Energy Supply Disruptions & Bank of Canada Rate Expand Gold & Uranium Equity Valuations

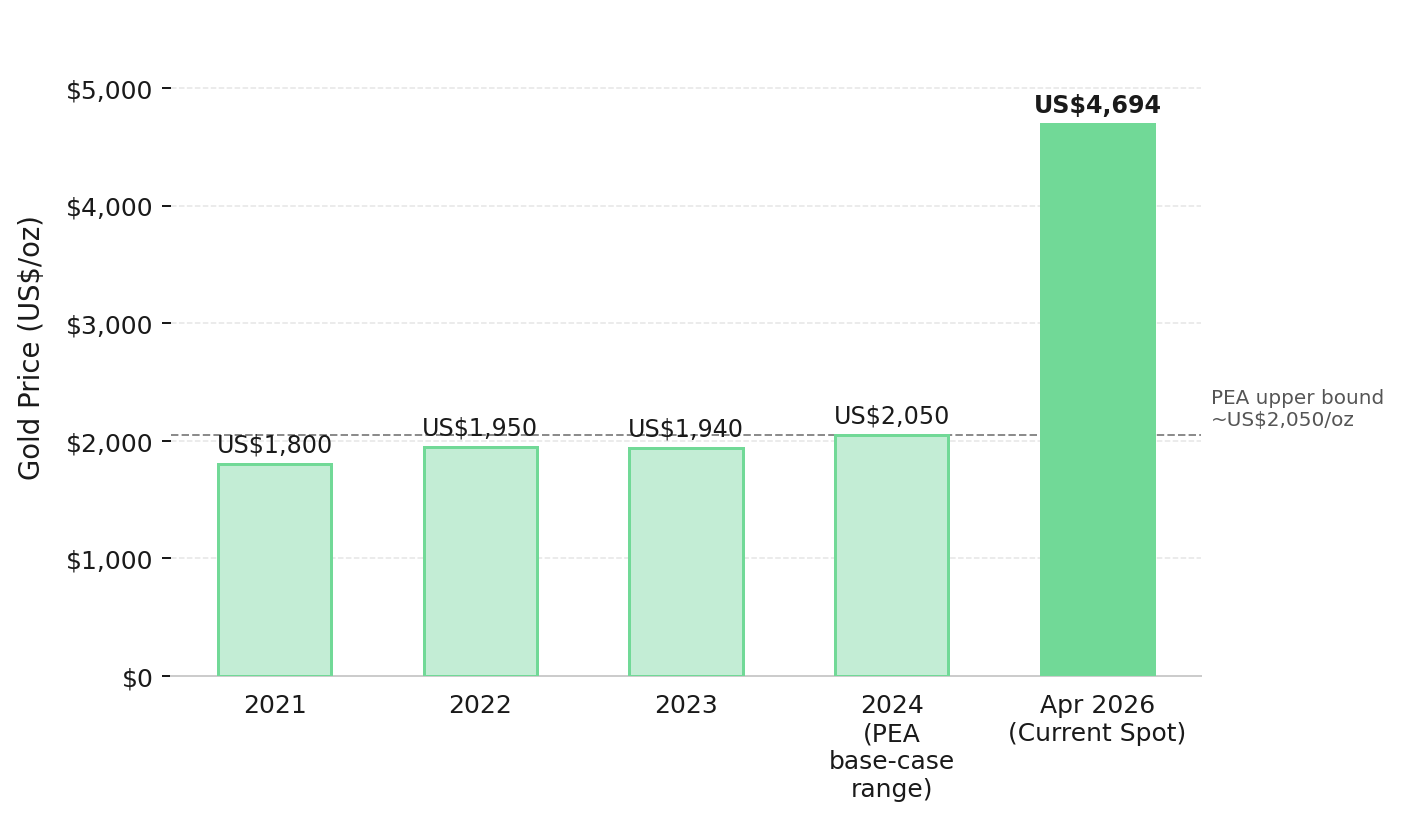

Strait of Hormuz crisis drives gold to US$4,694/oz and uranium above US$85/lb, reshaping NPV for Canadian junior gold and uranium explorers and developers.

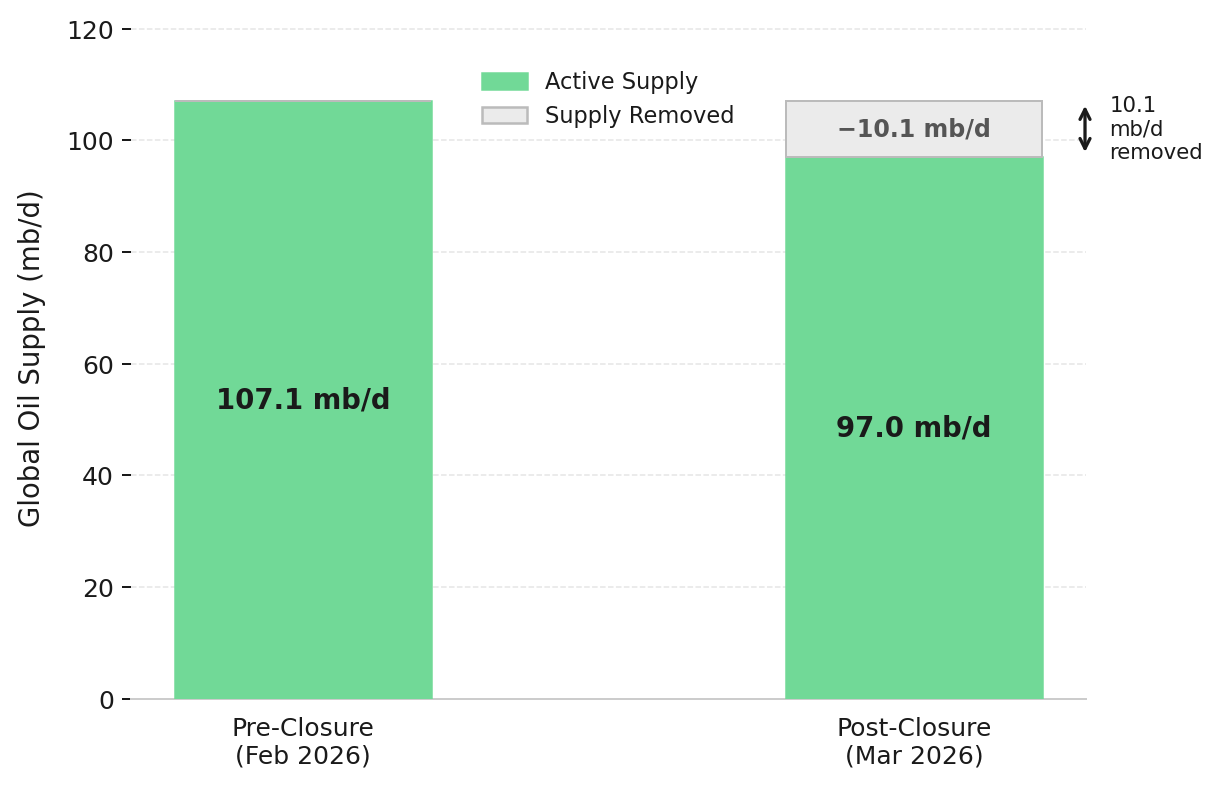

- The effective closure of the Strait of Hormuz since February 2026 has triggered the largest oil supply disruption in recorded history, removing approximately 10.1 million barrels per day from global markets and catalyzing a repricing of energy-adjacent hard assets.

- Gold at approximately US$4,694 per ounce and uranium at approximately US$86 per pound are responding to a collapse in energy security confidence, not inflation expectations alone, changing the net present value calculus for undeveloped resource projects globally.

- The Bank of Canada's rate held at 2.25% against Canada's Consumer Price Index at 2.4% and GDP forecast at 1.2% for 2026 creates a paradox for Canadian resource equities: financing conditions remain accessible, but construction cost inflation pressures are rising in parallel.

- Prime Minister Carney's April 21 Canada-US-Mexico Agreement Advisory Committee launch and the Alberta-British Columbia pipeline Memorandum of Understanding signal a Canadian federal posture aligned with large-scale resource development, reducing the regulatory risk premium for projects in the permitting pipeline.

- Canadian gold and uranium explorers and developers with de-risked assets, funded balance sheets, and near-term catalysts are positioned to capture the re-rating that historically follows a sustained commodity price shock of this magnitude.

On February 28, 2026, the US and Israel launched military operations against Iran, prompting the Iranian Revolutionary Guard Corps to mine the Strait of Hormuz, the 34-kilometer chokepoint through which approximately 20% of the world's seaborne oil trade previously passed. As of April 27, 2026, West Texas Intermediate crude traded at US$96.37 per barrel, gold closed at US$4,693.70 per ounce, and uranium spot prices held between US$85 and US$86 per pound. Canada's Consumer Price Index rose to 2.4% in March against a GDP growth forecast of 1.2%, per the Bank of Canada's January 2026 Monetary Policy Report. These figures are simultaneous expressions of a repricing of energy security as a scarce, finite input to the global economy.

Energy Supply Disruptions Reprice Global Energy Assets

The International Energy Agency reported in its April 2026 Oil Market Report that global oil supply fell by 10.1 million barrels per day to 97 million barrels per day in March, the largest monthly disruption on record. OPEC+ production declined 9.4 million barrels per day month-over-month as Middle Eastern infrastructure damage compounded the closure. A short-lived ceasefire briefly restored limited tanker traffic before the United States imposed a naval blockade on Iranian ports on April 13, 2026, and Iran re-closed the strait. IEA Executive Director Fatih Birol described the situation as the "largest energy security threat in history."

Oil Supply Shocks Drive Gold & Uranium Demand Repricing

Gold's safe-haven premium expands when energy-driven inflation erodes real yields. The Bank of Canada's decision to hold rates at 2.25% against a Consumer Price Index of 2.4% in March, a policy rate below inflation in real terms, is the condition that sustains institutional allocation to gold. Uranium's transmission is rooted in policy: nations that relied on Persian Gulf supply are accelerating nuclear capacity commitments at the sovereign level, generating a demand that does not reverse with a diplomatic resolution the way oil prices would. South Korea's April 2026 recommitment to nuclear expansion shifted utility-level uranium procurement from a policy preference to a national security imperative.

Gold at US$4,700 Reprices Undeveloped Project Economics

At US$4,694 per ounce, gold trades at 2.6 times the price level at which most junior developer preliminary economic assessments were built between 2021 and 2023. In projects with low all-in sustaining costs, net present value can expand by more than 100% for every US$1,000 per ounce increase in the gold price assumption. The result is enterprise value per ounce compression: a growing gap between current market capitalizations and in-situ values implied by revised economic models.

New Found Gold completed a preliminary economic assessment at Queensway in July 2025 at gold price assumptions now more than US$2,000 per ounce below current spot. Hammerdown is in production ramp-up, feeding the Pine Cove mill at 700 tonnes per day with expansion capacity targeting 1,400 tonnes per day for Queensway's Phase 1 material. On April 27, 2026, the company closed a CAD $115,055,200 bought deal financing including full exercise of the underwriters' over-allotment option, with co-lead orders from Eric Sprott, maintaining an approximately 19% shareholding, and EdgePoint Investment Group.

Keith Boyle, Chief Executive Officer of New Found Gold, frames the production-stage economics at current gold prices:

"The first couple of years we're looking at about 100,000 oz a year at an all-in sustaining of about $1,300. So, you do the quick math on that and that's 300 plus million dollars of cash flow a year on that basis."

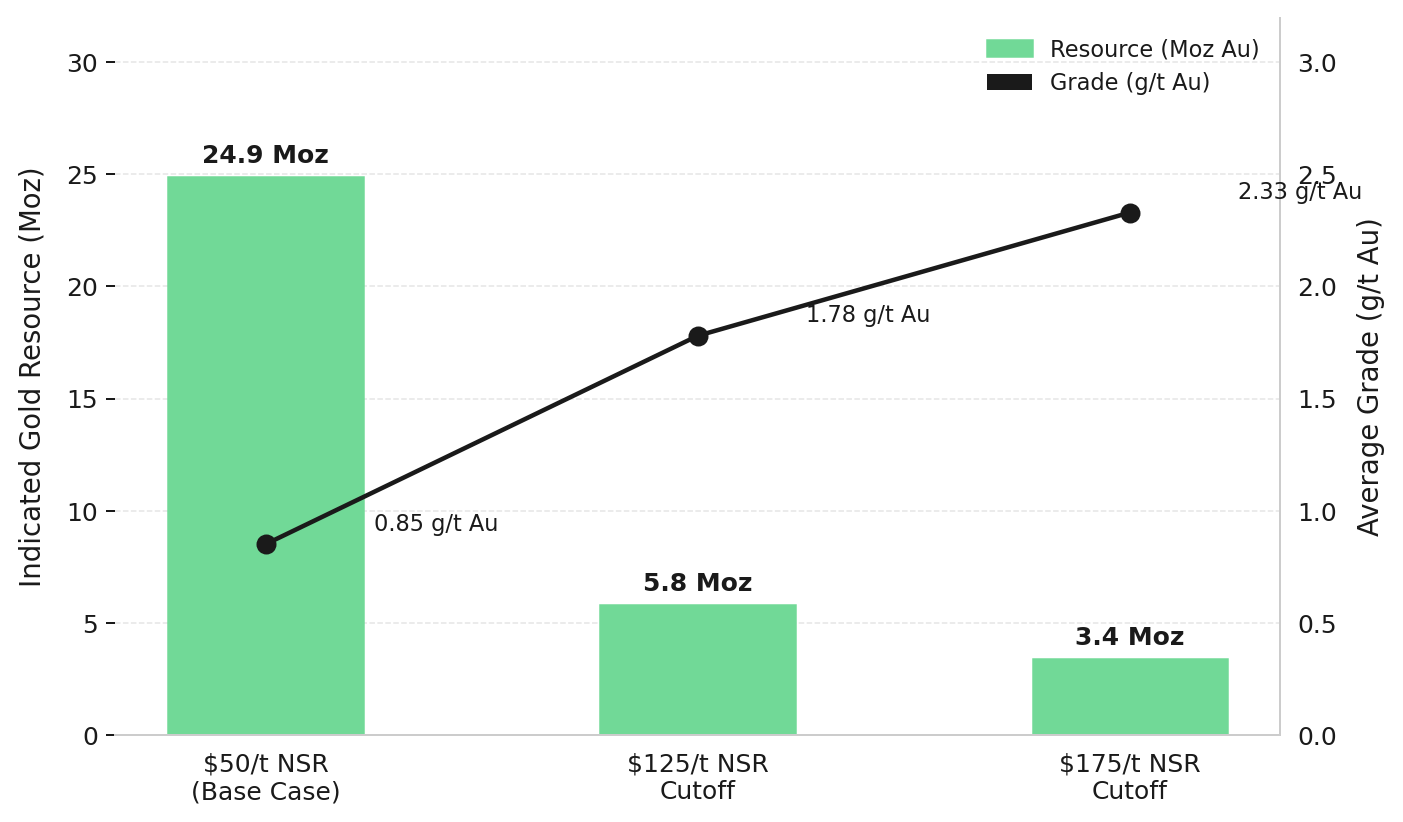

Higher-Grade Underground Mine Plans Gain Economic Priority

As the net smelter return cutoff rises, resource tonnage contracts but grade concentrates, producing a smaller but more economically viable target for underground development.

Tudor Gold holds total Indicated Mineral Resources of approximately 28.9 million gold-equivalent ounces. At the US$125 per tonne net smelter return cutoff, the Indicated resource concentrates to 5.8 million ounces at 1.78 grams per tonne gold. Tudor's market capitalisation of approximately C$548.74 million as of March 2026, measured against 24.9 million ounces of Indicated gold, reflects neither the current gold price nor the preliminary economic assessment on an underground mining scenario currently underway, which will deliver the Goldstorm Deposit's first formal net present value and internal rate of return framework.

Joseph Ovsenek, President and Chief Executive Officer of Tudor Gold, ties the grade concentration directly to the development path being advanced:

"What we're focused on is this higher grade underground mine, say targeting that 3 g or better material to start with and come up with say an 8 to 10,000 ton per day underground mine, capex a billion, billion and a half. That's something we can handle. We can build that mine. We don't need help from anyone else and that's something we can push ahead to production."

Energy Security Risks Accelerate Uranium Procurement Demand

Uranium spot prices at approximately US$86 per pound represent a 15% decline from the January 2026 high of US$101.41 but remain approximately 7% above the year's opening price. The long-term contract price has continued moving higher as utilities return to procurement after a period of deferral. The Hormuz crisis has converted sovereign nuclear policy commitment into utility procurement urgency with multi-decade horizons, a demand signal insulated from near-term spot volatility.

ATHA Energy controls 100% of the Angikuni Basin in Nunavut and holds a national land package of 6.8 million acres across Canada's most active uranium basins. The company retains a 10% free-carried interest in Athabasca Basin exploration projects operated by NexGen Energy and IsoEnergy, providing Saskatchewan discovery exposure at no additional cost to shareholders. ATHA closed a CAD $63 million financing in February 2026, including a cornerstone investment by Queens Road Capital Investment.

Troy Boisjoli, Chief Executive Officer of ATHA Energy, addresses the setup and ATHA's positioning within the current uranium cycle:

"The macro environment in the uranium sector is unequivocally unlike any time I've seen in my career. The sentiment, the real demand that's being built up, coupled with some of the supply side risk, is a setup, a structural setup, like we have not seen in the uranium space. Being in control of a district like we're in has us in a very good position of strength relative to the market and relative to our strategic opportunities and the availability to advance this forward in a timeline that is relevant to this uranium cycle."

District-Scale Uranium Discoveries Gain Strategic Value

ATHA's 2026 exploration program at Angilak deploys three simultaneous diamond drill rigs, the largest program in the project's history, commencing late April 2026. The 2025 program produced five new uranium showings including RIB North, where the maiden hole intersected 34.7 meters of composite uranium mineralization at peak grades of 8.16% uranium oxide over 0.5 meters, more than eight times ATHA's internal high-grade threshold.

Canadian Policy Support Reduces Mining Regulatory Risk Premiums

Prime Minister Carney announced a 24-member Advisory Committee on Canada-US-Mexico Agreement Economic Relations on April 21, 2026, with its first meeting on April 27, ten weeks before the mandatory Joint Review begins on July 1. The Major Projects Office creates an expedited federal approval channel, and the Memorandum of Understanding with Alberta targeting a new pipeline to British Columbia's northwest coast signals federal-provincial alignment on resource infrastructure. British Columbia's April 9, 2026 decision to pause deliberation on the Mitchell Treaty Twin Tunnels permit amendment, pending legal certainty over mineral titles held by Tudor Gold, reflects the Canadian regulatory system's protection of recorded mineral claim holders. The Canadian dollar at 0.7345 against the United States dollar creates a revenue tailwind for companies receiving United States dollar commodity prices, though investors should model this against capital cost inflation for cross-border equipment procurement.

The Investment Thesis for Gold & Uranium

- Gold developers and emerging producers with preliminary economic assessments built at assumptions 40% to 60% below current spot carry materially understated net present values, creating a re-rating opportunity as updated studies reflect current prices.

- Developers with existing milling and tailings infrastructure carry lower effective capital intensity than greenfield projects, compressing the cash breakeven timeline and reducing execution risk at any gold price above the all-in sustaining cost.

- Exploration and development stage companies holding bulk-tonnage gold-copper deposits with identified higher-grade subdomains benefit disproportionately from the current high-price market, as underground selective mining scenarios marginal at US$1,800 per ounce become economically dominant at US$4,700 per ounce.

- Uranium explorers with district-scale land control in Canadian jurisdictions and free-carried interest structures providing Athabasca Basin exposure at zero marginal exploration cost are positioned to deliver discovery results into a demand market conditions driven by sovereign nuclear procurement urgency and rising long-term contract prices.

- The Carney government's Major Projects Office and Canada-US-Mexico Agreement Advisory Committee reduce the regulatory risk premium applied to Canadian mining equities in a way not yet reflected in junior equity valuations.

The Strait of Hormuz closure is not an oil market event from which gold and uranium have incidentally benefited. It is a repricing of the assumption that global energy supply chains are reliable, that central banks can manage inflation within narrow bands, and that the in-ground value of scarce resources is adequately reflected in current equity market capitalizations. Gold at US$4,694 per ounce and uranium at US$86 per pound are the market's forward-looking assessments of a world in which energy security has become a sovereign imperative. The actionable implication for investors is to identify the producers, developers, and explorers whose project fundamentals, treasury strength, jurisdictional positioning, and near-term catalysts are calibrated to this environment.

TL;DR

The closure of the Strait of Hormuz since February 2026 has removed 10.1 million barrels per day from global oil supply, triggering the largest energy shock in recorded history and driving gold to approximately US$4,694 per ounce and uranium to approximately US$86 per pound. These price levels are not primarily inflation responses, they reflect a repricing of energy security confidence that has fundamentally changed the net present value undeveloped resource projects. Canadian gold developers and uranium explorers with de-risked assets, funded treasuries, and near-term technical catalysts are positioned to capture the re-rating that follows a commodity shock of this scale, provided investors apply rigorous discipline to project-stage risk, financing structure, and jurisdictional variables.

FAQs (AI-Generated)

Gold and uranium respond to the Strait of Hormuz crisis through different but reinforcing mechanisms. Gold rises because energy-driven inflation erodes real yields, reducing the opportunity cost of holding a non-yielding monetary asset. When central banks, including the Bank of Canada, which held its policy rate at 2.25% against a Consumer Price Index of 2.4% in March 2026, maintain rates below the inflation rate, institutional capital rotates into gold as a store of value. Uranium rises for various reasons: nations that previously depended on Persian Gulf oil supply are now accelerating nuclear energy commitments at the sovereign policy level, driving long-term utility procurement demand that is largely insulated from near-term diplomatic developments. Both commodities are, in different ways, proxies for energy security, which is exactly what the Hormuz crisis has called into question.

Most junior gold developer preliminary economic assessments were built between 2021 and 2023 at gold price assumptions of roughly US$1,700 to US$1,900 per ounce. At US$4,694 per ounce, those studies understate net present value materially. In projects with all-in sustaining costs in the US$1,000 to US$1,400 per ounce range, the free cash flow per ounce produced more than doubles relative to the base-case assumption. The practical consequence is enterprise value per ounce compression: the market capitalization of many junior developers still reflects older price assumptions, while the economic reality has changed significantly. Investors should not rely on existing preliminary economic assessments at face value, they should recalculate implied net present values using current spot prices, current discount rates, and current capital cost estimates before drawing conclusions about whether a company is undervalued.

The Mitchell Treaty Twin Tunnels is a proposed underground infrastructure corridor that KSM Mining ULC, a subsidiary of Seabridge Gold, wants to route through the Treaty Creek Project area, including the Perfectstorm Zone, a discovery that Tudor Gold's management has characterized as having potential to exceed the Goldstorm Deposit in both tonnes and grade. British Columbia's Major Mines Office paused deliberation on the permit amendment on April 9, 2026, citing the absence of legal certainty over Tudor Gold's overlapping mineral titles. The decision maker indicated that resolution could come through either a negotiated agreement or a court ruling. Tudor Gold has filed two proceedings in the British Columbia Supreme Court and has stated a preference for a negotiated resolution. The three possible outcomes are: a negotiated settlement that compensates Tudor Gold or modifies the tunnel route; a court ruling affirming Tudor Gold's mineral title rights; or a protracted legal process that delays the Perfectstorm Zone's development timeline without necessarily affecting the Goldstorm Deposit or the preliminary economic assessment currently underway.

ATHA Energy's management has drawn explicit comparisons between the RIB North discovery at Angilak, which returned 34.7 meters of composite uranium mineralization at peak grades of 8.16% uranium oxide over 0.5 meters, and discovery-stage intersections at world-class Athabasca Basin deposits, including the Arrow deposit operated by NexGen Energy. The geological characteristics being cited include mineralization thickness, grade profile, and alteration signatures analogous to Athabasca-style unconformity-hosted deposits. However, investors must apply a critical distinction: no formal NI 43-101 Mineral Resource Estimate currently exists at Angilak, and the 2024 Exploration Target of 60.8 to 98.2 million pounds of uranium oxide at 0.37% to 0.48% uranium oxide is a conceptual range, not a certified resource. The key risks specific to this stage include the possibility that follow-up drilling fails to confirm the geometry, continuity, or grade of the RIB North system; that assay results diverge materially from radiometric data; and that the logistical complexity of operating in remote Nunavut introduces timeline and cost variables not present in Saskatchewan-based projects.

The Bank of Canada's decision to hold the policy rate at 2.25% on April 29, 2026, against a Consumer Price Index of 2.4% and with GDP forecast at just 1.2% for the year, creates a near-term financing environment that is broadly constructive for capital-intensive junior mining companies. Pre-revenue developers and explorers depend on equity and debt markets to fund exploration programs, feasibility studies, and construction. A rate hold preserves the cost of capital at levels that make project financing viable without excessive equity dilution. However, investors should monitor two scenario risks. First, Scotiabank has publicly modelled three rate hikes in the second half of 2026, which would raise the discount rate applied in net present value models and increase the cost of any new debt facility. Second, the Bank of Canada's April 29 Monetary Policy Report will be scrutinized for any signal that the Governing Council is prepared to respond to energy-driven inflation broadening into core goods and services, a shift in tone that would represent a tightening of financial conditions even without an immediate rate change.

Analyst's Notes

Subscribe to Our Channel

Stay Informed