Hormuz-Driven Energy Inflation & Federal Reserve Rate Holds Compress Gold Equity Valuations

Hormuz inflation blocks Fed rate cuts, compressing gold equities despite 23 months of central bank buying and US$5,400–$6,300 institutional year-end targets.

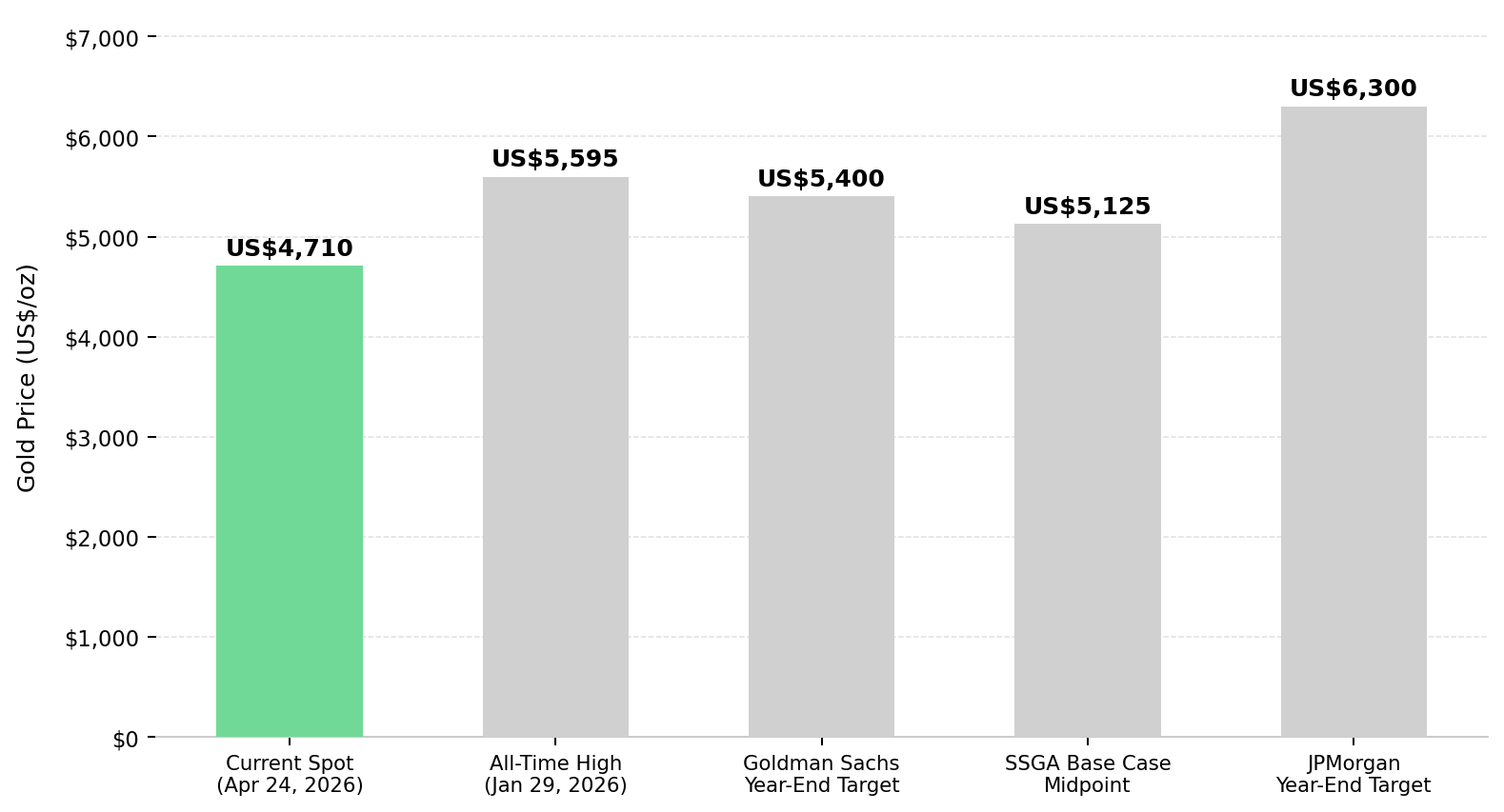

- Gold's correction to US$4,710 per ounce represents a cyclical repricing driven by elevated real yields, creating a valuation gap for institutional allocators.

- Disruptions in the Strait of Hormuz lifted March 2026 inflation to 3.3% year-over-year, blocking Federal Reserve rate cuts required to compress gold equity discount rates.

- Central banks purchased gold for 23 consecutive months, establishing a verifiable physical price floor secured between US$4,000 and US$4,100 per ounce.

- Tier-1 producers generate free cash flow trade at multiples calibrated to gold prices 45% to 88% below spot levels, embedding conservatism into equity pricing.

- Capital rotation away from non-yielding assets disproportionately impacts developers, creating an entry window for fully permitted projects with near-term construction schedules.

Energy Supply Shocks Elevate Real Yields and Divert Capital from Gold Equities

Gold closed April 24, 2026, at US$4,710 per ounce, representing a 15.9% contraction from the January 29 all-time high. The Strait of Hormuz is operating under a supervised pause, sustaining Brent crude at levels incompatible with the Federal Reserve achieving its 2% inflation mandate. Goldman Sachs Commodities Research warned that if the Strait remains restricted, Brent crude will average above US$100 per barrel throughout 2026, anchoring headline inflation and elevating real yields.

This energy-driven inflation increases the opportunity cost of holding non-yielding bullion, redirecting capital away from gold equities. Furthermore, the International Monetary Fund flagged the Iran conflict as a downside risk tightening global financial conditions.

Prolonged Fed Rate Holds Anchor Discount Rates for Mining Valuations

With the CME FedWatch tool pricing a 99.5% hold probability for the April 28 to 29 Federal Open Market Committee meeting, Jerome Powell's exit language before his May 15, 2026 term expiration becomes the sole market-moving variable. The March 2026 committee revised Personal Consumption Expenditures inflation upward to 2.7%, leaving at most one 2026 rate cut and anchoring elevated discount rates applied to gold equity net present values.

On April 24, the United States Department of Justice closed its formal probe of Jerome Powell, immediately sending Kevin Warsh's confirmation odds from 27% to 85% in a single institutional trading session. Gold's positive price response confirmed a Federal Reserve independence discount strictly embedded in bullion pricing. The April 30 first-quarter Gross Domestic Product release operates as the primary quantitative trigger for accelerating second-half easing expectations, as a below-consensus economic growth print would force the Federal Reserve to reconsider rate cuts.

Sustained Official Sector Accumulation Establishes a Verifiable Physical Price Floor

JPMorgan Global Research models 585 tonnes of quarterly demand in 2026, establishing a physical demand floor independent of Western exchange-traded fund flows. Poland, Kazakhstan, Uzbekistan, and Malaysia accumulated official sector reserves in early 2026, while China's reserves reached 2,309 tonnes. State Street Global Advisors identified China's purchases as the primary mechanism counteracting Western exchange-traded fund selling during the first-quarter price correction.

The structural demand model explains approximately 70% of quarterly gold price movements through verified buying tonnage. Every 100 tonnes of quarterly demand above the 350-tonne threshold equates to 2% of quarterly price appreciation, placing the hard support floor firmly between US$4,000 and US$4,100 per ounce. Institutional base cases project significant upside based on this demand profile, with Goldman Sachs Commodities Research holding a US$5,400 per ounce year-end 2026 target and JPMorgan Global Research modelling a high-conviction scenario reaching US$6,300 per ounce.

Conservative Pricing and Execution Risk Sustain Gold Equity Discounts

The rate-hold environment raises the opportunity cost of non-yielding bullion, suppressing Western exchange-traded fund inflows. Simultaneously, execution risk premiums related to construction schedules compress junior-to-mid-tier mining multiples independent of underlying commodity support. This creates pricing anomalies across producers and developers that project-level fundamentals do not justify.

Most published technical studies calculate net present values using base-case gold price assumptions between US$2,500 and US$3,250 per ounce, placing these financial models 45% to 88% below current spot pricing. As rate-cut expectations firm, these discount factors will compress, allowing equities to re-rate on fundamental cash flow generation parameters.

Fixed-Cost Leverage and Debt-Free Balance Sheets Expand Producer Cash Margins

Producer returns in the elevated real yield regime are exclusively generated by disciplined cost execution, on-schedule capital projects, and the avoidance of dilutive financings. Serabi Gold entered the second quarter of 2026 entirely debt-free with US$64.4 million in cash. The company trades at 1.9x enterprise value to EBITDA against a peer average of 3.1x, generating a 24% free cash flow yield while funding a US$5.0 million fourth ball mill entirely from existing operational cash flow.

Mike Hodgson, Chief Executive Officer of Serabi Gold, quantifies the fixed-cost leverage amplifying margin expansion at current gold prices:

"Between power, diesel, and labor, that's 65% of our costs… There's a big fixed cost component. We actually know what our costs are month on month. It's the revenue that's just going up and up and up with this gold price. And the margin is just expanding."

Capital Allocations in Tier-1 Jurisdictions Accelerate Free Cash Flow Generation

Integra Resources achieved a record 76,800 total tonnes per day mining rate in the first quarter of 2026 at the Florida Canyon Mine in Nevada, a jurisdiction ranked first globally in the 2025 Fraser Institute Annual Survey of Mining Companies.

George Salamis, President and Chief Executive Officer of Integra Resources, frames the specific production trajectory strategically embedded in current capital investment:

"2026 is about building capacity today at Florida Canyon to deliver more ounces, stronger cash flow, lower costs tomorrow. The guidance range looking out two years out to 80 to 90,000 ounces per year in 2027 and another 80 to 90,000 ounces in 2028 was a positive surprise."

Institutional Capital Availability De-Risks Commercial Production Timelines for Developers

Elevated real yields inherently increase project discount rates, making time to commercial production the central mathematical variable in resource equity valuation models . i-80 Gold issued a full notice to Hatch Engineering for the Lone Tree facility in the first quarter of 2026, backed by over US$1.0 billion in available capital.

Paul Chawrun, Chief Operating Officer of i-80 Gold, outlines the steady-state cash flow case realized once owner-operated processing replaces third-party toll milling operations:

"We'll have the Lone Tree plant producing gold by the end of 2027 with a bit of a ramp up in 2028. I think we estimated somewhere around 150 to 200 million net cash flow per year once it operates at somewhere in the range of $3,000 dollar gold."

Low-Capital Oxide Startups Provide Immediate Cash Flow to Fund District-Scale Expansion

Cabral Gold is advancing Phase 1 heap leach construction at 54% completion at the MG deposit in Para state, Brazil, targeting a first gold pour in the fourth quarter of 2026. The Pre-Feasibility Study reports an exceptional after-tax internal rate of return of 78% at US$2,500 per ounce gold against initial capital of US$37.7 million.

Alan Carter, President and Chief Executive Officer of Cabral Gold, identifies the oxide-first cash flow strategy directly driving corporate valuation:

"We are building an initial gold in oxide heap leach project which should mine about 3,000 tonnes a day. That will provide a significant amount of cash to allow us to develop the larger district, grow the global resource base and demonstrate the economic viability of the much larger phase two project."

Non-Dilutive Debt Financing Packages Validate Project Economics and Secure Construction Timelines

Jurisdictional quality operates as a first-order variable in net present value modelling under elevated real yields. New Found Gold successfully secured a US$205 million financing package closing in mid-April 2026 to advance the Queensway Gold Project in Newfoundland toward late 2027 production without requiring dilutive equity financing.

Keith Boyle, Chief Executive Officer of New Found Gold, outlines the specific production economics mathematically underpinning the institutional debt financing commitment:

"The first couple of years we're looking at about 100,000 ounces a year at an all-in sustaining of about $1,300. You do the quick math on that and that's 300 plus million dollars of cash flow a year on that basis."

Codified Permitting Frameworks Reduce Country Risk Premiums and Expand Net Present Values

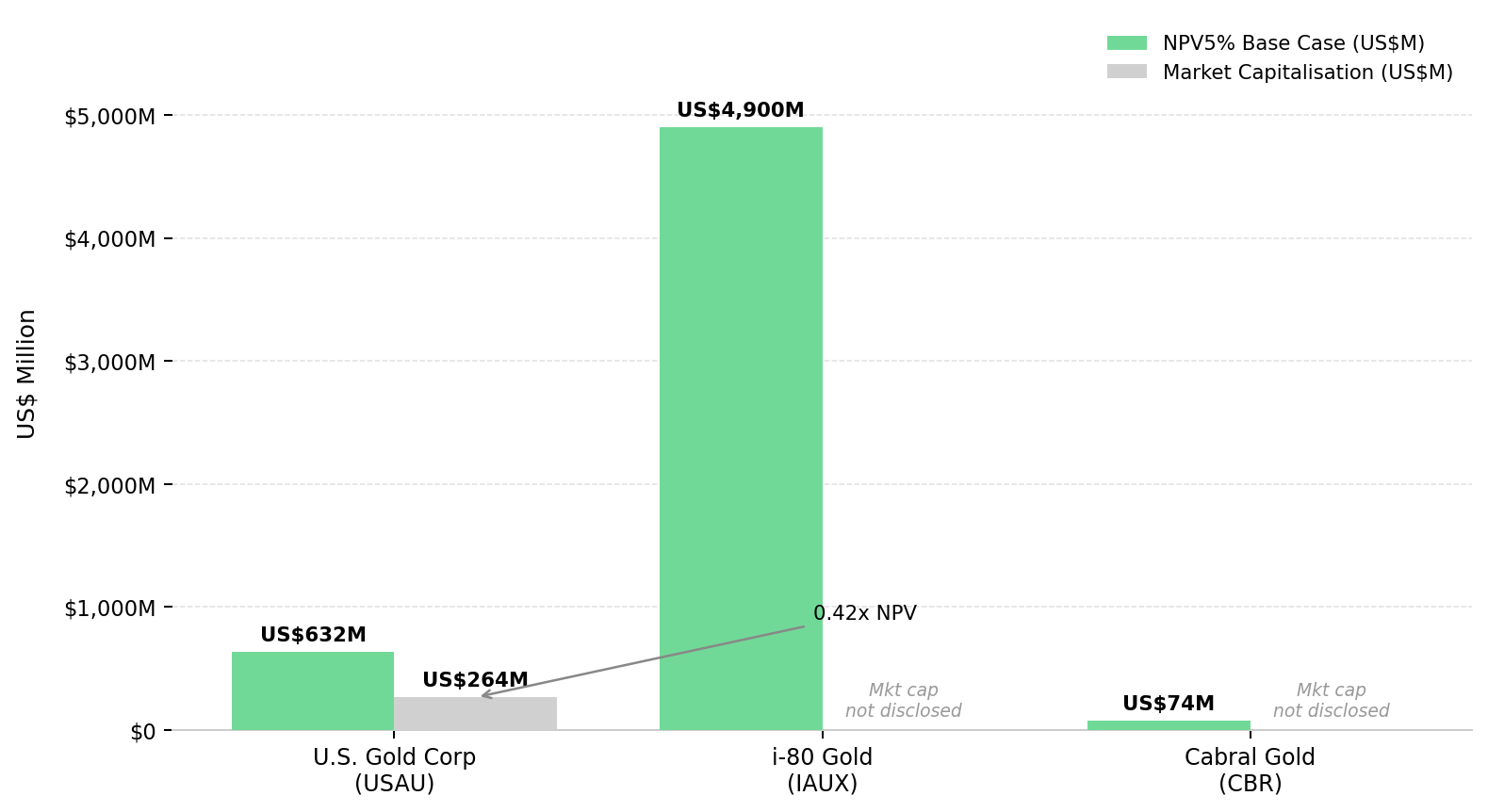

U.S. Gold Corp completed an April 2026 Definitive Feasibility Study for the fully permitted CK Gold project in Wyoming, definitively reporting an after-tax net present value of US$632 million, which geometrically rises to approximately US$1.4 billion at US$4,500 per ounce gold. The project strategically holds all required federal and state permits, which are fundamentally non-revocable under Wyoming state law.

Luke Norman, Executive Chairman of U.S. Gold Corp, quantifies the project finance environment for a fully permitted and globally shovel-ready asset:

"There's a lot of money out there right now chasing mining opportunities with not a lot of projects like ours that are shovel ready. That 400 million dollars is a sweet spot. We think we're walking into a pretty friendly environment for mining financing right now."

High-Grade Resource Delineation Optimizes Operational Mine Sequencing and Institutional Indexing

Hycroft Mining Holding Corporation officially targets an Initial Assessment Technical Report in the second quarter of 2026 to systematically transition its Nevada mine to high-margin sulfide milling. The company formally joined the VanEck Junior Gold Miners exchange-traded fund in April 2026, increasing institutional indexing exposure.

Diane Garrett, President and Chief Executive Officer of Hycroft Mining, explains the rationale for prioritising the Brimstone and Vortex high-grade silver systems to heavily optimize production:

"Nobody thought there was high-grade at Hycroft. This is the game-changer. They are 100% in agreement that what we need to do is keep drilling and expanding these high-grades."

Systematic Resource Conversion Shortens Institutional Development Timelines and Capital Pathways

With total global gold mine supply growing only 1% in 2025, institutional capital is preferentially allocated to exploration programs that systematically convert resources from inferred to indicated classification. Tudor Gold physically hosts 24.9 million indicated ounces at the Treaty Creek Goldstorm Deposit in British Columbia, advancing a preliminary economic assessment alongside a 10,000-metre 2026 drill program.

Joseph Ovsenek, President and Chief Executive Officer of Tudor Gold, details why the high-grade component systematically enables a manageable capital pathway:

"Within that resource we actually have some higher grade mineralisation in that 2 to 3 to 4 gram range. And that's what we can use to accelerate and move Treaty Creek into production quicker than say another lower grade opportunity."

Favorable Metallurgical Characteristics Support Phased Capital Execution and Primary Sulfide Extraction

Cobra Resources is advancing the Manna Hill copper-gold project in South Australia and independently confirmed continuous mineralisation across 750 meters of strike. Preliminary metallurgical work strictly supports a low-capital heap leach startup ahead of a flotation circuit for primary sulfide ore.

Rupert Verco, Managing Director of Cobra Resources, details the molybdenite intercept successfully confirming the underlying porphyry system:

"We have standalone molybdenite intersections of up to 10 to 12 meters at 0.1% which is pretty high grade and that's showing us that we're in a very fertile porphyry system."

Accelerated Mineral Resource Estimates Eliminate Stage-Gate Delays and Fast-Track Feasibility Decisions

P2 Gold received a C$7.5 million placement to advance the Gabbs project securely situated directly on Nevada's Walker Lane Trend. The critical capital injection fully funds an updated Mineral Resource Estimate strictly targeting the third quarter of 2026.

Joe Ovsenek, President and Chief Executive Officer of P2 Gold, directly links the upcoming resource estimate to the accelerated corporate feasibility schedule:

"We'd like to get a resource estimate out by the end of the summer, and that will feed right into our schedule to have that feasibility done by year end."

The Investment Thesis for Gold

- Exposure to monetary diversification and verifiable central bank accumulation establishes a definitive physical price floor.

- Jurisdictions offering regulatory stability and permitting transparency reduce country risk premiums applied to long-dated project cash flows.

- Favorable cost structures supported by debt-free balance sheets allow producers to self-fund capacity expansions without relying on dilutive equity financing.

- Development timelines aligned with multi-year demand growth trends isolate value creation from near-term exchange-traded fund pricing volatility.

- Permitted asset expansions with low initial capital expenditure intensity provide asymmetric leverage to elevated commodity spot prices.

- District-scale exploration that converts inferred geological material to indicated classification directly advances definitive feasibility decisions.

Gold at US$4,710 per ounce represents a commodity market in transition rather than distress. The 15.9% pullback is cyclically tied to Hormuz-driven energy inflation and the resulting Federal Reserve rate-hold, which elevates real yields and temporarily suppresses equity multiples. A structural demand floor verified by 23 consecutive months of sovereign central bank purchasing secures base-case project economics across the mining lifecycle. The normalisation of global inflation data will unlock the Federal Reserve rate cuts necessary to compress institutional discount rates, providing leveraged upside as institutional capital rotates back into the precious metals sector.

TL;DR

Gold's 15.9% pullback from its January 2026 all-time high is a cyclical repricing caused by Hormuz-driven energy inflation, which pushed United States Consumer Price Index inflation to 3.3% and blocked Federal Reserve rate cuts. Despite this headwind, a structural price floor between US$4,000 and US$4,100 per ounce is mathematically defended by 23 consecutive months of central bank purchasing. Meanwhile, gold mining equities remain systematically mispriced. Execution risk premiums and highly conservative base-case price assumptions within net present value models embed deep institutional discounts relative to US$5,400 to US$6,300 year-end targets. Consequently, outsized returns are concentrated in debt-free producers and permitted developers positioned in Tier-1 jurisdictions boasting near-term construction timelines.

FAQs (AI Generated)

Gold's pullback from US$5,595 to US$4,710 per ounce is driven by a cyclical headwind rather than a structural breakdown in demand. The Strait of Hormuz disruption pushed March 2026 United States Consumer Price Index inflation to 3.3% year-over-year, forcing the Federal Reserve to maintain its rate-hold position. Because gold is a non-yielding asset, elevated real yields increase the opportunity cost of holding bullion and suppress Western exchange-traded fund inflows. Central bank buying for 23 consecutive months has defended the US$4,000 to US$4,100 floor, but the most powerful re-rating catalyst remains delayed by the same inflation that sustains the geopolitical risk premium.

Two near-term catalysts are most directly relevant. A below-consensus April 30 first-quarter Gross Domestic Product reading would accelerate market pricing for second-half 2026 Federal Reserve rate cuts, reducing real yields and weakening the dollar. Separately, a credible Hormuz ceasefire that normalises oil prices would reduce headline inflation, reopening Federal Reserve easing capacity in a single macro event. Either outcome resolves the primary compression factor for gold equities without requiring a change in the structural demand picture.

The floor is demand-quantity driven rather than sentiment-based. JPMorgan Global Research's structural demand model explains approximately 70% of quarterly gold price movements through central bank and investor buying tonnage. At approximately 585 tonnes of quarterly demand modelled for 2026, the floor has a verifiable quantitative basis. The de-dollarisation thesis driving official sector accumulation is accelerating rather than moderating, reducing the probability of a sustained break below this floor.

Two compounding factors explain the valuation gap. First, execution risk premiums involving construction schedules, permitting timelines, and cost overruns are embedded in junior-to-mid-tier mining multiples independent of commodity price support. Second, most published technical figures use base-case gold price assumptions between US$2,500 and US$3,250 per ounce, meaning the equity market is discounting studies that are already structurally conservative at current spot prices.

Three criteria separate durable exploration assets from speculative positions. First, high-grade intercepts generate project-level economics at conservative price assumptions. Second, Tier-1 jurisdictions ranked in the top quartile of the Fraser Institute Annual Survey of Mining Companies offer permitting transparency and legal certainty that materially reduce execution risk. Third, explorers that can sustain systematic drill programs through the current rate-hold period without forcing equity issuance avoid the dilution that erodes per-share resource value.

Analyst's Notes

Subscribe to Our Channel

Stay Informed