US Tariffs Extend Trade Uncertainty Into 2027, Pushing Gold Above $5,100 Per Ounce: Expanding Producer Cash Margins to Historically Elevated Levels

US tariffs push gold above $5,100/oz, expanding producer cash margins to historic highs. Discover which miners, developers, and explorers benefit most.

- President Trump's invocation of Section 122 to impose a 10% global tariff, alongside Section 301 and 232 investigations, introduces prolonged trade uncertainty rather than a short-term policy shock.

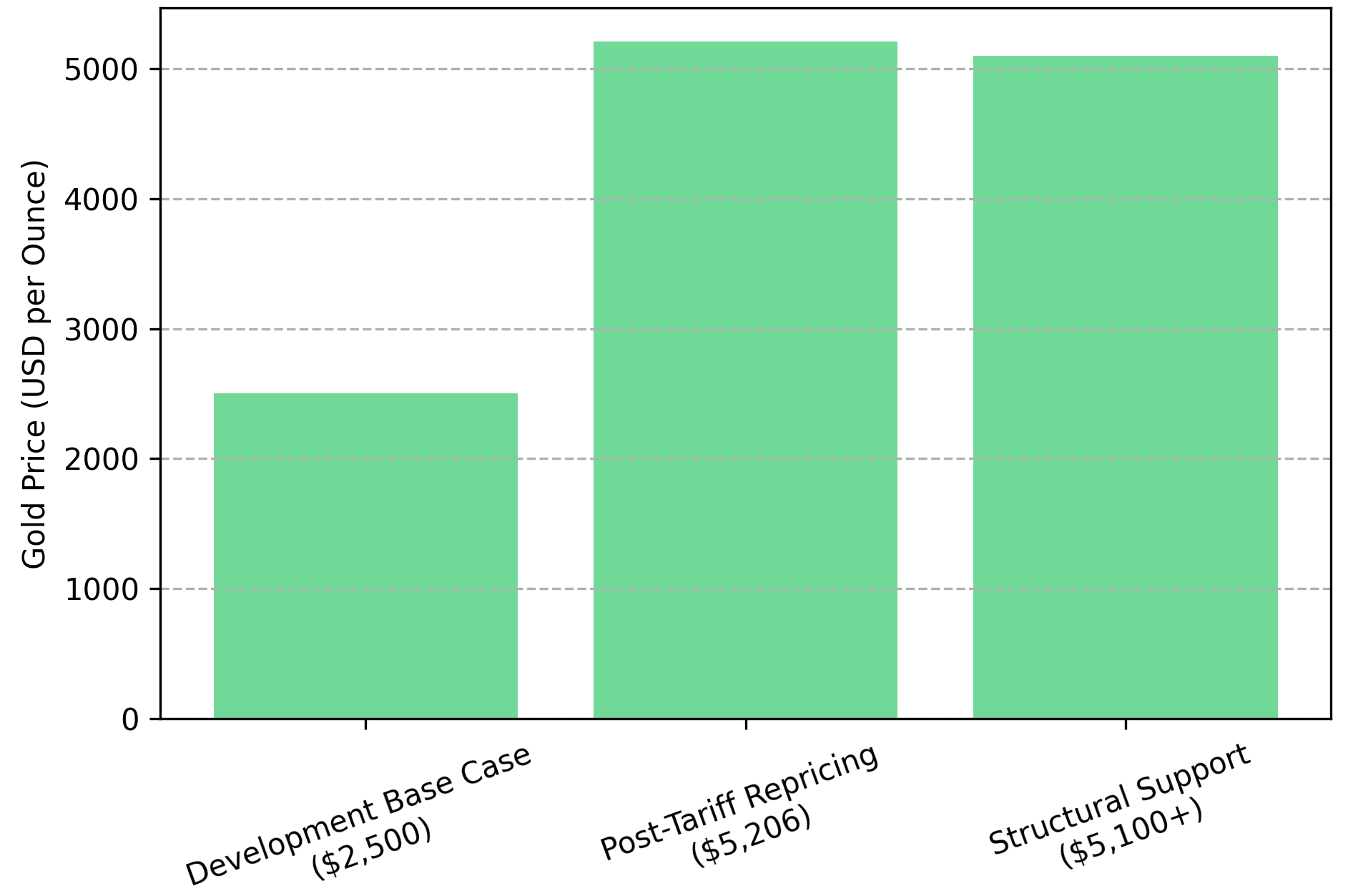

- Gold surged above $5,206 per ounce on February 23, 2026, and has remained above $5,100 per ounce, reflecting safe-haven demand amid elevated inflationary and geopolitical risk.

- While Treasury rotations and fading rate-cut expectations create near-term volatility, structural trade fragmentation supports a sustained higher price regime.

- Producers with all-in sustaining costs (AISC) below $1,800 per ounce are generating historically elevated cash margins at $5,000-plus gold, materially altering capital allocation and debt capacity.

- Developers and explorers with robust internal rates of return (IRR), scalable resources, and Tier-1 jurisdictions are positioned for EV/oz re-ratings if elevated gold prices persist.

Section 122 & the Repricing of Trade Risk

President Trump's use of Section 122 of the Trade Act of 1974 to impose a 10% global import tariff, while simultaneously initiating formal Section 301 and 232 investigations, represents a structural policy escalation with durable market consequences. Unlike traditional trade measures, Section 122 requires no prior investigation and functions as a stopgap mechanism subject to Congressional approval for extension after 150 days, while formal probes proceed on timelines that have historically extended up to a year. The effective trade uncertainty window extends well into 2026 and 2027.

The significance for markets is duration. Trade friction is no longer episodic - it is embedded into the policy timeline. Investors must now discount elevated import costs, inflationary pass-through, retaliatory trade measures, and supply chain realignment simultaneously. Reuters reported gold reaching $5,206.39 per ounce on February 23, 2026, with the metal remaining above $5,100 per ounce through the following session. This repricing reflects geopolitical and policy risk, not simply a commodity cycle.

This is not a commodity story first. It is a macro stability story. The structural nature of Section 122, combined with the open-ended timeline of formal investigations, means investors cannot model a near-term resolution. That uncertainty has a price, and gold is where markets are paying it.

Safe-Haven Inflows & the Rate Expectations Tension

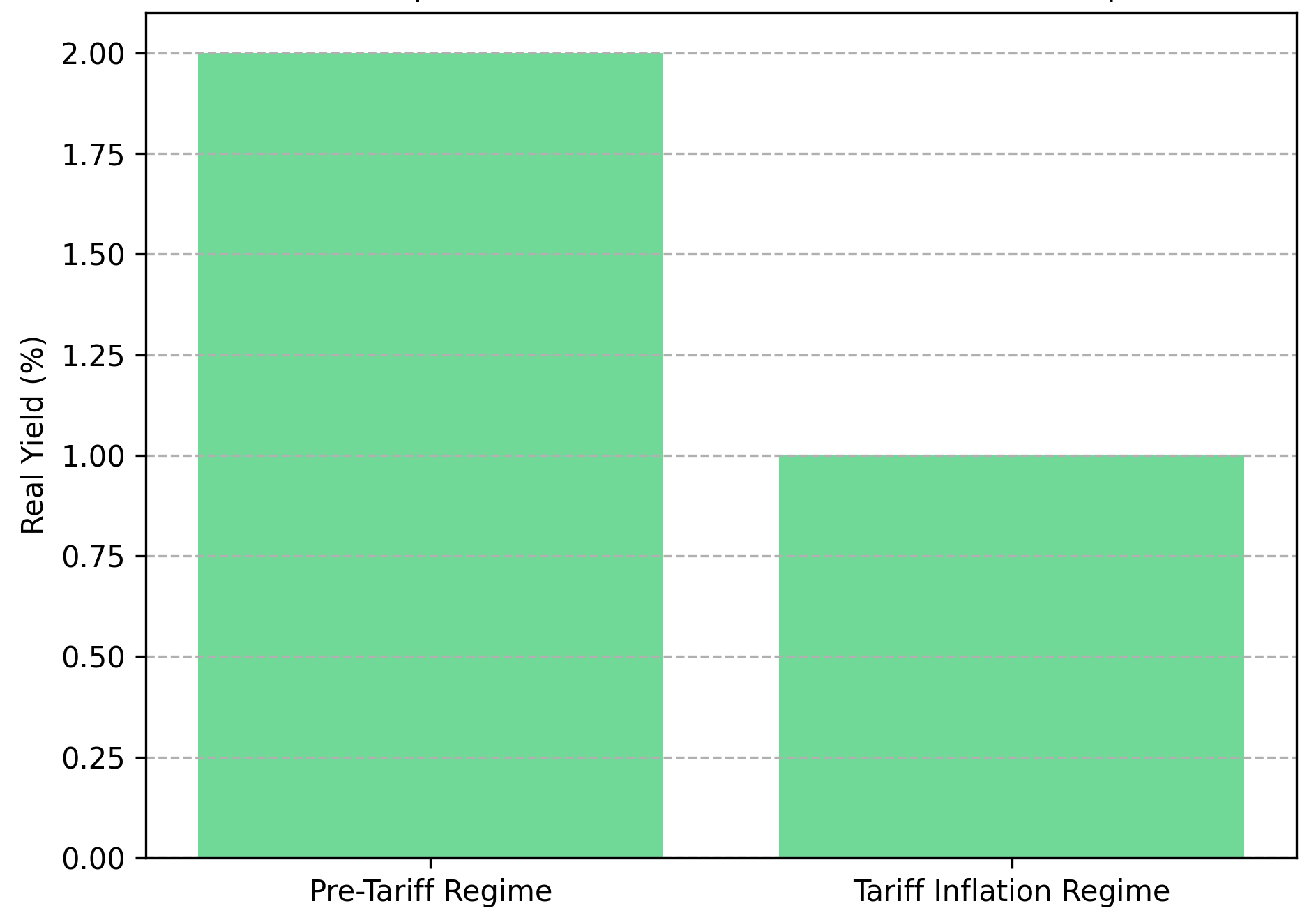

Gold initially rallied more than 2% following the tariff announcement before consolidating near $5,158 per ounce. Two forces now define the near-term outlook: safe-haven demand tied to trade and geopolitical stress, and reduced expectations of near-term Federal Reserve rate cuts driven by elevated inflation risk. Tariffs are inherently inflationary, and when markets reprice inflation upward, rate-cut expectations fall, supporting nominal yields.

Gold typically performs best when real yields, measured as nominal yields minus inflation expectations, compress. If tariffs lift inflation expectations faster than nominal yields rise, gold remains structurally supported. This creates a regime of tactical volatility set against durable macro backing.

The Federal Reserve faces a constrained response function. Tightening into tariff-driven inflation risks exacerbating an economic slowdown, while accommodating it risks entrenching above-target price levels. This policy bind reinforces the macro case for gold as a hedge against asymmetric policy outcomes on both ends of the rate spectrum.

Producer Margin Expansion at $5,000-Plus Gold

At current prices above $5,100 per ounce, producers with AISCs between $1,600 and $1,800 per ounce are generating historically elevated margins. AISC, or all-in sustaining cost, captures operating costs plus sustaining capital and corporate general and administrative expenses - providing a more complete profitability measure than cash cost alone.

Perseus Mining reported AISC of US$1,649 per ounce for the six months ending December 31, 2025, against a realized price of US$3,241 per ounce during that period. At current spot levels, margins expand considerably further, reinforcing the company's US$755 million net cash position as of the same reporting period. Serabi Gold, operating in Brazil's Tapajos Province, delivered AISC of US$1,816 per ounce alongside EBITDA of US$48.2 million through the third quarter of 2025. Driven by the Coringa mine, the company is ramping consolidated production toward approximately 60,000 ounces annually by 2026.

Integra Resources generates consistent free cash flow from its Florida Canyon operation in the Great Basin while advancing DeLamar through a Feasibility Study dated February 2, 2026, which carries a 97% IRR. Integra recently announced a $60 million financing that was three times oversubscribed and supported by 12 new institutional investors, with proceeds directed entirely to DeLamar early works. i-80 Gold, operating across a Nevada brownfield portfolio, reported full-year 2025 revenue of $95.2 million. The company's published guidance outlines a transition from third-party toll processing through 2027 to internal processing at the Lone Tree autoclave facility beginning in 2028, a shift management anticipates will reduce per-ounce processing costs by $1,000 to $1,500.

George Salamis, President & Chief Executive Officer, Integra Resources, on Florida Canyon's margin profile:

"Florida Canyon continues to deliver strong margins. We're still making $2,500 of margin per gold ounce produced... Florida Canyon is going great. It's doing exactly what we said it would."

Development Assets: IRR Sensitivity & Capital Discipline

Developers benefit disproportionately from sustained price regimes because IRR and NPV models are highly sensitive to commodity price inputs. A project carrying a 56% IRR at $2,500 per ounce gold can see that return expand materially as spot pricing approaches $5,000 per ounce, depending on cost structure and capital intensity.

New Found Gold's Queensway project in Newfoundland reported a 56.3% IRR and C$743 million NPV at a 5% discount rate in its Preliminary Economic Assessment, filed September 2, 2025, at a $2,500 per ounce base case. Through the acquisition of Maritime Resources, which closed November 13, 2025, New Found Gold also acquired full ownership of the Pine Cove Mill and tailings facility, along with the Hammerdown mine, which is currently ramping toward steady-state production in 2026. This positions the company as a transitioning producer with district-scale development optionality across 110 kilometers of strike in one of Canada's most prospective mining provinces.

Hashim Ahmed, Chief Financial Officer, New Found Gold, on financial discipline in a rising gold price environment:

"Financial discipline as we transition is one of my key focuses... What we internally look at is how much cash are we generating net-net... It's being financially disciplined in making sure that this gold price does not allow us to make wrong decisions."

Cabral Gold, advancing its heap leach project in Brazil's Tapajos Province, outlined a 78% after-tax IRR and US$1,210 per ounce AISC in its Prefeasibility Study released July 29, 2025, at a $2,500 per ounce base case. The board approved the construction decision in October 2025; earthworks are in progress, long-lead items have been ordered, and a US$45 million gold loan construction financing closed November 26, 2025. First production is targeted for Q4 2026. Hycroft Mining, located in Nevada, holds measured and indicated resources of 16.41 million ounces of gold and 562.57 million ounces of silver, alongside approximately $199 million in unrestricted cash as of February 9, 2026. An ongoing drill program of approximately 14,500 meters targets the Vortex and Brimstone high-grade silver systems, with the company planning to expand to five rigs in the second half of 2026.

Diane Garrett, President & Chief Executive Officer, on Hycroft Mining’s resource scale and balance sheet strength:

"We've got about $200 million US in the bank. It makes it really one of the most attractive balance sheets in the industry, and that's allowing us to really expedite and accelerate the drill program."

Tudor Gold controls 24.9 million ounces of gold in the indicated category at Treaty Creek in British Columbia through an 80% project interest, with negotiations ongoing with joint venture partner American Creek Resources to consolidate to 100% ownership. The company's current development focus targets higher-grade starter zones averaging 3 grams per tonne or better, sized for an underground mine of 8,000 to 10,000 tonnes per day. U.S. Gold Corp holds permitted reserves of 1.672 million gold-equivalent ounces at its CK Gold project in Wyoming, with a tight capital structure of approximately 16.4 million shares outstanding. Management describes the project as shovel-ready as it completes a Definitive Feasibility Study, a characterization consistent with CK Gold's existing construction permit.

Exploration Optionality in a High-Price Cycle

Explorers offer convex exposure to sustained commodity cycles. In structurally bullish macro regimes, risk capital returns selectively to projects in Tier-1 jurisdictions with the scale required to justify feasibility-stage capital allocation. P2 Gold is advancing the Gabbs gold-copper project in Nevada, targeting a resource profile exceeding 5 million gold-equivalent ounces against a current base of 3.45 million gold-equivalent ounces

Joseph Ovsenek, President & Chief Executive Officer, on P2 Gold’s project economics at spot pricing:

"We had a 108% IRR. NPV at a 15% discount rate was roughly $1.5 billion, the NPV at a 5% discount rate was close to $3.5 billion. This project is very robust at low metal prices and kicks off a lot of cash as the gold price goes up."

These figures represent management's internal sensitivity analysis at spot gold prices, distinct from the base-case economics of the company's 2025 Preliminary Economic Assessment. Environmental baseline studies are underway, with a water permit targeted for Q1 2026 and a construction decision targeted for late 2027, subject to permitting outcomes. Projects of this scale in established Nevada mining districts attract sustained institutional attention during elevated price cycles.

Jurisdictional Advantages

Trade fragmentation reinforces capital preference for politically stable, permitting-transparent jurisdictions. According to the Fraser Institute's Annual Survey of Mining Companies - with survey data referenced by companies in this report spanning the 2024 and 2025 survey years - Nevada, Newfoundland, Wyoming, and British Columbia rank among the top jurisdictions globally for investment attractiveness. In periods of elevated global uncertainty, jurisdictional premiums tend to expand as investors assign lower discount rates to assets with reduced above-ground political risk.

Luke Norman, Management, U.S. Gold Corp, on the scarcity value of a permitted, shovel-ready project:

"We are one of the only permitted, shovel-ready, fully ready-to-go projects in North America sitting within a junior. That is sending a lot of interested capital our way."

Brazilian producers and developers, including Serabi Gold and Cabral Gold, operate in the established Tapajos Province mining district with a long track record of operating history that partially offsets the emerging-market risk premium. Perseus Mining's West African portfolio introduces broader jurisdictional diversification while its US$755 million net cash position provides a substantial liquidity buffer against operational or political disruption. Jurisdiction does not eliminate risk, but in volatile macro regimes it directly influences capital access, valuation multiples, and development execution capacity.

Risk Factors & Conditions

Balanced analysis requires identifying conditions under which the current gold price regime could reverse. Rapid trade de-escalation through bilateral agreements under the Section 301 and 232 investigation frameworks would reduce geopolitical risk premiums. Aggressive Federal Reserve tightening that lifts real yields sharply above current levels would directly compress gold's valuation support. Sustained USD appreciation presents a related risk, as does supply-side acceleration from higher-cost producers incentivized by elevated prices.

Investors should monitor the real yield trajectory, Treasury flow patterns, and Section 301 and 232 investigation outcomes closely. Structural uncertainty appears durable given the embedded timeline of formal investigations, but gold remains rate-sensitive. Any material shift in Federal Reserve forward guidance could introduce significant near-term price volatility even within an otherwise supportive macro backdrop.

The Investment Thesis for Gold

The current macro environment presents a coherent multi-factor case for sustained gold exposure.

- Sustained $5,000-plus gold materially expands producer free cash flow relative to AISC, creating capital allocation flexibility that supports dividend capacity, debt reduction, and organic growth simultaneously.

- Development projects with IRRs above 50% at $2,500 per ounce gold demonstrate substantial economic leverage at current spot prices, with payback periods compressing and financing terms improving as the gap between modeled and realized pricing widens.

- Strong balance sheets across producers and advanced developers reduce equity dilution risk, lower the cost of project-level financing, and improve optionality for mergers and acquisitions in an environment where premium assets command elevated valuations.

- Tier-1 jurisdiction concentration in Nevada, Newfoundland, Wyoming, and British Columbia may command valuation premiums relative to assets in higher-risk operating environments, as capital allocation in fragmented trade conditions increasingly rewards political and regulatory predictability.

- Exploration assets in scalable Nevada-based systems, such as P2 Gold's Gabbs project, offer convex upside if macro support persists and risk capital continues to rotate toward projects with defined feasibility pathways.

- Portfolio construction may prioritize production-stage companies with demonstrated margin resilience, development-stage assets with defined permitting timelines and infrastructure access, and selective exploration exposure where resource scale justifies the risk-adjusted return profile.

Section 122 investigations run on statutory timelines that extend into 2026 and 2027, and formal Section 301 and 232 probes carry no mandated resolution date. Gold trading above $5,000 per ounce reflects that timeline - and absent an early bilateral trade resolution under Section 301 or 232, or a material shift in Federal Reserve forward guidance that lifts real yields sharply, the conditions supporting that price level remain in place.

Producers with AISC well below current spot prices are generating free cash flow that did not exist at $2,500 per ounce gold. Developers carrying IRRs modeled at $2,500 per ounce are seeing those returns expand at current prices without changes to their cost structures or capital requirements. Explorers in Tier-1 jurisdictions with resources large enough to support feasibility-stage capital are attracting institutional attention that lower price environments did not justify. If Section 301 and 232 investigations proceed without early resolution and real yields remain below inflation expectations, the conditions that pushed gold above $5,000 per ounce remain in place - which means the current price level is more likely to function as a floor for investment modeling than as a ceiling investors are timing against.

TL;DR

President Trump's Section 122 tariff action has embedded trade uncertainty into the policy horizon through 2027, driving gold above $5,100 per ounce as markets price structural geopolitical and inflationary risk. Producers with AISCs below $1,800 per ounce are generating historically elevated cash margins, while developers carrying IRRs above 50% at $2,500 base-case gold now demonstrate substantial economic leverage at spot pricing. Tier-1 jurisdictions — Nevada, Newfoundland, Wyoming, and British Columbia — are attracting capital preference as trade fragmentation rewards political and regulatory predictability. The investment case spans producers with demonstrated free cash flow resilience, developers with defined permitting timelines, and explorers in scalable systems with institutional-grade resource profiles.

FAQs (AI-Generated)

Gold surpassed $5,100 per ounce primarily because President Trump's invocation of Section 122 introduced structural, multi-year trade uncertainty rather than a temporary policy shock. Simultaneously, inflationary pressure from tariffs has complicated Federal Reserve rate policy, compressing real yields and reinforcing gold's safe-haven appeal.

Section 122 of the Trade Act of 1974 allows the President to impose a temporary global import tariff without prior investigation. Because it runs concurrently with longer Section 301 and 232 formal investigations — which can take up to a year — the effective uncertainty window extends well into 2026 and 2027, giving gold sustained macro support beyond an initial price spike.

Producers with all-in sustaining costs (AISC) between $1,600 and $1,800 per ounce are generating margins of $3,300 or more per ounce at current spot prices above $5,100. This materially expands free cash flow, enabling dividend capacity, debt reduction, and organic growth without relying on equity markets.

Benefit is distributed across the capital structure but varies in nature. Producers capture immediate margin expansion. Developers see IRR and NPV models reprice sharply upward, improving financing terms and payback periods. Explorers in Tier-1 jurisdictions with scalable resource profiles attract risk capital as institutional investors seek convex upside within politically stable operating environments.

Key reversal risks include rapid trade de-escalation through bilateral agreements under Section 301 and 232 frameworks, aggressive Federal Reserve tightening that sharply lifts real yields, sustained US dollar appreciation, and supply-side acceleration from higher-cost producers incentivised by elevated prices. Investors should monitor real yield trajectories and Federal Reserve forward guidance closely.

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

Stay Informed