Kazakhstan's 10% Production Cut & Higher Incentive Prices Improve Western Project Economics

Kazakhstan's 10% uranium production cut is lifting incentive prices, improving Western project economics, and reinforcing long-term supply constraints.

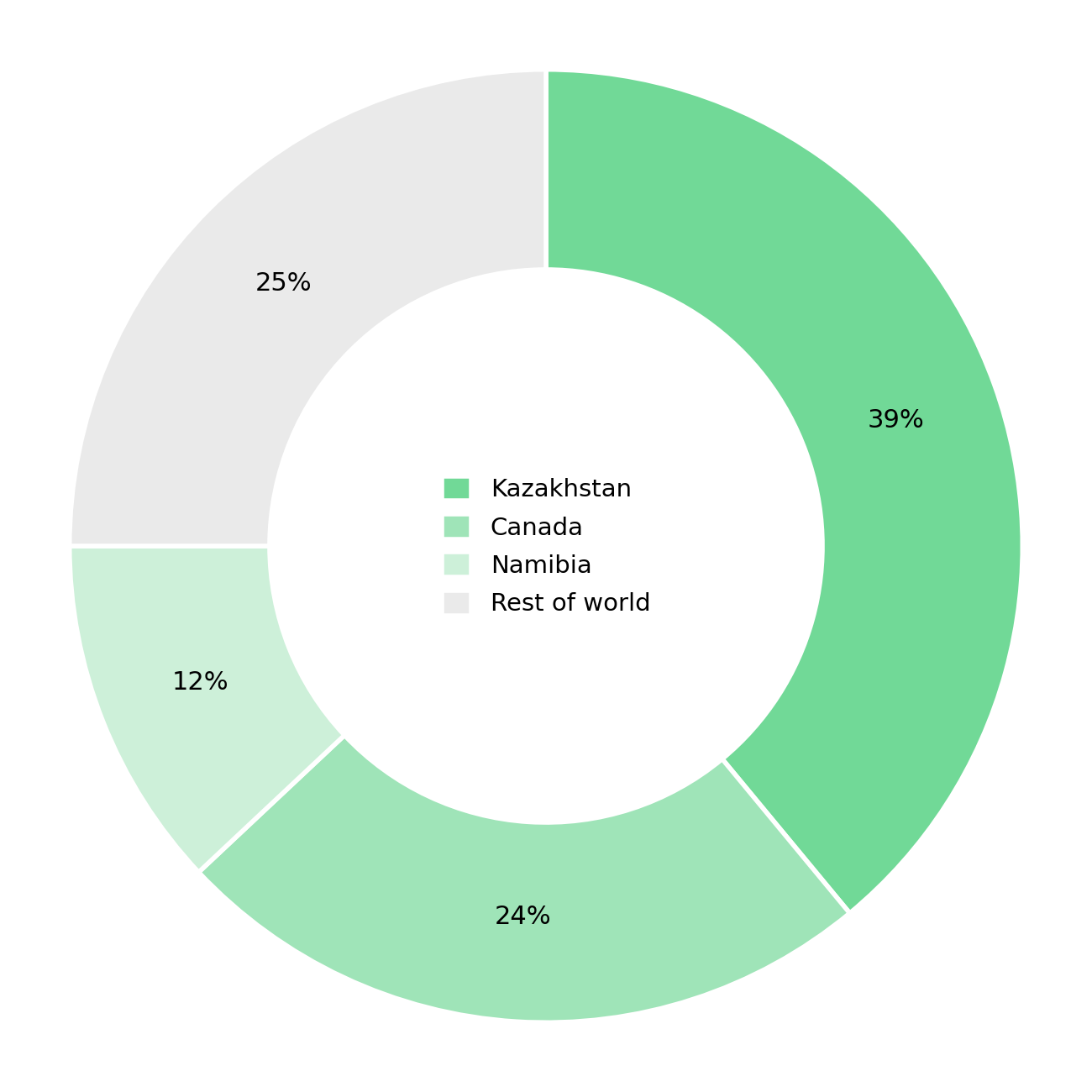

- Kazakhstan, which accounts for roughly 40% of global mined uranium, has confirmed a 10% production cut for 2026, reducing guidance from 32,777 tonnes to 29,697 tonnes.

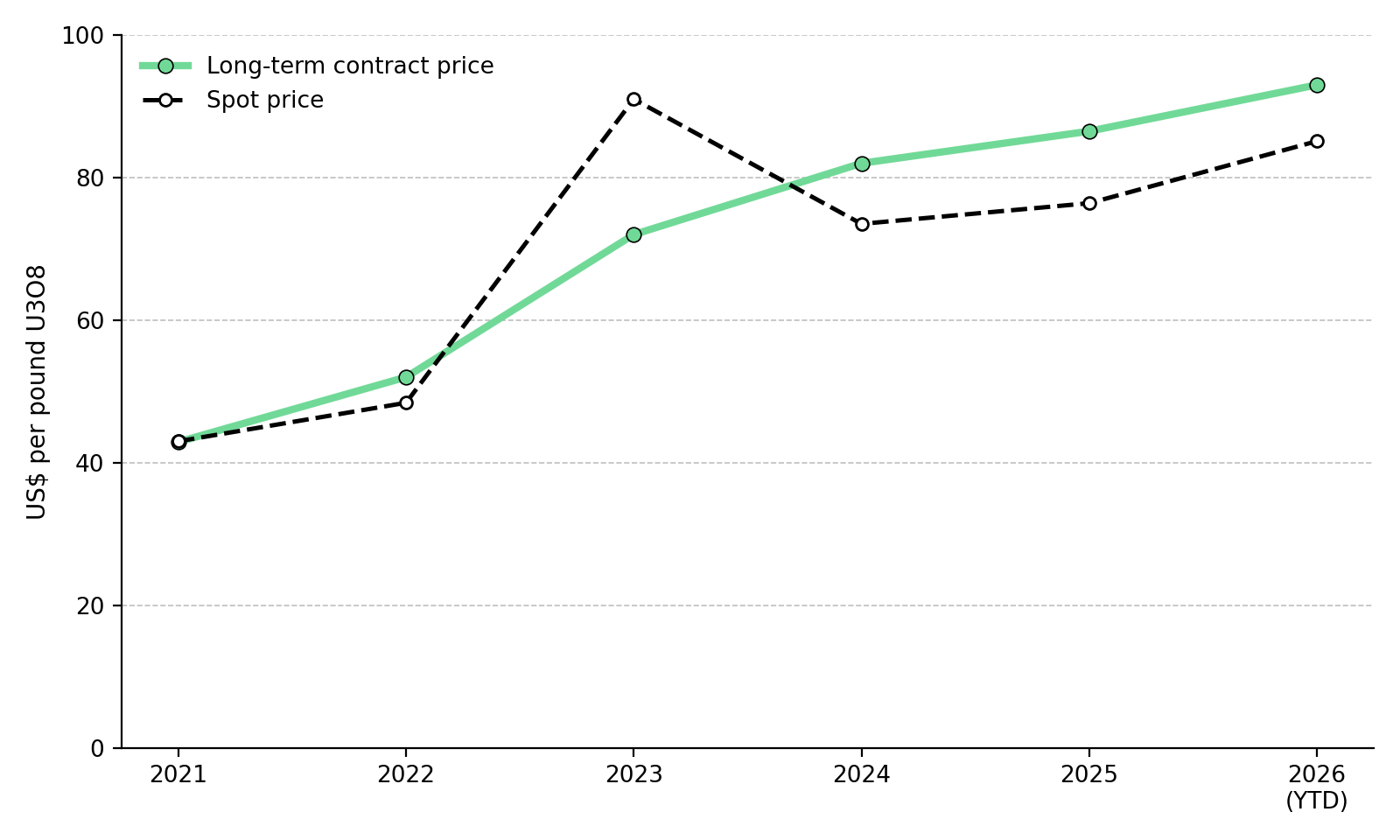

- The production cut is widening the gap between uranium's long-term contract price, which is near an eighteen-year high of approximately $93 per pound, and the spot price, which has remained near $85 per pound, signaling that utilities are pricing in tighter future supply.

- US uranium mine production more than doubled in 2025, according to the Energy Information Administration, but output remains well below the level needed to meaningfully reduce reliance on overseas uranium supply.

- Western uranium producers, developers, and explorers each benefit differently from tighter uranium supply, with producers generating cash flow today, developers advancing toward production, and explorers offering longer-term discovery potential.

- Term uranium prices provide a better measure of future supply expectations than spot prices because most utility purchasing occurs through long-term contracts rather than the spot market.

Supply Concentration & Higher Uranium Incentive Prices

Few commodities are as geographically concentrated as uranium, allowing a single sovereign producer's guidance revision to influence the global market. Kazakhstan accounts for roughly 40% of global uranium output, far exceeding the concentration seen in gold or copper, where the largest producing country typically supplies only a low double-digit share of global output. When Kazakhstan's state uranium company reduces planned production, utilities and producers must reassess future supply availability across the global uranium market. Lower output from the industry's lowest-cost producer increases the uranium price needed to justify new production from higher-cost projects elsewhere.

Kazakhstan has confirmed that 2026 production will fall from 32,777 tonnes to 29,697 tonnes, a reduction of 3,080 tonnes, or 10%. Most of the reduction comes from the Budenovskoye joint venture, while final production guidance remains dependent on sulfuric acid availability, the leaching reagent used in Kazakhstan's in-situ recovery operations. The reduction reflects an operational decision rather than depleted resources or weaker uranium demand. Because much of Kazakhstan's production is already committed under long-term contracts, the company has little incentive to maximize output at current prices, leaving higher-cost producers to supply future demand.

Rising Input Costs & Slower Production Growth

Kazakhstan's production cut is difficult to reverse because its in-situ recovery operations depend on adequate sulfuric acid supply. When sulfuric acid becomes scarce because of competing demand from fertilizer and battery metals producers or logistics disruptions, uranium production cannot increase regardless of the size of the resource base. Conventional and heap leach operations are less dependent on a single processing input, making their production costs less sensitive to sulfuric acid shortages.

Energy Fuels operates the only fully licensed conventional uranium mill in the US at White Mesa, Utah, and reports processing costs of $9 to $12 per pound of uranium oxide and mining, processing, and transport costs of $23 to $30 per pound at its Pinyon Plain operation. These costs remain well below current realized uranium prices, while conventional mining is less exposed to sulfuric acid supply constraints than Kazakhstan's in-situ recovery operations. Mark Chalmers, Chief Executive Officer of Energy Fuels, discusses why new uranium supply remains difficult:

"You see it around the world, the challenges people have been having are restarting and getting projects going. Prices still aren't where they really need to be long term. The uranium business looks fantastic going forward."

US Uranium Reshoring & Remaining Capacity Gap

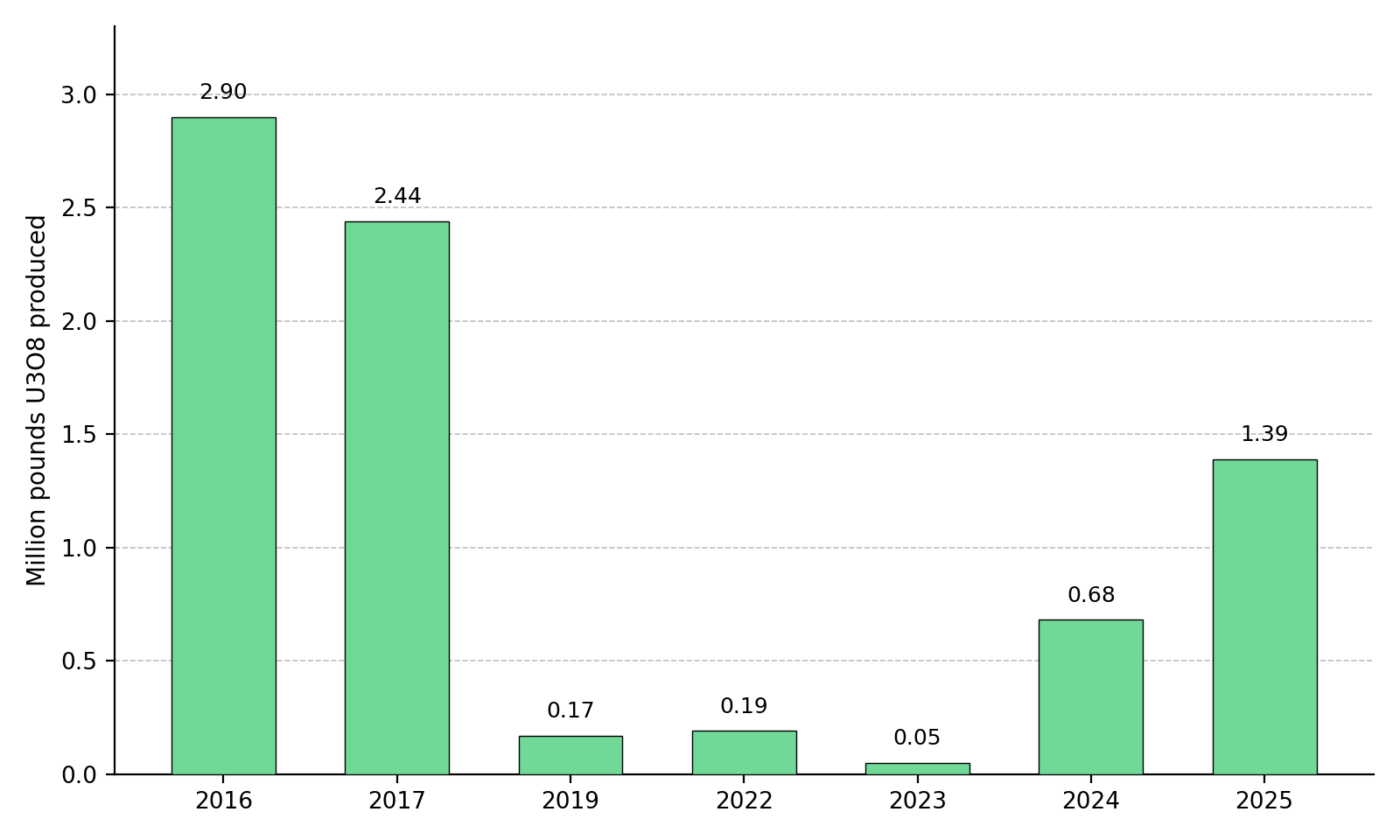

The US Energy Information Administration's June Domestic Uranium Production Report confirmed that mine production more than doubled to 1.388 million pounds of uranium oxide in 2025, up from 677,000 pounds in 2024 and the highest annual output since 2016. Exploration and development drilling activity also reached its highest level since 2013, signaling continued investment in expanding domestic uranium supply. The increase marks measurable progress in rebuilding US uranium production capacity.

enCore Energy operates in-situ recovery uranium assets in South Texas and is expanding production from its existing operations. Q1 2026 uranium extraction increased 22% year over year to 90,000 pounds from 73,711 pounds, while the company realized an average sales price of $67.78 per pound. US uranium production of 1.388 million pounds in 2025 remains well below the 13.3 million pounds of licensed annual capacity across operating in-situ recovery facilities, indicating that much of the existing infrastructure remains underutilized.

Development Milestones & Future Uranium Supply

Development-stage uranium companies have defined resources but are not yet producing, with permitting, engineering, and feasibility work advancing projects toward construction while reducing development risk. Success at this stage depends less on resource discovery than on advancing permitting, engineering, and project execution.

Atomic Eagle is advancing the Muntanga uranium project in Zambia, which hosts a combined measured, indicated, and inferred resource of 58.8 million pounds of uranium oxide at an average grade of 309 parts per million. In June, the company secured environmental approval from the Zambia Environmental Management Agency and approval of its Resettlement Action Plan from the Office of the Vice President, completing two key social and environmental permitting milestones ahead of any construction decision. The company continues to prioritize expanding the resource base before making a construction decision. Phil Hoskins, Chief Executive Officer of Atomic Eagle, describes the growing gap in uranium supply:

"For the first time since the 1960s, towards the end of this decade, reactors are going to be dependent on new supply coming out of the ground. Since Fukushima, the market has been working through significant secondary supplies. That deficit, around 30 million pounds, is going to need to be rectified from uranium coming out of the ground."

IsoEnergy holds the Hurricane deposit in Saskatchewan's Athabasca Basin, which the company describes as the world's highest-grade indicated uranium resource. The company also completed the acquisition of Toro Energy, adding the Wiluna project in Western Australia to its portfolio. The combined portfolio spans Canada, Australia, and the US, with the company's Utah assets offering the nearest potential source of production while larger development projects continue to advance. Phil Williams, Chief Executive Officer of IsoEnergy, explains why higher uranium prices must persist:

"When you look at demand doubling or more by 2040, and no real understanding of where the supply is coming from, prices do have to stay higher for longer in order to incentivize that."

Exploration Success & Resource Growth

ATHA Energy controls the entire Angikuni Basin surrounding its Angilak project in Nunavut, a land package the company describes as Canada's largest prospective uranium exploration package. The 2025 drilling program intersected uranium mineralization in every hole drilled across roughly 14 kilometers of the Rib Corridor. The company has also fully funded its largest exploration program to date, approximately 20,000 meters across three drill rigs, through a C$63 million financing completed in February. Angilak does not yet have a defined mineral resource. The project's value will depend on future exploration results rather than existing mineral resources or near-term production. Troy Boisjoli, Chief Executive Officer of ATHA Energy, discusses why exploration matters during supply uncertainty:

"We have the opportunity and the ability to be executing on a project that has tremendous scale potential at a time in the uranium sector when the vast majority of the risk is on the supply side, and there's supply side uncertainty here."

A production cut by the dominant supplier does not reduce the geological or execution risks associated with uranium exploration. New uranium discoveries become more valuable because they provide the only long-term source of replacement supply once existing producers and developers have fully expanded their current resource bases, a process that can take a decade or more.

Long-Term Contract Pricing & Uranium Market Signals

Uranium pricing differs from that of most commodity markets because most uranium is not bought and sold on the spot market. Instead, utilities and producers negotiate long-term contracts that typically span several years and include either base-escalated or market-related pricing terms. As a result, the spot price reflects only a small share of total uranium transactions and may not fully capture underlying utility demand.

Comparing spot and long-term uranium prices provides a clearer picture of current supply expectations. Spot uranium has traded near $85 per pound since early April, reflecting limited utility activity in the spot market rather than weaker uranium demand. Long-term uranium contract prices reached approximately $93 per pound in the first quarter of 2026, their highest level in more than eighteen years. Higher long-term contract prices indicate that utilities are pricing in Kazakhstan's production cut and the associated risk of a concentrated uranium supply. Utilities negotiating multi-year contracts are assuming tighter future uranium supply even while activity in the spot market remains limited.

The distinction between spot and long-term contract pricing has direct implications for valuing uranium producers and developers. Long-term contract prices, rather than spot prices, underpin the realized-price assumptions used in company net present value and internal rate of return models. They also form the basis for the price assumptions that reserve-based lenders and project financiers use when assessing project bankability. A sustained increase in long-term contract prices provides a stronger basis for financing and project development decisions than short-term movements in the spot market. Long-term contract prices therefore, provide the clearest pricing signal for evaluating producers, developers, and explorers throughout the uranium supply chain.

The Investment Thesis for Uranium

- Kazakhstan's 10% production cut shifts the economics of the uranium market by increasing the incentive price needed to bring higher-cost Western production into operation.

- US uranium production more than doubled in 2025, but current output remains well below installed licensed capacity, highlighting that reshoring has begun but has not yet restored sufficient domestic supply to offset tighter global markets.

- Development-stage projects are advancing through permitting and engineering, reducing development risk without generating cash flow. Future value will depend on feasibility studies, financing, and construction decisions that move projects toward production.

- Exploration companies provide exposure to future uranium discoveries, but their value depends on defining mineral resources through continued drilling rather than generating near-term production or cash flow.

- Long-term uranium contract prices provide a clearer indication of market conditions than spot prices because utilities negotiate most uranium purchases through multi-year contracts that reflect future supply expectations.

- Jurisdictional diversification across Canada, the US, Zambia, and Australia spreads permitting, cost, and political risks across multiple uranium-producing regions rather than relying on a single jurisdiction.

Kazakhstan's production cut is more than a short-term event; it highlights how heavily the global uranium supply depends on a single producer. The production cut underscores how concentrated global uranium supply remains, making supply concentration a more important driver of long-term uranium prices than any single company's quarterly results. Higher long-term contract prices relative to spot prices reflect utility expectations that future uranium supply will remain tight, even while spot market activity remains limited. This pricing dynamic affects producers, developers, and explorers differently because each responds to higher long-term uranium prices at a different stage of the project lifecycle. Further production guidance from Kazakhstan, sulfuric acid supply conditions, and permitting progress for Western uranium projects will help determine whether long-term uranium supply remains constrained.

TL;DR

Kazakhstan's 10% uranium production cut reinforces how dependent the global market remains on a single low-cost supplier. With long-term uranium contract prices near an eighteen-year high and well above spot prices, utilities are signaling expectations of tighter future supply. US uranium production is recovering but remains far below licensed capacity, while producers, developers, and explorers each stand to benefit differently from stronger long-term pricing. Permitting progress, exploration success, and jurisdictional diversification are becoming increasingly important as the industry works to bring new uranium supply online.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed