Mine Supply Grows Only 1% as Central Banks Absorb 25% of Output, Favoring Buildable Gold Developers

Gold's supply outlook remains tight as mine output grows only about 1% and central banks absorb a quarter of supply, favoring buildable gold developers.

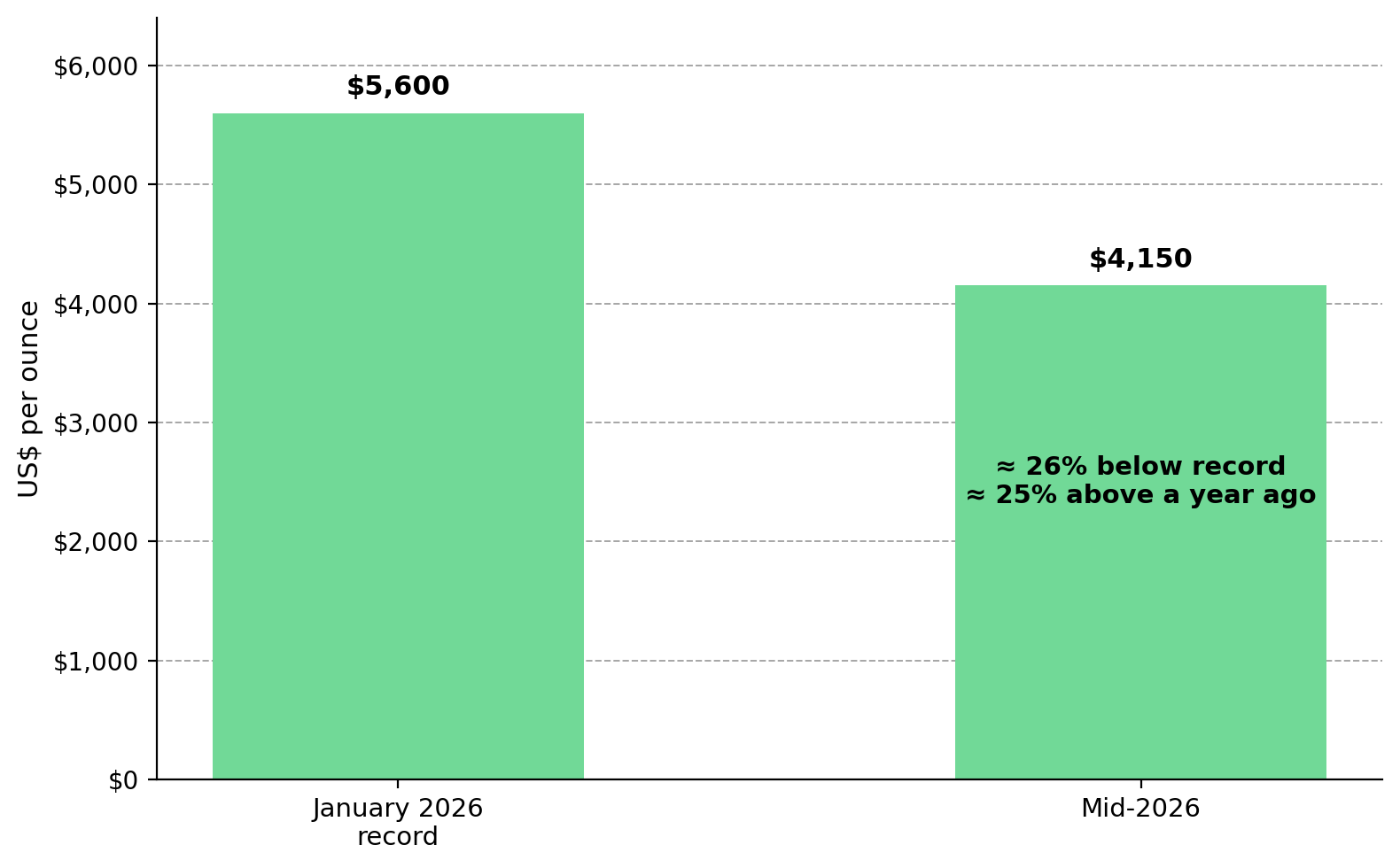

- Gold trades about 25 percent below its January 2026 record near $5,600 an ounce but remains roughly 25 percent higher than a year ago. The pullback reflects higher real-rate expectations and lower geopolitical risk premiums rather than any improvement in mine supply or official-sector demand.

- The longer-term driver is constrained mine supply. Mine output reached a record in 2025 but grew only about 1%, while Newmont, Barrick, and Agnico Eagle guided to lower 2026 production as reserves declined.

- Central banks now absorb roughly a quarter of annual mine supply, reducing the metal available to private buyers regardless of price.

- The market now rewards buildability over resource size. Projects with strong economics, permits, and financing command higher valuations than large resources without a clear path to production.

- The developers and explorers featured here show how the market rewards buildability over resource size. All are pre-cash-flow or ramping to production, and development-stage equities carry a high risk of capital loss.

Cyclical Gold Weakness & the Enduring Supply Constraint

Gold entered the second half of 2026 near $4,100 to $4,200 an ounce, about 25% below its January record near $5,600 but still roughly 25% higher than a year earlier. The pullback reflects higher US interest-rate expectations and a lower Middle East risk premium as Brent crude fell toward $72 a barrel. Short-term price moves often reflect macro data and market positioning rather than changes in the physical gold market.

For long-term capital, the key question is whether gold supply can keep pace with demand. The Fed, the US dollar, and geopolitical risk drive short-term price moves, while mine supply and official-sector demand determine the longer-term trend. The constraint is no longer finding gold but bringing new supply into production at an economic return. As a result, developer valuations depend less on resource size and more on a project's ability to reach production.

Stalled Mine Growth & Sustained Central-Bank Buying Tighten Gold Supply

Two forces are tightening the gold market: constrained mine supply and sustained official-sector demand. Mine supply has become increasingly unresponsive to higher prices. At the same time, central banks continue buying regardless of price, removing metal from the tradable market. Together they keep the physical market tight despite short-term price weakness.

Mine Supply Grows Slowly as Reserves Decline

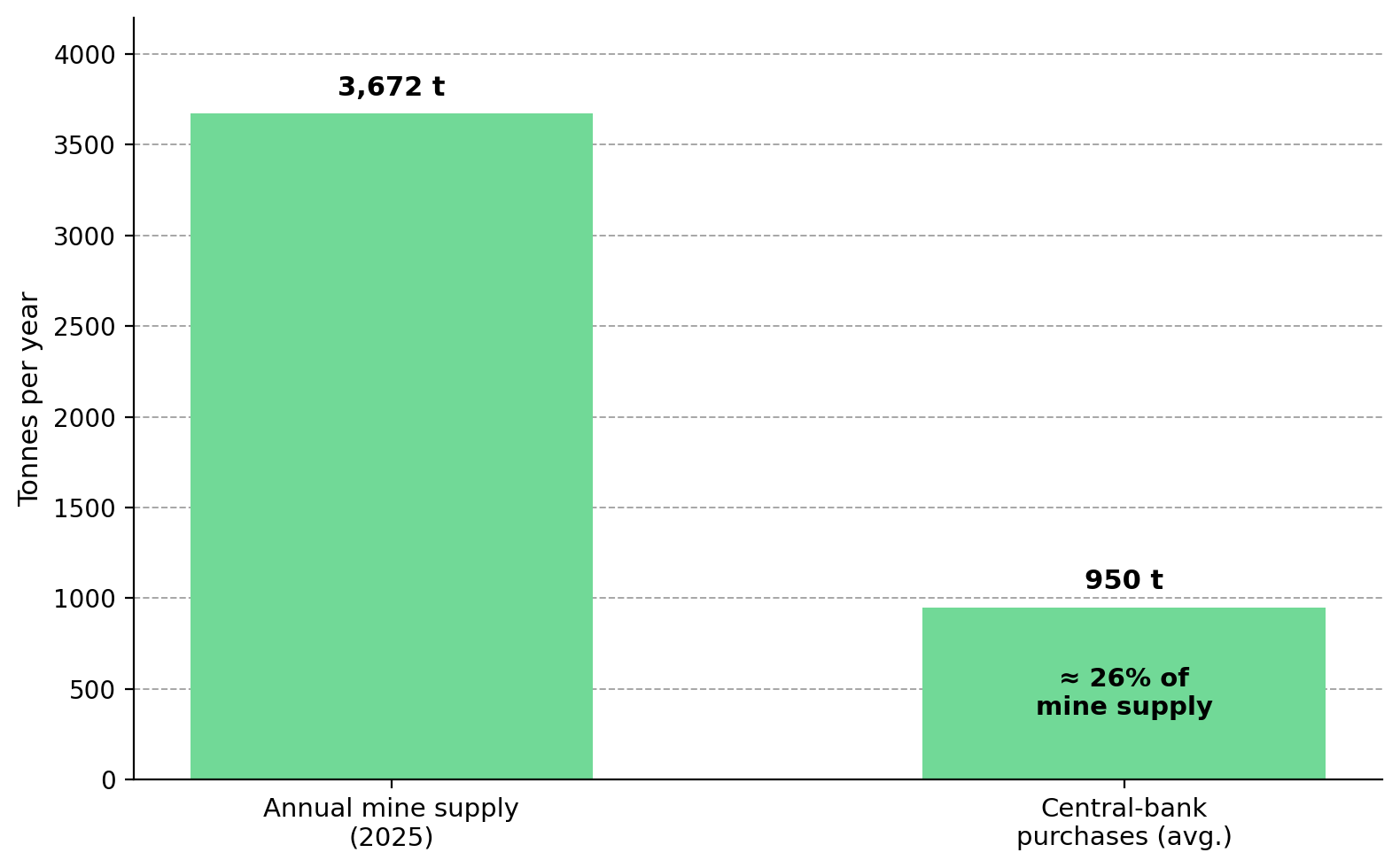

According to the World Gold Council, mine production reached a record 3,672 tonnes in 2025 but grew only about 1% from the prior year, extending a 15-year pattern of minimal supply growth. Higher prices do not quickly increase supply because discoveries are becoming rarer, permitting takes longer, and new mines often require more than a decade to reach production. Only reserves, not total resources, support current mine production, and every ounce mined reduces that inventory until it is replaced.

Freeport-McMoRan's Grasberg mine in Indonesia, operating under force majeure, is expected to produce about 35% less gold than its original 2026 target of roughly 1.6 million ounces, with full recovery not expected until 2027. Newmont, Barrick, and Agnico Eagle also reported lower gold production in 2025 and guidance to further declines in 2026 as reserves mature.

Official-Sector Buying Absorbs a Quarter of Mine Supply

The second driver is sustained central-bank buying. Goldman Sachs Research estimates official-sector purchases have averaged 900 to 1,000 tonnes a year, or roughly a quarter of annual mine production, since the 2022 freezing of Russian reserves accelerated central-bank reserve diversification. Gold bought by central banks is typically held in reserves, reducing the metal available to private buyers.

This figure is best interpreted as a multi-year average rather than a quarterly run rate. The World Gold Council reported gross official buying of about 244 tonnes in the first quarter of 2026, while J.P. Morgan estimated net reported purchases at just 16 tonnes after Turkiye sold 60 tonnes in March, noting that a meaningful share of central-bank activity remains unreported. Quarterly data can fluctuate, but sustained central-bank buying remains a key assumption behind major banks' above-spot gold price targets.

Gold Developer Valuations Shift From Resource Size to Buildability

Scarce gold supply has shifted equity valuations toward buildable projects. Resource size alone no longer commands a premium. Large inferred resources carry limited value until economic studies, permitting, and financing establish a credible path to production.

This is why enterprise value per ounce varies widely across otherwise similar deposits. The market discounts low-confidence resources and mineralization that has not yet demonstrated economic viability. Buildability, not resource size, now drives valuations.

Project Economics Now Drive Valuations More Than Resource Size

Tudor Gold holds one of Canada's largest undeveloped gold resources at its Treaty Creek project in British Columbia, including 24.9 million ounces of indicated gold within a large gold-copper-silver porphyry system. The next valuation catalyst is the preliminary economic assessment, which will determine whether those ounces can generate attractive project economics.

The same valuation approach also applies to earlier-stage explorers. P2 Gold's Gabbs gold-copper project in Nevada is valued less on resource size than on the economics its studies can demonstrate. Its October 2025 preliminary economic assessment reported an after-tax net present value of about $943 million and an internal rate of return of roughly 34%, with management indicating both metrics improve at current spot prices.

Permitting, Cost Position & Cash Flow Drive Developer Valuations

Once buildability drives valuations, project de-risking becomes the key differentiator. The three most important factors are permitting, a low all-in sustaining cost (AISC), and visible near-term cash flow. A feasibility study converts resources into reserves and provides the technical basis for project financing.

Fully Permitted Projects Command Higher Valuations

Longer permitting timelines have increased the value of fully permitted projects. U.S. Gold Corp's fully permitted CK Gold project in Wyoming carries an after-tax net present value of about $630 million and an internal rate of return near 30% using a conservative $3,250 gold price, with copper contributing roughly 30% of project economics. Its market capitalization of about $260 million remains well below the project's after-tax net present value, although construction financing has not yet been secured.

Luke Norman, Executive Chairman of U.S. Gold Corp, explains why a Wyoming state permit with a closed objection window can reduce permitting risk compared with projects on US federal land or in jurisdictions where permits remain open to legal challenge:

"We're the first fully permitted hard rock mining opportunity in almost 100 years in Wyoming. If you're in Canada or on federal ground, anyone could come in and challenge your permit to mine midstream. You could be halfway through a build and someone could challenge it."

Cost Position Determines Which Projects Remain Economic

In a gold price drawdown, cost position determines which projects remain economic. New Found Gold is advancing the Hammerdown mine toward commercial production while developing the larger Queensway project, whose preliminary economic assessment outlines AISC of about $1,090 to $1,300 per ounce on fully funded initial capital of C$155 million. Its acquisition of a permitted mill reduces development risk by providing existing processing infrastructure that many explorers must build from scratch.

Near-Term Cash Flow Reduces Financing Risk

Near-term cash flow is the strongest form of de-risking because it reduces reliance on equity financing and volatile capital markets. Cabral Gold is about 70% through constructing a low-capital heap-leach operation at its Cuiú Cuiú project in Brazil, targeting first gold in the fourth quarter of 2026 at a life-of-mine grade of about 0.7 grams per tonne and AISC of roughly $1,200 per ounce. The near-surface oxide ore supports lower-cost heap leaching, while deeper sulfide ore would require a conventional mill.

Alan Carter, President and Chief Executive Officer of Cabral Gold, explains how early cash flow can fund district-scale exploration while reducing reliance on equity financing:

"These four to six gold deposits that we know about now within this district, and we've got 50 targets that need to be tested, are going to require time and money, and we think the best way to fund that massive effort is not to keep diluting the capital structure. We need to be self-funding, so that's why we're putting this initial phase one operation into production."

Stable Jurisdictions & Existing Infrastructure Strengthen Developer Valuations

The same geopolitical fragmentation driving central-bank reserve diversification also increases resource-nationalism risk, where royalty increases, license reviews, and retroactive taxation can reduce project returns. Stable jurisdictions and existing infrastructure therefore command higher valuations because they reduce permitting and execution risk.

Brownfield Infrastructure Reduces Development Risk

A past-producing site with existing power, roads, and processing infrastructure is cheaper and faster to advance than a greenfield discovery. Hycroft Mining holds one of the world's largest precious-metals deposits in Nevada, with about 16.5 million ounces of gold and nearly 600 million ounces of silver. The company is debt-free, holds roughly $200 million in cash, and has a largely institutional shareholder base. Its scale and Nevada location support long-term value, although a full-scale development would require multi-billion-dollar capital spending and favorable metal prices.

Diane Garrett, President and Chief Executive Officer of Hycroft Mining, explains why existing infrastructure in a stable mining jurisdiction can lower capital requirements and development risk:

"Most other developers are greenfield developers. They've got a resource, but sometimes that's about it. The infrastructure we have on site today would cost over a billion dollars to build, and we're in Nevada, USA, the premier mining jurisdiction."

Critical Minerals Follow the Same Supply & Valuation Drivers

The same supply constraints apply beyond gold. Limited supply growth and a premium for low-capital projects in stable, permit-friendly jurisdictions apply across strategic metals. Cobra Resources demonstrates how the same valuation framework extends to critical minerals. Its South Australian projects target heavy rare earths and copper using low-capital in-situ recovery instead of conventional mining. Although the commodity differs, the same valuation drivers apply: constrained supply, lower capital intensity, and a credible path to production.

Developer Case Studies Reinforce the Gold Macro Thesis

These projects reflect the same gold-market thesis. Mine supply is growing by only about 1% a year while reserves continue to decline, as central banks absorb roughly a quarter of annual mine output. Those supply-demand dynamics are largely independent of the next inflation print or Fed decision and remain a key assumption behind major banks' above-spot gold price targets.

The correction has not changed the supply outlook, but it has changed what the market rewards. Capital now rewards projects that convert resources into permitted, financed, low-cost production and discounts those that cannot. That is why permitting, cost position, and near-term cash flow now explain more of the variation in developer valuations than headline resource size. Cyclical risks remain. A credible de-escalation in geopolitical tensions or a more hawkish Fed could pressure gold prices and developer valuations, but neither would increase mine supply or replenish reserves.

The Investment Thesis for Gold

- Gold's long-term outlook rests on mine supply growing only about 1% a year while reserves decline and replacement projects remain scarce.

- Official-sector demand equal to roughly a quarter of annual mine supply reduces the metal available to private buyers and remains a key assumption behind major banks' above-spot gold price targets.

- The market now rewards developers that have demonstrated project economics, permitting progress, and financing over those with large inferred resources alone.

- Fully permitted projects in stable jurisdictions command higher valuations because permitting risk has largely been removed before construction begins.

- Low all-in sustaining costs (AISC) protect margins during gold price declines and allow developers to continue funding growth.

- Near-term, low-capital cash flow reduces shareholder dilution and dependence on volatile capital markets, making it one of the strongest project de-risking factors.

- The same supply constraints and preference for buildable projects also apply across adjacent critical minerals, extending this valuation framework beyond gold.

The key constraint in gold is no longer finding deposits but bringing new supply into production. With mine supply growing only about 1% a year and central banks absorbing roughly a quarter of new output, the strongest developer valuations belong to projects that can reach permitted, financed, low-cost production. The companies discussed that progression, from large resources awaiting economic studies to projects approaching first production. The key distinction is buildability over resource size, while recognizing that development-stage companies carry a high risk of capital loss and remain exposed to gold price volatility.

TL;DR

Gold's recent pullback reflects short-term macro factors rather than an improvement in supply. Mine production is growing by only about 1% annually while reserves continue to decline, and central banks absorb roughly one-quarter of annual mine output, tightening the physical market. As a result, the market increasingly values developers that can demonstrate project economics, permitting progress, low operating costs, and near-term cash flow instead of simply reporting large resource estimates. The article concludes that buildability has become the primary driver of gold developer valuations, although development-stage companies remain exposed to financing, execution, and gold price risks.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed