Copper Supply Constraints & a 70% Demand Coverage Gap Drive Interest in Deliverable Projects

Copper supply constraints and a 70% demand coverage gap are raising the value of developers, explorers, and restart projects positioned for future production.

- Major mine disruptions at Grasberg, El Teniente, and Kamoa-Kakula have turned copper's long-forecast deficit into a realized, multi-year shortfall, with Jefferies modeling an average annual deficit near 491,000 tonnes through 2030.

- The binding constraint is no longer the copper price but the thin pipeline of new mines, with the International Energy Agency estimating that existing and planned projects will satisfy only about 70% of 2035 demand.

- Investors are assigning higher valuations to projects with completed economic studies, manageable capital requirements, and credible permitting and financing pathways because these projects have a clearer route to production than similarly sized undeveloped deposits.

- Development-stage and exploration-stage companies that advance permitting, financing, resource definition, or restart plans offer exposure to the supply shortfall because they increase the likelihood of future copper production.

- The thesis carries risk because weaker Chinese demand, crowded long positioning, or faster-than-expected mine restarts could narrow the deficit, while pre-production miners remain pre-revenue and highly sensitive to financing and permitting outcomes.

Mine Disruptions Turn the Copper Deficit from Forecast to Reality

For most of the past decade, analysts forecast a copper deficit, but new supply kept the market balanced. Mine disruptions in 2025 and 2026 pushed copper consumption above available supply. A series of mine disruptions removed hundreds of thousands of tonnes of copper supply within months. Freeport-McMoRan's Grasberg in Indonesia, the world's second-largest copper mine, declared force majeure after a September 2025 mudslide and pushed its full restart from 2027 to 2028; Benchmark Mineral Intelligence estimates roughly 600,000 tonnes of contained copper will be lost between that event and the end of 2026. Disruptions at Codelco's El Teniente and sulphuric-acid shortages at Kamoa-Kakula further reduced supply and widened the deficit.

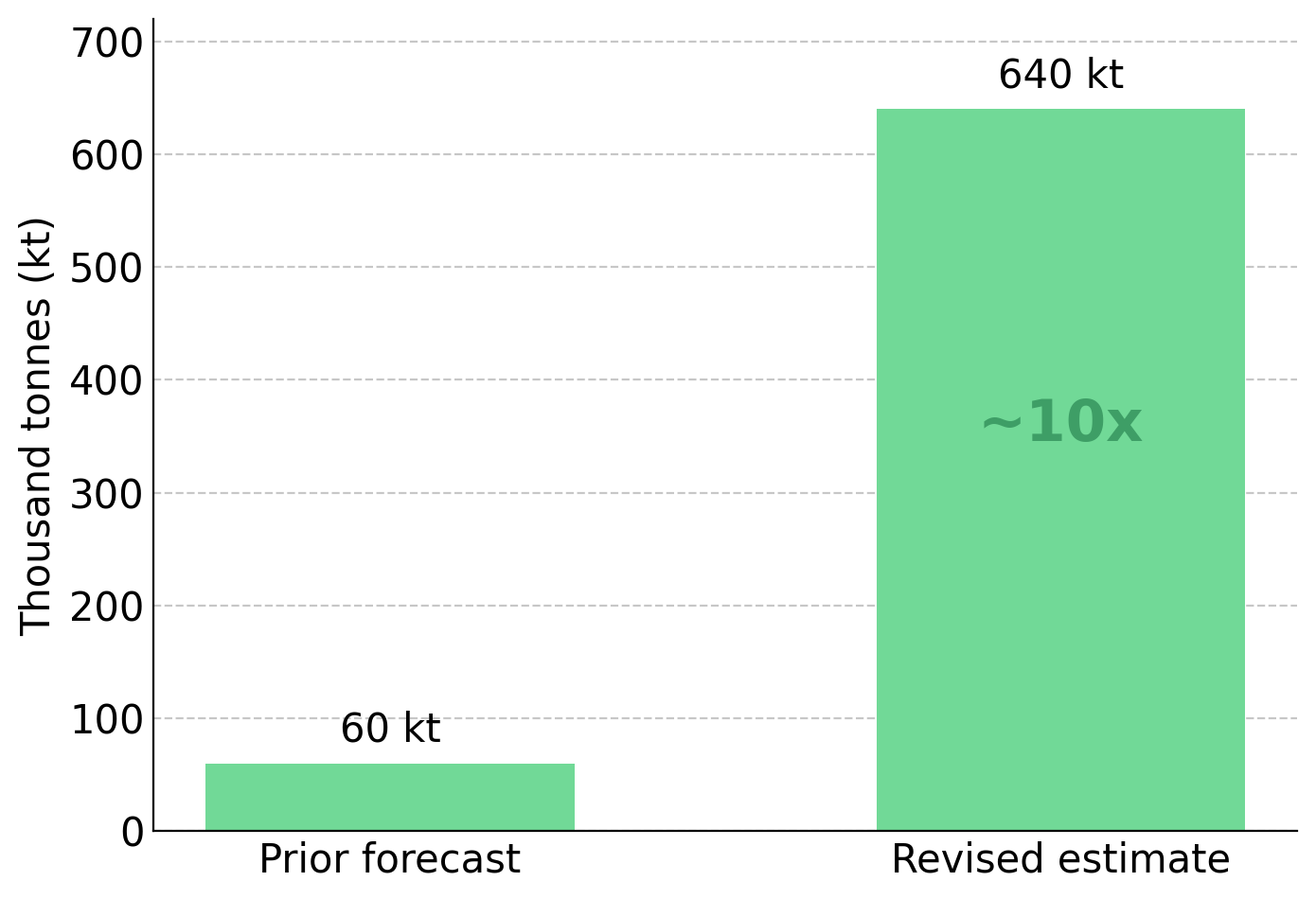

Goldman Sachs raised its 2026 copper deficit estimate outside the US to roughly 640,000 tonnes, about ten times its prior forecast, while the International Copper Study Group now expects a refined-market deficit after two years of surplus. A deficit means refined copper consumption exceeds refined supply. Because copper must move from concentrate to refined metal, mine disruptions can take months to reach inventories but are difficult to reverse once they do.

Concentrated Mine Supply Increases the Value of New Copper Projects

The 20 largest mines account for about 36% of global copper output, so a single mega-mine outage can shift the global supply balance. Many of these mines are aging, deeper, and more technically challenging, which increases disruption risk and limits how quickly higher prices can bring on new supply.

Supply concentration increases the value of development-stage and exploration-stage projects that can bring new copper supply to the market. As supply risks increase, capital is moving beyond major producers toward developers and explorers with a credible path to production.

New Mines, Not Higher Prices, Are the Real Copper Bottleneck

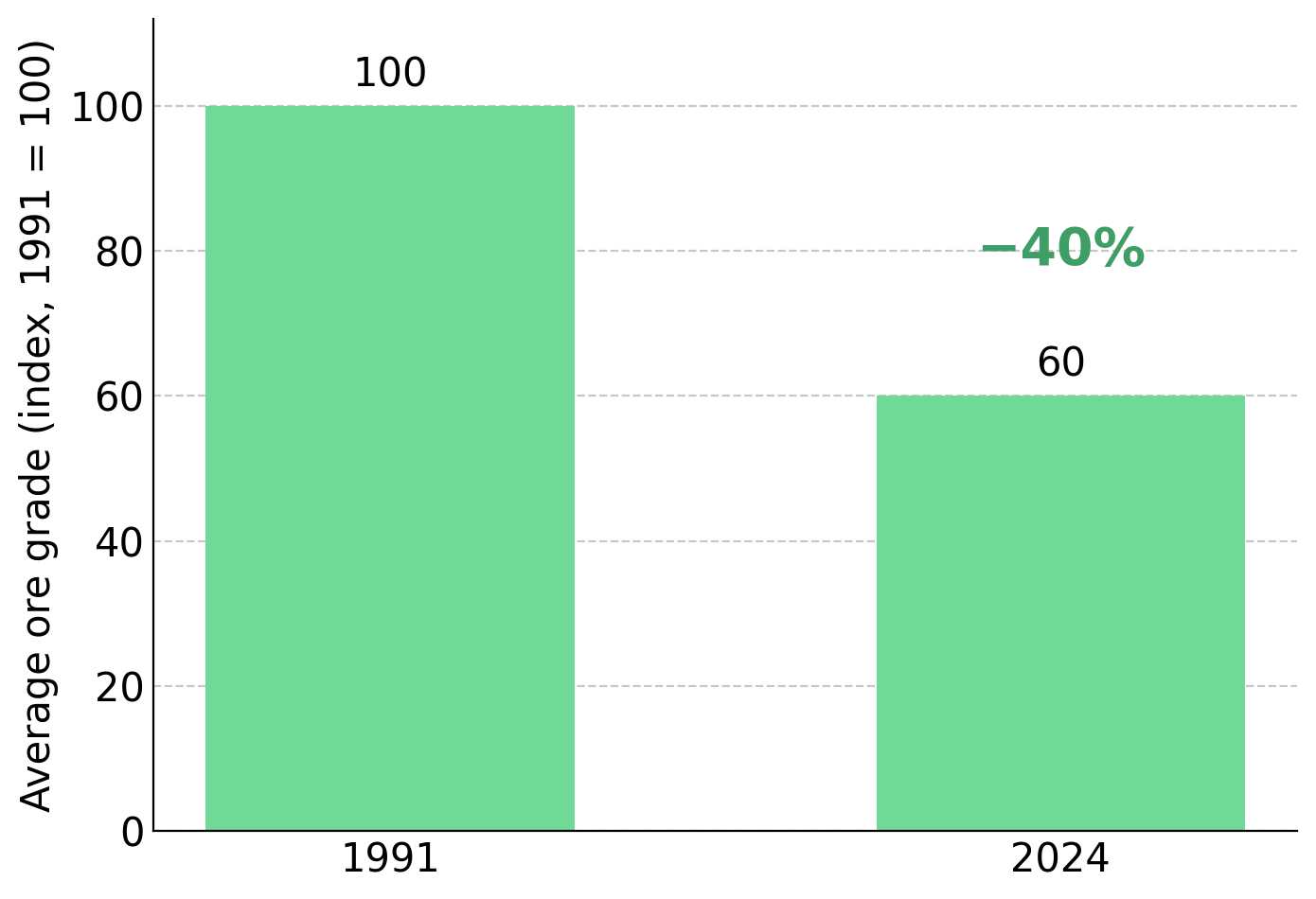

High copper prices typically encourage new mine development. In copper, long development timelines prevent supply from responding quickly. Greenfield mines typically take more than a decade to develop, ore grades have fallen roughly 40% since 1991 according to S&P Global, and capital requirements continue to rise as projects get deeper and more complex. The International Energy Agency estimates that existing and planned mines will meet only about 70% of projected 2035 demand. Demand growth from electrification, grid expansion, and artificial intelligence infrastructure is adding new copper consumption even at elevated prices, with J.P. Morgan estimated that data centers alone will add roughly 110,000 tonnes of demand in 2026.

Production growth has become harder to deliver as mature copper districts face declining grades, longer permitting timelines, and rising capital intensity. Merlin Marr-Johnson, Chief Executive Officer of Fitzroy Minerals, argues that the industry's challenge is maintaining output rather than adding new supply:

"Production growth within Chile, and in fact globally, is difficult; it's a very mature industry struggling to maintain production. All of this goes to show that copper prices have to re-rate."

Deposit Scarcity Increases the Value of Advanced Copper Projects

If the copper deficit reflects a shortage of new supply, investors should focus on pre-production companies with a credible path to production. Resource confidence influences valuation because it affects the likelihood that a deposit becomes a producing mine. Inferred resources carry the most uncertainty, indicated resources are better defined, and measured resources provide the highest level of confidence. A deposit dominated by inferred resources typically commands a lower valuation than a similarly sized project with defined economics and a clear permitting path.

As fewer large-scale copper discoveries enter the development pipeline, projects with district-scale resources become more valuable to producers seeking future supply growth. Jonathon Deluce, Chief Executive Officer and founder of Abitibi Metals, says the limited number of comparable assets is a key differentiator for B26:

"The consistency is how rare these deposits are in the marketplace. There are very few available across Canada that have the size and scale like B26."

Deposit Scarcity Increases the Value of Advanced Copper Projects

In a market short of new copper supply, development-stage projects with completed economic studies and financeable capital requirements command a premium. Investors assess project quality through NPV8, IRR, and AISC, which measure project value, expected returns, and operating costs. Together, these metrics determine whether a deposit can attract financing and advance toward production.

The Marimaca Oxide Deposit carries a post-tax NPV8 of about US$709 million at US$4.30/lb copper and roughly US$1.1 billion at spot prices, with an IRR of 31%-39% and first-five-year AISC near US$1.97/lb. Initial capital costs of about US$587 million and a balance sheet with roughly US$147 million in cash and no debt support the project's financing flexibility. Management argues that large, financeable copper projects are attracting growing interest from major mining companies seeking new supply.

Hayden Locke, Chief Executive Officer of Marimaca Copper, argues that assets meeting those criteria attract interest from the largest mining companies:

"If you start to deliver a project that has three to four to five million tons of contained copper in it, in the low coastal belt in Chile with access to infrastructure... that would grab the attention of just about every major mining company in the world, because all of them are desperate for copper exposure."

District-Scale Discoveries Gain Value as Copper Supply Tightens

Mogotes Metals' Filo Sur project in Argentina's Vicuña district adjoins Lundin Mining's Filo del Sol deposit and sits on the same structural trend as NGEx Minerals' Lunahuasi and Los Helados projects. During its inaugural 2025-2026 drill season, Mogotes reported two copper-gold-silver-molybdenum discoveries, including 86 metres at 0.7% copper, 0.55 g/t gold, 2.7 g/t silver and 169 ppm molybdenum from 108 metres at Albor, with mineralisation remaining open at depth. Discoveries at opposite ends of the property suggest mineralisation may extend across a larger project area, increasing the potential scale of future exploration targets.

Brownfield Restarts Deliver New Copper Supply Faster & at Lower Cost

Brownfield restarts can add copper supply faster and at lower cost than new mine builds. Selkirk Copper's planned restart of the Minto mine targets roughly 25% of comparable greenfield costs by reusing more than US$330 million of existing infrastructure, including a 4,100-tonne-per-day mill. Historic concentrate grades of 36%-40% copper, versus a global average of roughly 26%-28%, are especially valuable as treatment and refining charges approach zero and high-grade concentrate remains scarce.

M. Colin Joudrie, President and Chief Executive Officer of Selkirk Copper, highlighted how brownfield mines reduce capital requirements by hundreds of millions of dollars:

"It's a pre-production story with the benefit of low-cost capital; we'll probably be coming in at about 25% [of a greenfield build] to produce the copper we're targeting. If we had to do that in a greenfield setting today, you're probably looking at 800 to 900 million dollars US to get it back into production."

Capital Efficiency Becomes a Competitive Advantage for Copper Projects

When financing is scarce, capital requirements and project design matter as much as grade. Shared or existing processing infrastructure can reduce upfront capital requirements. Fitzroy Minerals plans to process oxide ore through a partner's existing solvent extraction and electrowinning plant, avoiding the cost of building its own processing facility. By-product credits can lower copper production costs by adding revenue from a second metal.

