New Found Gold: Execution Risk Replaces Geological Uncertainty as Development Advances

New Found Gold shifts from exploration to development, reducing geological risk at Queensway while execution, financing, and ramp-up become key investor risks.

- New Found Gold has transitioned from an exploration-driven story to an early-stage developer, with a US$75 million debt package and the Pine Cove Mill acquisition giving it the capital and infrastructure to target first Queensway production by the end of 2027.

- The Queensway Phase 1 preliminary economic assessment (PEA) outlines a front-loaded production profile: 100,000 ounces per year in the first two full years at above 12 grams per tonne (g/t), tapering to a four-year average of 69,000 ounces at 9.6 g/t, against an initial capital expenditure (capex) of C$155 million.

- Hammerdown is expected to generate enough cash flow to offset its own capital requirements this year, meaning the US$75 million debt package does not need to fully fund the path to Queensway production on its own.

- The 74,000-metre grade control program completed in 2025 confirmed the continuity of the high-grade core across a zone representing roughly a year of Phase 1 production, shifting the primary risk from geology to operational execution.

- Near-term milestones include the debt package closing, the environmental assessment certificate (EAC) application outcome, Hammerdown's commercial production ramp, and a Third Quarter 2026 technical report that will present Phase 1 at near-feasibility quality for the first time.

What Has Happened

New Found Gold (TSX: NFG) has moved beyond the discovery phase that built its reputation. A term sheet for a US$75 million debt financing package, expected to close mid-April 2026, combined with the November 2024 acquisition of Maritime Resources and its Pine Cove Mill, gives the company the capital and infrastructure to advance its flagship Queensway project in Newfoundland toward production.

For most of its existence, the investment case rested on high-grade intercepts along the Appleton fault zone. Today, the company operates the Hammerdown Mine, is ramping toward commercial production, and is targeting first production at Queensway toward the end of 2027. Geological uncertainty has not disappeared, but the 74,000-metre grade control program completed in 2025 confirmed the high-grade core across a zone representing roughly a year of Phase 1 production. The risk profile has shifted from whether the ore is there to whether the company can mine and process it on schedule and on budget.

A Mandate Change That Defined the Current Trajectory

When Keith Boyle took the Chief Executive Officer role in January 2025, the mandate was clear: get to cash flow.

"We've got this great asset called Queensway, and we've got to take advantage of the high-grade gold that sits right at the surface for us to get to cash flow and stop the ‘raise money, drill, raise money, drill’."

The acquisition of Maritime Resources in mid-November 2024 was the first concrete step under that strategy, bringing Pine Cove Mill and the Nugget Pond Gold Circuit, a 700-tonne-per-day processing facility, under New Found Gold's control.

The strategic logic was straightforward. Rather than constructing a standalone processing plant, the company secured Pine Cove Mill, approximately 95 kilometres from Hammerdown, enabling revenue generation from Hammerdown ore during the Queensway development period and reducing net capital requirements ahead of first Queensway production.

Queensway Phase 1: What the PEA Outlined

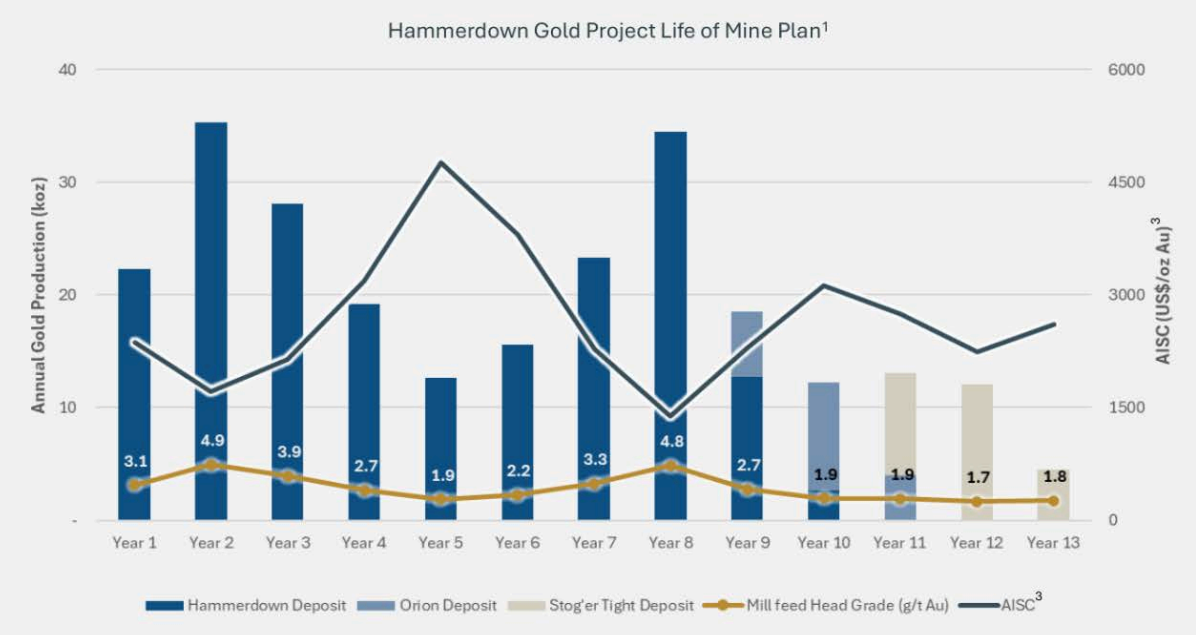

The preliminary economic assessment (PEA) released in 2025 outlined a phased development approach targeting a mining rate of 700 tonnes per day, focused on the high-grade core of the Queensway deposit. Over the first four years, the plan averages 9.6 grams per tonne (g/t) and approximately 69,000 ounces per year, but the grade profile is front-loaded: the first two full years are expected to run above 12 g/t, delivering a targeted 100,000 ounces per year in the first two full years, before grades taper below 9 g/t, at a Phase 1 average all-in sustaining cost (AISC) of US$1,282 per ounce over the full four years.

Initial capital expenditure (capex) for Phase 1 was set at C$155 million in the PEA and may come in slightly higher following two structural changes: relocating the gold circuit from Nugget Pond to Pine Cove, which could be largely offset by replacing owner mining with a contract mining model, which removes the need to purchase an equipment fleet.

Hammerdown as a Bridge Asset

Hammerdown is operational and trucking ore to Pine Cove Mill as it ramps toward commercial production. A PEA on the combined Hammerdown and Pine Cove properties projected approximately 50,000 ounces over the next two years, with modelled cash flow upwards of C$100 million at a US$4,000 per ounce gold price assumption.

Boyle was direct on the capital implications:

"The cash flow from the operation should offset the capital that is required to be spent this year at Hammerdown."

This reflects that the mine is not expected to be a net consumer of capital at the consolidated level. That matters for the financing picture. The US$75 million debt package does not need to carry the full weight of getting to Queensway production. Hammerdown's cash generation, even at gold prices below the current spot, reduces the gap.

Execution Risk: The New Investment Question

The 74,000-metre drill program completed in 2025, roughly 75% of which was directed at infill, grade control, condemnation, and geotechnical work, has materially reduced geological uncertainty at Queensway. Management described a confirmed high-grade zone of approximately 60 metres long by 35 metres deep by 40 metres wide, representing about the first year's worth of Phase 1 production, where drilling demonstrated the consistency of the core. For a high-grade open-pit mine, that level of continuity confirmation before the first blast is a meaningful reduction in grade risk for the first year of Phase 1 production, covering the highest-grade portion of the mine plan.

What remains is execution. New Found Gold is working with its engineering, procurement, and construction management (EPCM) contractor WSP on procurement packages for both the Queensway development and the Pine Cove Mill expansion, while applying for its environmental assessment (EA) certificate in the Second Quarter of 2026. Construction is targeting a 2026 start, with first Queensway production targeted toward the end of 2027. Management acknowledged that narrow-vein mining carries real day-to-day operational complexity, noting that the challenges the Hammerdown team navigates are ordinary by industry standards but real nonetheless. Queensway will demand the same disciplines.

Exploration Upside Remains a Secondary Driver

The 2026 drill program could well be larger than the 74,000 metres 2025 program, ramping from four rigs to six or seven over summer. Roughly 60% is allocated to upgrading Phase 2 and Phase 3 inferred resources ahead of the Third Quarter 2026 technical report update, which will present Phase 1 at near-feasibility quality while Phases 2 and 3 remain at PEA level. The remaining 40% targets new opportunities: follow-up at the Dropkick zone, the JBP fault zone running parallel to the Appleton fault, the Bullseye property acquired from Exploits in the Fourth Quarter of 2025, and a historically drilled area 65 kilometres to the south.

The split reflects where the project actually stands. A full feasibility study (FS) covering the entire Queensway development is not anticipated before Phase 2 and Phase 3 metallurgical test work and resource upgrades are completed, work that is ongoing through 2026.

What to Watch Next

The closing of the US$75 million debt package, expected in mid-April 2026, is the immediate catalyst to monitor. The cost of debt, covenants, and drawdown conditions will determine how much operational flexibility the company retains as it moves into construction. Closely tied to that is the EA application, which sets the regulatory timeline for Queensway development. Any significant delay to EA receipt would push back construction commencement and potentially defer first production beyond the late 2027 target.

Hammerdown's ramp-up will serve as an early read on management's ability to operate narrow-vein assets in this jurisdiction, with production rates and costs becoming clearer as the mine approaches commercial production later in 2026. The Third Quarter technical report will be the first disclosure to present Phase 1 economics at near-feasibility quality alongside updated Phase 2 and Phase 3 resource estimates, providing a more defensible basis for project valuation than the current PEA. Beyond that, a meaningful intercept from the 40% of drilling directed at new targets could broaden the resource base and reintroduce the exploration narrative that originally defined the company.

FAQs (AI-Generated)

It means the company has largely confirmed the presence and continuity of high-grade gold at Queensway, shifting investor focus to whether management can successfully build, finance, and operate the project on time and within budget.

The PEA outlines a phased, relatively low-capex development with strong early production, targeting 100,000 ounces annually in the first two years, which could accelerate payback and reduce financing risk.

Hammerdown serves as a bridge asset, generating near-term cash flow that can help offset development costs and reduce reliance on external financing for Queensway.

Key risks include permitting timelines, construction execution, cost control, Hammerdown’s production ramp-up, and the company’s ability to deliver Queensway on schedule.

Investors should watch for the US$75 million debt package closing, environmental assessment approval, Hammerdown reaching commercial production, and the Third Quarter of 2026 technical report update.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed