an exceptional 34.5% U₃O₈ grade, demonstrating the potential for world-class resources outside traditional mining regions.

- Diversification strategies are emerging as companies expand beyond uranium into critical minerals, with leading operators developing rare earth element processing capabilities and vanadium production to capture additional value streams from uranium-bearing ore bodies.

- Exploration portfolios spanning over 7 million acres across multiple basins are positioning companies for discovery upside, as geological analogues to the prolific Athabasca Basin in regions like the Angikuni, Thelon, and Baker Lake basins offer untapped potential for significant uranium resources.

- Near-term production catalysts are accelerating as formerly shuttered mines prepare for restart, with projects like Tony M in Utah leveraging existing infrastructure and full permitting to capitalize on current uranium price dynamics while new mills advance through the licensing process.

Market Dynamics Driving Uranium

Investors are looking for the best uranium companies as we enter what industry observers are calling "the new nuclear age," driven by a confluence of factors that have fundamentally altered the supply-demand equation. The spot price of $72.20 per pound represents more than a doubling from recent lows, reflecting growing recognition of uranium's critical role in global energy security and decarbonization efforts.

.png)

Western supply shortages have become particularly acute following geopolitical tensions that have disrupted traditional uranium trade flows. This supply constraint coincides with unprecedented demand growth from multiple sectors, including traditional nuclear power generation, emerging small modular reactor technologies, and the voracious energy appetite of data centers supporting artificial intelligence applications.

The COP28 nuclear pledges have provided additional momentum, with numerous countries committing to significant expansions of their nuclear power capacity. This long-term demand visibility, combined with current supply constraints, has created a favorable pricing environment that is incentivizing both restart of previously shuttered operations and development of new uranium projects.

Infrastructure Bottlenecks & Lack of Processing Capacity

Perhaps nowhere is the supply constraint more evident than in uranium processing infrastructure. The United States currently operates only one conventional uranium mill, the White Mesa facility in Utah which has become a critical chokepoint in the domestic uranium supply chain. This facility, licensed to process over 8 million pounds of U₃O₈ annually, serves not only as a uranium processor but also as the only U.S. facility capable of processing monazite into rare earth element oxides.

The strategic importance of the White Mesa mill extends beyond uranium processing. The facility has demonstrated unique capabilities in handling alternative feed materials and supporting Cold War-era mine cleanup programs, highlighting its role in national security and environmental remediation efforts. However, the concentration of such critical processing capacity in a single facility underscores the urgent need for expanded infrastructure.

Recognition of this bottleneck has prompted significant investment in new processing facilities. The development of the Mustang Mineral Processing Plant in Colorado represents a key initiative to address domestic processing capacity constraints. Built on the former Pinon Ridge Mill site, this facility benefits from existing infrastructure, including monitoring wells, power supply, and environmental controls, which should facilitate a more streamlined licensing process.

The proximity advantage of new processing facilities to mining operations cannot be overstated. The Mustang plant's location near the Sunday Mine Complex significantly reduces hauling costs compared to alternative processing options, demonstrating how strategic positioning can provide substantial economic advantages in an industry where transportation costs can significantly impact project economics.

Exploration Excellence in Premier Jurisdictions

The quality of uranium discoveries in recent years has been exceptional, particularly in Canada's Athabasca Basin, which continues to set global standards for uranium grade and resource quality. The Hurricane deposit exemplifies this trend, containing 48.6 million pounds of indicated resources at an extraordinary 34.5% U₃O₈ grade, making it Canada's highest-grade published indicated uranium resource.

What makes the Hurricane deposit particularly compelling is its robustness across various economic scenarios. The deposit demonstrates remarkable insensitivity to cut-off grade assumptions, retaining 93.9% of its contained metal even at a 10% cut-off grade. This characteristic provides significant downside protection and suggests the deposit could remain economic across a wide range of uranium price scenarios.

The geological context of these discoveries extends far beyond individual deposits. The Athabasca Basin has produced over 900 million pounds of uranium historically, and Saskatchewan ranks second worldwide in mining investment attractiveness. This proven track record, combined with continued exploration success, reinforces the basin's status as a premier uranium jurisdiction.

However, exploration activity is not limited to the Athabasca Basin. Geological analogues in the Angikuni, Thelon, and Baker Lake basins offer significant untapped potential. The Angilak project, which features a 31-kilometer structural corridor with surface samples assaying up to 30% U₃O₈, demonstrates that high-grade uranium mineralization extends beyond traditional mining areas.

Recent discoveries continue to validate this exploration thesis.

"The RIB East Discovery represents the second new discovery (first being KU Discovery) during the 2025 Angilak Exploration Program, beyond the Lac 50 Deposit Trend in the Angikuni Basin. These results continue to confirm the Company's exploration approach and thesis, while demonstrating our technical team's ability to execute and discover. The Company is thrilled with the fact that the RIB East Discovery has high‑grade mineralization hosted within a graphitic structure – a known setting for mineralization in all major Athabasca Basin deposits and mines. We are at the early stages of understanding the potential of RIB East, with drilling covering just 400 m of a 2 km long anomaly. The early successes of the 2025 Angilak Exploration Program truly illustrate how underexplored and robust the mineralizing system is in the Angikuni Basin," - Troy Boisjoli, CEO of ATHA Energy.

The scale of current exploration efforts is unprecedented. Companies are collectively managing portfolios exceeding 7 million acres across multiple Canadian basins, representing one of the largest exploration commitments in the sector's history. This extensive land position provides multiple opportunities for discovery and reflects confidence in the long-term uranium outlook.

Resource Scale & Development Pipeline

The scale of uranium resources under development provides insight into the sector's long-term supply potential. Beyond the headline-grabbing high-grade deposits, significant resources are being advanced across multiple jurisdictions and geological settings.

In the United States, the Tony M mine in Utah exemplifies the restart potential within the domestic uranium industry. Having produced approximately 1 million pounds historically between 1979 and 2008, the mine benefits from extensive existing infrastructure, including 29 kilometers of underground development, power stations, and ore processing facilities. This infrastructure advantage significantly reduces the capital requirements for restart compared with greenfield development.

The diversity of uranium deposit types under development provides important portfolio balance. While high-grade Athabasca-style deposits capture headlines, larger lower-grade resources also play crucial roles in supply security. The Dieter Lake project, containing 24.4 million pounds at 0.06% U₃O₈, represents the type of resource that could provide steady, long-term production to complement higher-grade, shorter-life deposits.

International projects add further geographic and geological diversification. The Coles Hill project in Virginia, despite current mining restrictions, contains approximately 163 million pounds of historic resources, representing one of the largest undeveloped uranium deposits in the United States. Such resources provide optionality for future development as regulatory frameworks evolve.

The development pipeline extends beyond traditional uranium mining jurisdictions. Projects in Quebec, including the Matoush deposit with 12.3 million pounds of indicated resources at 0.95% U₃O₈, demonstrate high-grade potential outside the Athabasca Basin. Similarly, international holdings in Australia provide exposure to established uranium mining jurisdictions with different geological and regulatory characteristics.

Operational Excellence & Cost Management

The economics of uranium production have improved dramatically with rising prices, but operational excellence remains crucial for sustainable profitability. Current production costs at leading operations are expected to decline to approximately $23-30 per pound by the fourth quarter of 2025, providing substantial margins at current uranium prices.

This cost improvement reflects both operational optimization and economies of scale as production ramps up. The Pinyon Plain mine in Arizona has demonstrated particularly strong performance, with ore reconciliation showing grades 33-100% higher than initial estimates. Such outperformance not only improves project economics but also validates geological models and exploration techniques.

"This quarter delivered proof that our long‑term commitment to the Pinyon Plain uranium mine has been worth the effort, as the mine continues to be one of the highest, if not the highest, grade uranium mine in U.S. history. The exceptional production at this mine is a 'once in a lifetime event' and has come at the perfect time for Energy Fuels as it places us in the enviable position of increasing production while lowering costs." - Mark Chalmers, CEO of Energy Fuels.

The integration of multiple revenue streams represents an increasingly important aspect of uranium operations. The co-production of vanadium from uranium-bearing ores provides additional revenue that can significantly improve project economics. Some operations report vanadium-to-uranium ratios as high as 9:1, highlighting the potential for vanadium to become a primary revenue driver under certain market conditions.

Processing efficiency improvements continue to drive cost reductions. Advanced techniques including ore sorting and slurry ablation are being implemented to optimize recovery rates and reduce processing costs. These technological improvements, combined with operational scale increases, position leading operators to maintain profitability even in more challenging price environments.

Critical Minerals Integration & Value Enhancement

The uranium industry is increasingly recognizing opportunities to capture additional value through critical minerals processing. This diversification strategy not only provides revenue upside but also enhances strategic value by producing materials essential to modern technology and defense applications.

Rare earth element production from uranium operations represents a particularly compelling opportunity. The White Mesa mill has achieved commercial-scale production of neodymium-praseodymium (NdPr) oxide, with pilot production of heavy rare earth oxides including dysprosium and terbium planned for 2025. The market dynamics for these materials are extremely favorable, with dysprosium prices up 348% in Europe and terbium up 367%.

The advantage of producing rare earth elements from monazite, a uranium-bearing mineral, extends beyond simple co-production economics. Monazite offers high grades of 50-60%+ total rare earth oxides, higher recovery rates, easier processing characteristics, and uranium byproduct value. This combination of advantages provides significant competitive positioning compared with traditional rare earth operations.

International projects are being developed specifically to support this critical minerals strategy. The Toliara project in Madagascar has the potential to produce 26,000 tonnes per annum of monazite, supporting 2,600 tonnes per annum of NdPr production along with significant dysprosium and terbium output. A final investment decision is expected in the first half of 2026.

The medical isotope market represents another emerging opportunity for uranium operators. The development of radium-226/228 recovery for Targeted Alpha Therapy in cancer treatment could provide high-value revenue streams from existing operations. While currently in the research and development stage, the potential for commercial off-take agreements represents significant upside potential.

Financial Positioning & Capital Allocation

The uranium sector's financial health has improved dramatically with rising commodity prices, but capital allocation strategies vary significantly across the industry. Leading companies maintain strong balance sheets with substantial liquidity positions, providing flexibility to capitalize on market opportunities and weather potential volatility.

Liquidity positions exceeding $250 million are not uncommon among leading operators, with diversified holdings including cash, marketable securities, and valuable inventory positions. Inventory management has become particularly strategic, with companies holding significant uranium stockpiles to benefit from favorable pricing trends while maintaining operational flexibility.

The absence of debt in many uranium companies provides significant strategic advantages. Debt-free balance sheets enable companies to pursue growth opportunities without financial constraints and provide downside protection during market volatility. This financial strength also positions companies to pursue strategic acquisitions as consolidation opportunities emerge.

Equity portfolios in uranium juniors provide additional strategic value beyond financial returns. Holdings in exploration companies provide exposure to discovery upside while maintaining liquidity and portfolio diversification. These strategic investments also provide industry intelligence and potential acquisition targets as projects advance through development stages.

Strategic Partnerships & Industry Consolidation

The uranium industry is witnessing increased strategic collaboration as companies seek to optimize capital allocation and reduce development risks. Joint venture structures and carried interest arrangements provide mechanisms for companies to maintain exposure to multiple projects while managing capital requirements.

Carried interest positions in major uranium projects provide particularly attractive risk-adjusted exposure. Companies maintain 10% interests in significant exploration projects while avoiding capital contributions, allowing them to benefit from discovery upside without diverting resources from core development activities.

The technical expertise available within the uranium industry continues to strengthen as experienced professionals from major uranium companies join emerging developers. Management teams with backgrounds at Cameco, NexGen, and other industry leaders bring operational expertise and industry relationships that significantly enhance development prospects.

Strategic partnerships extend beyond traditional joint ventures to include processing agreements and technical collaborations. Ore purchase agreements and toll processing arrangements provide operational flexibility while optimizing capital utilization across the industry. These partnerships become particularly valuable during periods of processing capacity constraints.

Market Dynamics

Despite the favorable market environment, uranium investments carry significant risks that must be carefully evaluated. Regulatory approval processes for new mines and processing facilities can be lengthy and uncertain, potentially delaying project development and capital returns.

Geopolitical factors continue to influence uranium markets, with trade relationships and supply chain security becoming increasingly important considerations. The concentration of uranium production in certain countries creates supply vulnerability that both creates opportunities for alternative suppliers and represents ongoing market risk.

Environmental and social considerations remain crucial factors in uranium project development. Community engagement and environmental stewardship are essential for maintaining social license to operate, particularly in sensitive jurisdictions or near indigenous communities.

Market cyclicality remains a fundamental characteristic of uranium markets. While current fundamentals are strong, investors must consider the potential for price volatility and the impact of changing market conditions on project economics and development timelines.

Investment Implications

Investors are starting to understand the uranium bull market thesis as we enter a mature phase characterized by sustained higher prices and increased sector confidence. The combination of supply constraints, infrastructure bottlenecks, and growing demand from multiple sectors creates a favorable environment for well-positioned uranium companies. But it is the retail uranium bull sentiment that is currently driving share price, not fundamentals.

The development pipeline of high-quality projects across multiple jurisdictions provides confidence in the sector's ability to respond to growing demand. However, the timeline for bringing new production online remains extended, suggesting that current supply-demand imbalances may persist for several years.

Technological advances in both mining and processing continue to improve project economics and environmental performance. These improvements, combined with higher uranium prices, are expanding the universe of economically viable uranium projects and creating opportunities for resource expansion at existing operations.

The integration of critical minerals production with uranium operations represents a significant value enhancement opportunity that is still in the early stages of development. As these strategies mature, they could provide substantial additional revenue streams that improve project economics and reduce uranium price sensitivity.

For investors, the uranium sector offers exposure to a critical commodity with strong fundamental drivers and limited alternative supply sources. The combination of supply constraints, growing demand, and high-quality development projects creates an attractive investment environment, though careful project selection and risk management remain essential for success.

The uranium renaissance reflects broader trends toward energy security, decarbonization, and critical minerals independence. These long-term themes provide confidence that current market dynamics represent more than a cyclical upturn, suggesting sustained opportunity for well-positioned uranium investments.

Analyst's Notes

Subscribe to Our Channel

Stay Informed