Cobra Resources believes Manna Hill's shallow oxide mineralization could support a lower-capital development pathway before transitioning to conventional sulfide processing. Early-stage heap leach production could reduce upfront funding requirements while the broader resource is expanded, a significant advantage at a time when large greenfield copper projects face increasing capital intensity.

Rupert Verco, Managing Director of Cobra Resources, highlighted the project's potential staged development approach:

"What that really means from an economic standpoint is you've probably got a low cost low capex startup treating its heap leach for copper and possibly gold in some of the higher grade zones. And then you have a standard flotation circuit to treat your primary sulfide mineralization."

The Key Risks to a Multi-Year Copper Deficit

The main risk to the copper-deficit thesis is any development that increases supply or weakens demand. Chinese refined-copper demand fell about 8% year over year in Q4 2025, while short positioning on the Shanghai Futures Exchange reached its widest level since 2021; if Chinese demand remains weak, the deficit could narrow. London Metal Exchange net long positions are near the 80th percentile, while StoneX models a 2026 average copper price of about US$11,490/t, suggesting prices could retreat if investor positioning weakens.

Faster-than-expected mine restarts could reduce the projected copper deficit. If Grasberg or other disrupted mines restart ahead of schedule, the supply shortfall could narrow. Project-level risks include permitting approvals, licence amendments, assay and logistics delays, unfinished technical studies, and financing that has not yet been secured. Each can delay the transition from resource definition to production.

Pre-production miners are pre-revenue investments exposed to dilution, permitting delays, and commodity-price volatility. None of the companies discussed is generating operating cash flow today; their valuations depend on permitting, financing, exploration, and development milestones.

Supply Constraints Still Point to a Multi-Year Copper Deficit

The copper deficit reflects constrained supply rather than excessive demand. Mine supply is concentrated, aging, and slow to replace, while new mines take more than a decade to build. At the same time, electrification, grid expansion, and artificial intelligence infrastructure continue to add copper demand even at higher prices.

Copper is trading near record levels, but new supply still has to be developed. High copper prices cannot accelerate permitting, financing, or construction enough to meet projected demand. The key constraint is now the development pipeline, where future mine approvals, financing, and construction will determine whether the deficit narrows or persists.

The Investment Thesis for Copper

- Copper provides exposure to demand growth from electrification, grid expansion, and artificial intelligence infrastructure, sectors that continue to add consumption even at higher prices.

- Mine disruptions, declining ore grades, and a limited pipeline of new projects are slowing supply growth, increasing the likelihood of a multi-year copper deficit.

- Development-stage projects with completed economic studies, defined capital requirements, and a credible permitting path are attracting capital because they are more likely to reach production.

- Brownfield restarts and low-capital processing strategies can add copper supply faster and at lower cost because they reuse existing infrastructure and reduce upfront capital requirements.

- Explorers that define large, high-grade deposits become more attractive acquisition targets as producers seek new resources to replace declining reserves and future production.

- Explorers that define large, high-grade deposits become more attractive acquisition targets as producers seek new resources to replace declining reserves and future production.

- Permitting approvals, financing, and project economics will determine which producers, developers, and explorers advance toward production and which face delays.

Copper's deficit now reflects a shortage of new supply rather than a shortage of demand. Because a single mine disruption can affect global supply, investors are placing greater value on projects that can add new copper production, whether through development-stage assets, brownfield restarts, new discoveries, or lower-cost production models. The investment opportunity lies in companies that can advance new copper supply toward production while managing the permitting, financing, and demand risks that could narrow the deficit.

TL;DR

Mine disruptions, declining ore grades, and a limited pipeline of new projects have turned copper's long-forecast deficit into a realized supply shortfall. Existing and planned mines are expected to meet only about 70% of 2035 demand, while electrification, grid expansion, and AI infrastructure continue to increase consumption. As a result, investors are assigning greater value to development-stage projects, brownfield restarts, and exploration assets with credible paths to production. The key investment opportunity lies in companies that can advance new copper supply toward production, though permitting, financing, weaker Chinese demand, and faster-than-expected mine restarts remain important risks.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed