Junior Uranium Miners Surge Above Broader Sector as Global Supply Deficit Reach Critical Levels

Junior uranium companies show 18% monthly gains, structural supply deficits, and strategic M&A activity amid nuclear renaissance and institutional inflows.

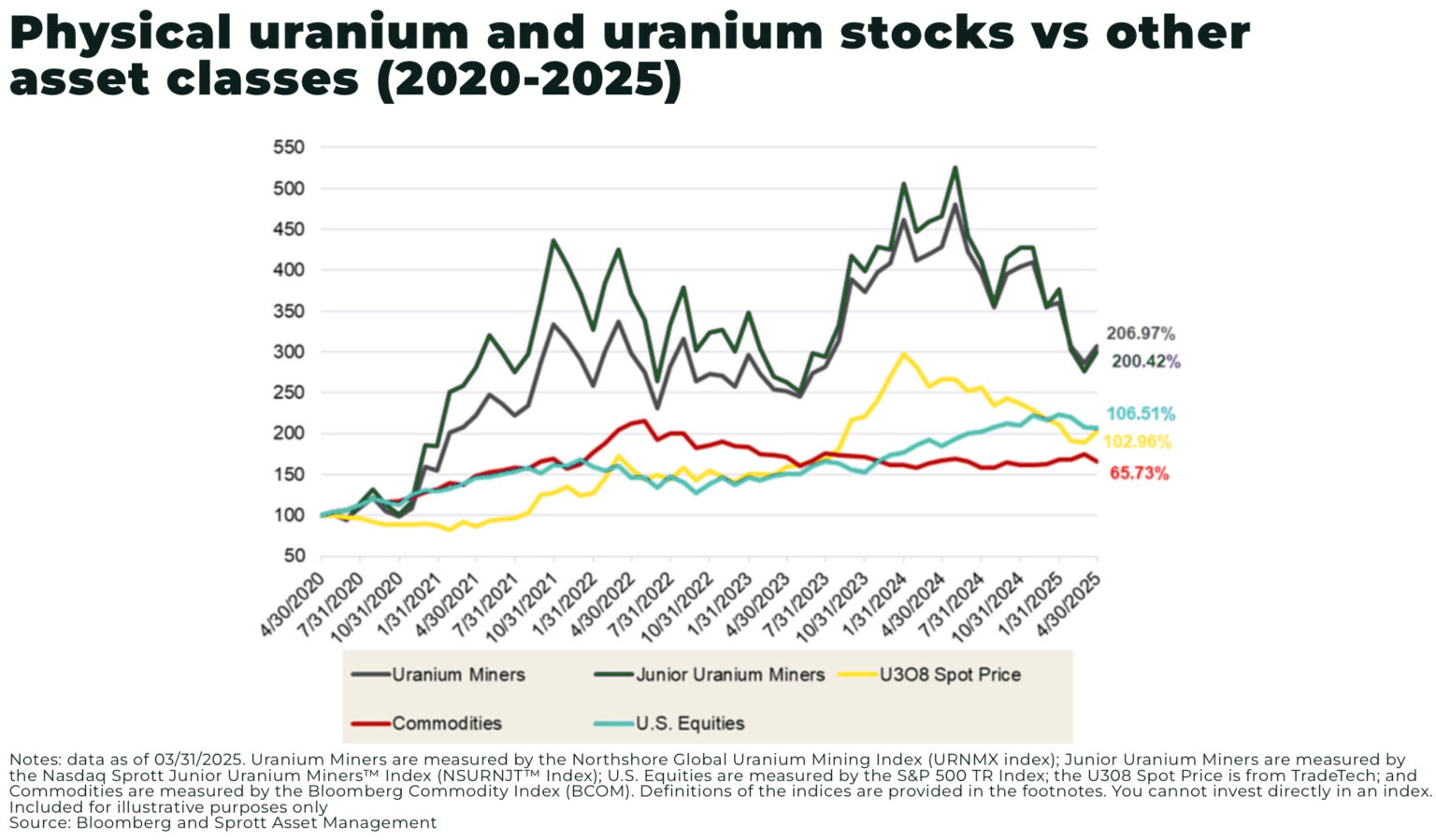

- The uranium sector experienced a dramatic V-shaped recovery in 2025, with junior mining companies demonstrating exceptional leverage to commodity price movements by delivering 17.94% gains during strong months compared to more modest returns from larger uranium producers.

- Global uranium production faces persistent structural deficits, covering only 80-90% of annual reactor demand, creating sustained supply gaps that are increasingly filled through inventory drawdowns and spot market purchases while long-term contract prices firm near $80 per pound.

- Strategic corporate consolidation is accelerating across the junior uranium space as companies optimise asset portfolios through mergers, acquisitions, and divestitures to focus on core production assets and maximise operational synergies within domestic supply chains.

- Institutional capital is flowing into uranium investments through specialised exchange-traded funds and strategic partnerships, reflecting growing recognition of the sector's fundamental dynamics and the need for diversified exposure to small and micro-cap uranium companies.

- Advanced exploration and development programs are progressing across established uranium districts, with companies leveraging technical innovations like In-Situ Recovery operations that reduce development timelines and capital requirements while maintaining environmental compliance.

The uranium sector is experiencing a fundamental transformation in 2025, driven by structural supply deficits, institutional capital inflows, and the urgent need to rebuild domestic nuclear fuel supply chains. While uranium prices have shown characteristic volatility, the underlying dynamics point to sustained opportunity, particularly within the junior mining segment where companies with market capitalisations under $100 million are demonstrating outsized leverage to commodity price movements and strategic positioning within an accelerating nuclear energy cycle.

Market Dynamics and Price Recovery

The uranium market's performance in 2025 illustrates both the sector's volatility and its underlying strength. The sector demonstrated remarkable resilience with uranium stocks recovering nearly 60% from early year depths through to June 2025 posting 11 consecutive weeks of gains.

The V-shaped recovery was accompanied by fundamental improvements in spot pricing. Uranium spot prices climbed nearly 10% in June, reaching $78.56 per pound, marking the strongest monthly performance of the year. Significantly, junior uranium miners outperformed the broader sector rising 17.94% in June, demonstrating the segment's enhanced leverage to spot price movements.

The structural backdrop supporting these price movements remains compelling. Global uranium production now covers only 80-90% of annual reactor demand, creating a persistent supply gap that is increasingly filled through inventory drawdowns and spot market purchases. Long-term contract prices have firmed near $80 per pound, though they remain below the $100+ threshold generally required to incentivise substantial new production capacity.

Financial Performance and Sector Leverage

The financial performance of junior uranium companies in 2025 demonstrates the segment's enhanced sensitivity to uranium price movements. Data from April showed junior miners rising 8.6% compared to 7.1% for uranium miners generally, driven by modest spot price gains to $67.70 per pound. This outperformance continued through subsequent months, with junior miners capturing disproportionate gains during the sector's recovery.

Several individual companies have delivered substantial returns. Private placement activities across the sector demonstrate continued access to capital markets.

Purepoint Uranium achieved a year-to-date share price gain of 109%, while simultaneously strengthening its strategic positioning through joint venture arrangements with IsoEnergy. Purepoint Uranium announced a non-brokered flow-through private placement at $6,000,000 as Chris Frostad, expressed confidence in the structural nature of the current cycle:

"We're in a structural upcycle. Things are lifting and building over time and they will continue."

Standard Uranium announced plans for a placement to raise up to C$3,500,000 to fund exploration activities. The current financing, structured as units with 24-month half-warrants, reflects current market conditions for junior exploration companies.

The company's immediate drilling campaign represents phase one of a multi-year program targeting 10,000-20,000 meters over two years, focusing on basement-hosted uranium deposits in the 250-450 meter depth range similar to the Arrow discovery.

Similarly, Urano Energy completed an upsized private placement raising C$900,000 to fund exploration as well on the company’s uranium projects in Utah and for general working capital purposes in support for domestic uranium and nuclear energy in the United States advances.

Strategic Corporate Activity and Consolidation

The junior uranium sector is experiencing significant corporate activity as companies optimize their asset portfolios and strategic positioning.

Myriad Uranium with Rush Rare Metals announced a proposed merger in August 2025, representing a strategic consolidation within the space. Under the arrangement, Myriad would acquire 100% of Rush's outstanding shares in exchange for Myriad shares, with Rush shareholders receiving one Myriad share for every two Rush shares.

Thomas Lamb, CEO of Myriad, explained the strategic rationale:

"Management of both companies strongly believe that Copper Mountain's value will be significantly higher under unified ownership. Given the vast historical spending and corresponding data, and the drilling and other work we have performed to date, we firmly believe Copper Mountain will be an important district-scale uranium source for the U.S."

Extending beyond individual mergers to broader portfolio optimization strategies, enCore Energy announced plans to divest its New Mexico uranium assets to Verdera Energy in exchange for preferred shares representing approximately 73% of Verdera, along with royalty interests and cash consideration of $350,000.

William M. Sheriff, Executive Chairman of enCore, articulated the strategic focus driving such decisions:

"As enCore pushes forward on its aggressive uranium extraction plans in South Texas, we continue to execute on our stated non-core asset disposition strategy to create additional value for shareholders. We believe that our New Mexico projects deserve a dedicated focus, which they do not currently receive inside enCore's broader portfolio of producing and near-term producing assets."

In addition, Verdera Energy joins the Clean Energy Association of New Mexico (CLEAN) to collaborate closely with local communities and maximize environmentally sound ISR uranium extraction technology to advance projects. Janet Sheriff, President and Director of CLEAN, stated:

“We are honored to announce Verdera Energy Corp. as a new member of CLEAN. Verdera is focused on advanced uranium projects that are amenable to In-Situ Recovery (“ISR”) in the state of New Mexico. ISR is known for its minimal surface disturbance and environmentally responsible approach to uranium extraction that eliminates the need for conventional mining practices.

"As the U.S. works to secure a domestic uranium supply, companies like Verdera become important in beginning a new environmentally sound chapter in New Mexico’s historic uranium landscape for clean, reliable, and affordable nuclear energy.”

The uranium sector is witnessing increased institutional participation, particularly through strategic partnerships that provide both capital and operational synergies. Snow Lake Energy completed due diligence and confirmed participation in GTI Energy's placement, representing a $1.5 million investment for a 9.9% stake in the company.

Bruce Lane, Executive Director of GTI Energy, emphasized the strategic significance of such partnerships:

"We are delighted that Snow Lake have confirmed their intention to proceed with the Placement and look forward to them joining the register after this week's shareholder meeting. Snow Lake's investment is strategically significant due to the proximity of their 50/50 JV Pine Ridge project, which adjoins Lo Herma along trend."

These strategic investments reflect a broader trend of institutional capital seeking exposure to uranium through diversified vehicles. The growth of specialized uranium ETFs, including the Sprott Junior Uranium Miners ETF (URNJ), provides institutional investors with diversified exposure to small- and micro-cap uranium companies while reducing individual company risk.

Exploration and Development Pipeline

The junior uranium sector is advancing multiple high-potential exploration programs across established uranium districts. Baselode Energy and Forum Energy Metals announced the commencement of drilling at their Aberdeen Project in Canada's Thelon Basin, targeting up to 7,000 meters across 18-25 drill holes.

In a news release, Baselode Energy highlighted the exploration potential:

"We're very excited that drilling has begun at Aberdeen. The Loki target area has all of the characteristics we'd expect to find near a high-grade uranium deposit in the Athabasca Basin; elevated uranium in the sandstone and within 10 m of the basement unconformity, clay alteration, bleaching, desilicification and highly anomalous pathfinder elements in the sandstone."

Similarly, Standard Uranium announced plans for a diamond drill program at its Davidson River project in Saskatchewan's Athabasca Basin, following completion of the first Exosphere Multiphysics survey in the region. CEO Jon Bey expressed confidence in the program:

"Standard Uranium has been working towards this drill program for over three years, and we couldn't be more excited to see the drills turning once again... It is now time to make a discovery and add significant value for our shareholders."

GTI Energy's Lo Herma Project exemplifies this positioning as one of the few near-term, low-cost In-Situ Recovery uranium projects in the United States. The company's strategic positioning reflects broader policy support for domestic uranium production capabilities. As geopolitical tensions highlight supply chain vulnerabilities, U.S. uranium projects with established permitting pathways and technical feasibility studies are attracting increased attention from both private investors and policy makers.

Junior uranium companies are strategically positioning themselves to benefit from the rebuild of America's domestic uranium supply chain. The technical advantages of In-Situ Recovery operations, which eliminate the need for traditional mining infrastructure while maintaining environmental compliance, position these projects favorably within regulatory frameworks increasingly focused on sustainable resource development.

The Investment Thesis for Uranium

- Leverage Structural Supply Deficits: Global uranium production consistently falls short of reactor demand by 10-20%, creating a structural deficit that junior exploration companies are positioned to address through new discoveries and development projects.

- Capitalize on Enhanced Price Sensitivity: Junior uranium companies demonstrate superior leverage to uranium price movements, with the segment showing 17.94% gains in strong months compared to more modest returns from larger producers.

- Target Advanced Development Projects: Focus investment on companies with near-term production potential, established permits, and proven technical feasibility, such as those with In-Situ Recovery capabilities that reduce development timelines and capital requirements.

- Monitor Institutional Capital Flows: Track institutional investment through specialized ETFs like URNJ and strategic partnerships that provide both capital and operational synergies, as these flows often precede broader market recognition.

- Prioritize Strategic Asset Consolidation: Seek companies positioned for acquisition by larger producers, as the high barriers to entry and technical complexity of uranium development favor strategic consolidation over organic growth.

- Evaluate Geopolitical Positioning: Consider domestic uranium projects within allied jurisdictions, particularly those supporting supply chain security objectives and benefiting from policy support for domestic production capabilities.

- Diversify Through Specialized Vehicles: Utilize uranium-focused ETFs to gain diversified exposure across the junior mining space while reducing individual company execution risks inherent in exploration-stage investments.

- Assess Management Track Records: Prioritize companies with management teams demonstrating previous success in uranium discovery, development, or production, as technical expertise significantly influences project success rates.

The uranium investment opportunity in 2025 reflects a convergence of structural supply constraints, institutional capital flows, and strategic positioning within a rebuilding nuclear supply chain. Junior uranium companies, while inherently volatile and subject to execution risks, offer leveraged exposure to these fundamental dynamics through their outsized sensitivity to uranium price movements and strategic value to larger producers seeking growth through acquisition. The sector's recent performance, combined with strengthening institutional participation and strategic corporate activity, suggests sustained opportunity for disciplined investors capable of managing the inherent volatility of exploration-stage resource investments.

The combination of structural supply deficits, policy support for domestic production, and technical advances in extraction methods creates a favorable backdrop for junior uranium investments, provided investors maintain appropriate diversification and recognize the extended development timelines characteristic of uranium projects.

Analyst's Notes

Subscribe to Our Channel

Stay Informed