Dollar Debasement Fears & Geopolitical Export Controls Drive Strategic Repricing in Critical Minerals

Dollar debasement and China's 92% rare earth refining control are repricing critical minerals. Permitted assets in allied jurisdictions now command security premiums.

- Expanding fiscal deficits and persistent real rate suppression are driving capital into hard assets, reinforcing a renewed monetary bid under critical minerals alongside gold and copper.

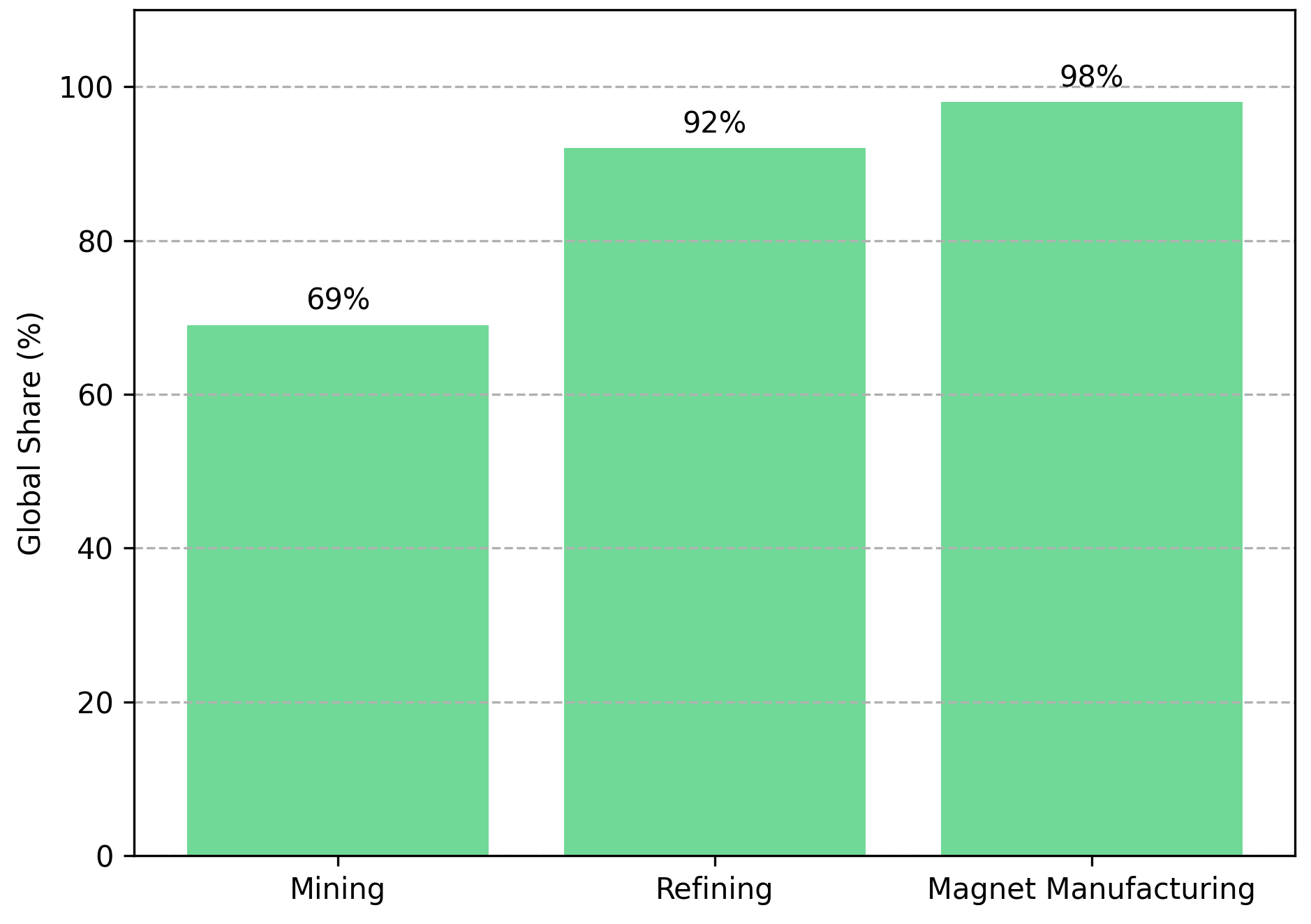

- China controls 69% of global rare earth mining and 92% of refining capacity. Expanded export curbs have transformed supply chains into instruments of geopolitical leverage.

- Paper market liquidity and options-driven volatility are amplifying price swings in battery metals, often obscuring structural deficits in sulphide nickel and heavy rare earth oxides.

- With eight-to-ten-year mine development timelines and five-plus-year refining buildouts, fully permitted or near-production assets in allied jurisdictions command a security premium.

- Companies such as Canada Nickel, Energy Fuels, Lifezone Metals, and Sovereign Metals illustrate how asset quality, cost positioning, and permitting visibility intersect with macro tailwinds.

Monetary Expansion, Real Asset Rotation & the Return of the Hard-Asset Bid

Persistent fiscal expansion across OECD economies has fundamentally altered capital allocation dynamics in commodity markets. Elevated sovereign debt-to-GDP ratios across major economies have coincided with structurally negative real interest rates that erode the purchasing power of fiat-denominated savings. Currency debasement concerns, once confined to emerging markets, have become a central consideration for institutional allocators managing long-duration liabilities.

This environment has reinforced allocation to tangible assets, extending the traditional precious metals bid into industrial commodities with strategic supply constraints. Nickel, copper, and rare earth elements are increasingly treated as both cyclical exposures and monetary hedges. Battery metals now trade partly on macro liquidity conditions rather than pure supply-demand fundamentals, creating pricing dynamics that reflect both industrial consumption forecasts and broader currency concerns.

When liquidity flows dominate futures and options markets, volatility expands accordingly. Industrial hedgers face short squeezes as delta hedging by dealers accelerates both upside and downside price movements. Reuters columnist Andy Home has documented the resulting margin hikes across exchanges, underscoring how paper market mechanics can diverge from physical market reality. For investors, the distinction between structural scarcity and speculative excess becomes critical when evaluating entry points.

Supply Chains as Strategic Instruments: The Geopolitical Reordering of Critical Minerals

Monetary tailwinds alone do not explain the repricing underway in critical minerals. China's dominant position across the rare earth value chain has transformed these materials from commodity inputs into instruments of geopolitical leverage. With 69% of global rare earth mining, 92% of refining capacity, and 98% of permanent magnet manufacturing, China's October 2025 expansion of export scrutiny has compounded supply concerns that were already acute.

Goldman Sachs estimates that a 10% disruption in rare earth supply would generate approximately $150 billion in global GDP impact, concentrated in electric vehicle production, defense systems, and grid infrastructure. Heavy rare earth elements, particularly dysprosium and terbium essential for high-temperature magnets in aerospace and defense applications, face the most severe supply constraints. NdPr oxide deficit projections continue to widen as demand growth outpaces committed supply additions.

The chokepoint in critical mineral supply chains is refining capacity, not mining alone. Long permitting windows of eight to ten years for new mining operations, combined with five-plus-year timelines for refining facility construction, create structural barriers to entry that existing producers leverage. Environmental approvals compound these delays, particularly in jurisdictions with rigorous permitting frameworks. As a result, assets outside China with integrated refining capability may command valuation premiums on enterprise value per tonne and enterprise value per resource metrics.

Volatility Versus Structural Scarcity: Distinguishing Liquidity Noise from Long-Term Deficits

The metals mania dynamic visible in exchange volumes does not negate underlying structural deficits. Dealer delta hedging mechanics and gamma squeezes amplify rallies and sell-offs alike, often squeezing industrial hedgers out of forward curves and distorting price signals. Yet long-cycle sulphide nickel projects and heavy rare earth refining capacity remain fundamentally underbuilt relative to projected demand growth through 2035.

Equity ownership in physical producers offers exposure beyond futures market whiplash. Companies with permitted assets, first-quartile cost structures, and near-term production visibility provide leverage to the structural deficit thesis without the mark-to-market volatility of derivatives positions. The challenge for investors is identifying which development-stage assets possess the combination of geological quality, permitting certainty, and financial capacity to reach production within commercially relevant timelines.

Nickel Sulphide Scarcity & the Premium on Tier-1 Development Assets

Indonesia's dominance in laterite nickel has reshaped the global supply curve, yet ESG and carbon intensity concerns have elevated the strategic value of sulphide deposits suited for battery-grade Class 1 nickel production. Sulphide processing generates substantially lower emissions than high-pressure acid leaching of laterites, creating a cost and compliance advantage for sulphide-focused developers in jurisdictions with carbon pricing mechanisms.

Canada Nickel's Crawford Project in Ontario holds the world's second-largest nickel reserve and resource, with March 2025 FEED results indicating an after-tax NPV at 8% discount of US$2.8 billion and internal rate of return of 17.6%. The project's net C1 cash cost of US$0.39 per pound and all-in sustaining cost of US$1.54 per pound position it in the first quartile of the global cost curve. The Environmental Impact Statement was filed in November 2024, with federal permits and full financing package targeted for 2026 and a construction decision by late 2026. The project has been referred to the Government of Canada's Major Projects Office. The company's IPT Carbonation and NetZero Metals initiative directly addresses the carbon intensity differentiation between sulphide and laterite processing.

The Canadian government's commitment to critical mineral development has accelerated permitting pathways and attracted sovereign capital. Mark Selby, Chief Executive Officer of Canada Nickel, describes the institutional support:

"The Major Projects Office is going to go out on behalf of their project portfolio and start to develop those relationships. To a sovereign wealth fund, they can say: if you're looking to deploy a couple billion dollars in a critical mineral sector in Canada, we've got a bunch of vetted projects that the country is firmly behind. Would you like to co-invest with us?"

Permitting certainty in Ontario contrasts with frontier jurisdictions where regulatory timelines remain unpredictable. For institutional investors, the combination of first-quartile AISC positioning and governmental alignment provides downside protection during periods of price volatility.

Rare Earth Refining: The Strategic Chokepoint in the Energy Transition

Mining capacity outside China is insufficient without corresponding refining infrastructure. Heavy rare earth elements remain critical for high-temperature permanent magnets in aerospace, defense, and electric vehicle applications, yet refining buildouts require five-plus-year timelines from initial permitting to commercial operation. The capital intensity and technical complexity of separation circuits have historically concentrated this value chain segment in China.

Energy Fuels operates the White Mesa Mill, the only facility in the United States able to process monazite for production of rare earth oxides. The company is actively processing alternate feed materials and targets commercial production of heavy rare earth oxides in late 2026. The Donald Project contributes an NPV of US$1.8 billion at a 10% discount rate. The October 2025 completion of a $700 million convertible note, which was oversubscribed by more than seven times, combined with liquidity of approximately $300 million as of September 2025, provides substantial financial capacity to execute the rare earth expansion.

The by-product monazite model reduces capital intensity compared to greenfield rare earth development, bypassing the eight-to-ten-year permitting window that constrains new entrants. Mark Chalmers, Chief Executive Officer of Energy Fuels, highlights the company’s dual advantage:

"We are like no other company in the critical mineral space. We're building a critical mineral hub using our longstanding uranium processing capabilities but also the ability to mine and recover rare earth."

The security premium attached to domestic refining capacity reflects both the permitting moat around existing licensed facilities and the strategic value of dysprosium and terbium supply outside Chinese export controls.

High-Grade Nickel & Vertical Integration: Sulphide Development Outside Dominant Producers

The need for high-grade sulphide resources outside Indonesia and China has elevated development-stage assets with proven geological quality and lower-emission processing pathways. Hydrometallurgical technology offers a cleaner alternative to traditional pyrometallurgical routes, with substantially lower primary energy requirements and reduced greenhouse gas emissions per tonne of refined nickel.

Lifezone Metals' Kabanga Project in Tanzania, according to the July 2025 Feasibility Study, holds reserves of 52.2 million tonnes at 1.98% nickel, with an AISC of $3.36 per pound, NPV at 8% discount of $1.58 billion, and internal rate of return of 23.3%. Final investment decision is targeted for 2026, supported by a partnership with the Government of Tanzania providing a 16% free carry interest.

The technological differentiation of hydrometallurgical processing addresses both environmental and cost considerations. Ingo Hofmaier, Chief Financial Officer of Lifezone Metals, describes the project’s technical advantage:

"Kabanga nickel deposit is one of the highest grade and best known undeveloped nickel assets around... Hydromet processing is a much better solution than going the old pyromet or smelter route with lots of primary energy… In our case it's a pressure cooker that is completely closed up and there's no emissions out of that process ultimately… The 4.1% copper equivalent grade is significantly higher than deposits like Resolution or Kamoa-Kakula.... "

First-quartile cost curve positioning and elevated IRR sensitivity to nickel price scenarios create asymmetric return potential. Jurisdictional risk in Tanzania requires consideration against the geopolitical alignment advantages of non-Chinese supply.

Multi-Mineral Leverage & Heavy Rare Earth Exposure at Near-Zero Incremental Cost

Heavy rare earth scarcity has intensified Western strategic engagement in Africa, where several large-scale deposits offer by-product recovery economics that improve all-in sustaining cost profiles. The ability to extract multiple critical minerals from a single ore body reduces single-commodity price risk while capturing the security premium attached to each strategic material.

Sovereign Metals' Kasiya Project in Malawi hosts a large-scale rutile deposit with a substantial graphite resource and heavy rare earth-rich monazite recoverable as a by-product at near-zero incremental cost. Rio Tinto maintains a strategic investment, while the International Finance Corporation has signed a Collaboration Agreement providing environmental and social expertise and securing rights to act as lender, mandated co-lead arranger, or investor for project financing. The ore body is hosted in a soft, friable saprolite that enables free-dig mining with simple processing requirements compared to fresh rock projects. The company continues to advance the Kasiya definitive feasibility study, with new workstreams adopted to align with potential lender requirements.

Ben Stoikovich, Chairman of Sovereign Metals, quantifies cost advantages:

"Our incremental cost to produce a ton of graphite as a byproduct from the Kasiya project will only be $241 US per ton. We're at the very bottom where other projects can't make money in the current market. We'd be selling graphite at a 50% operating margin even if we only sold into the lower value battery graphite market."

Multi-commodity exposure reduces single-metal risk, while by-product economics improve the AISC profile across all recovered materials.

Risk Considerations: Permitting, Capital Intensity & Volatility Management

Development-stage critical mineral assets carry execution risks that require explicit consideration. Mine development timelines of eight to ten years create exposure to commodity price cycles, with capital expenditure escalation risk during construction phases. Refining facility cost overruns have historically affected projects across the rare earth value chain, while currency volatility can materially alter project economics for non-dollar-denominated expenditures.

NPV sensitivity to discount rate shifts warrants attention, as rising risk-free rates compress present values of long-dated cash flows. IRR leverage to metal price creates asymmetric return profiles that benefit from price appreciation but amplify losses during cyclical downturns.

The Investment Thesis for Critical Minerals

- Permitted or producing assets outside China command strategic valuation support as security premia become embedded in institutional allocation frameworks.

- First-quartile AISC projects such as Crawford and Kabanga maintain margin resilience during periods of price volatility when higher-cost producers face operating losses.

- Licensed processing capacity at facilities like White Mesa bypasses multi-year permitting delays that constrain new market entrants.

- Projects like Kasiya provide diversified exposure across rutile, graphite, and rare earth elements, reducing single-commodity concentration risk.

- Hard-asset exposure aligns with dollar debasement risk and long-cycle infrastructure demand driven by electrification and defense priorities.

- Development timelines aligned with multi-year demand growth trends position near-FID assets to benefit from projected supply deficits in the late 2020s.

Monetary expansion continues to fuel capital rotation into hard assets, while geopolitical constraints limit the supply response that historically moderated commodity price cycles. Refining bottlenecks persist despite announced capacity additions, as five-plus-year buildout timelines lag demand growth projections. Futures market volatility obscures but does not eliminate the structural deficits developing across sulphide nickel, heavy rare earth elements, and battery-grade graphite.

The repricing underway reflects not a speculative spike alone, but a structural realignment of capital toward secure supply chains in allied jurisdictions. Development-stage and producing assets with first-quartile cost structures, permitting visibility, and strategic partnerships warrant deeper due diligence as the security premium becomes embedded in valuation frameworks.

TL;DR

Persistent fiscal deficits and negative real interest rates are driving institutional capital into hard assets, extending the traditional gold bid into strategic industrial commodities. China's dominant position across the rare earth value chain—controlling 69% of mining and 92% of refining capacity—has transformed critical minerals into instruments of geopolitical leverage, with October 2025 export curbs compounding supply concerns. Paper market volatility driven by dealer hedging mechanics obscures structural deficits in sulphide nickel and heavy rare earth elements that remain fundamentally underbuilt through 2035. With eight-to-ten-year mine development timelines and five-plus-year refining buildouts, fully permitted assets in allied jurisdictions with first-quartile cost structures now command valuation premiums as security considerations become embedded in institutional allocation frameworks.

FAQs (AI-Generated)

Expanding sovereign debt-to-GDP ratios and structurally negative real interest rates are eroding fiat purchasing power, driving capital rotation into tangible assets. Critical minerals now trade partly on macro liquidity conditions rather than pure supply-demand fundamentals, functioning as both cyclical industrial exposures and monetary hedges against currency debasement.

China controls 69% of global rare earth mining, 92% of refining capacity, and 98% of permanent magnet manufacturing. Goldman Sachs estimates a 10% supply disruption would generate approximately $150 billion in global GDP impact across electric vehicles, defense systems, and grid infrastructure—giving China significant leverage through export controls.

Sulphide processing generates substantially lower carbon emissions than high-pressure acid leaching required for laterite nickel, creating cost and compliance advantages in jurisdictions with carbon pricing. ESG considerations and battery-grade Class 1 nickel requirements have elevated sulphide deposits despite Indonesia's dominance in lower-cost laterite production.

Assets outside Chinese control with permitting visibility, first-quartile cost structures, and near-term production timelines command valuation premiums as institutional allocators prioritize supply chain security. Licensed refining capacity in allied jurisdictions bypasses multi-year permitting delays, creating structural barriers that support premium valuations.

Eight-to-ten-year development timelines create exposure to commodity price cycles and capital expenditure escalation. NPV sensitivity to discount rate shifts compresses valuations when risk-free rates rise, while currency volatility affects project economics for non-dollar expenditures. Refining facility cost overruns have historically affected projects across the value chain.

Analyst's Notes

Subscribe to Our Channel

Stay Informed