US Energy Security Policy Tightens Nuclear Fuel Markets & Pushes Uranium Futures Beyond $85/lb

Uranium prices surpass $85/lb as US policy shifts, AI data center demand, and supply constraints create structural market tightening for nuclear fuel investors

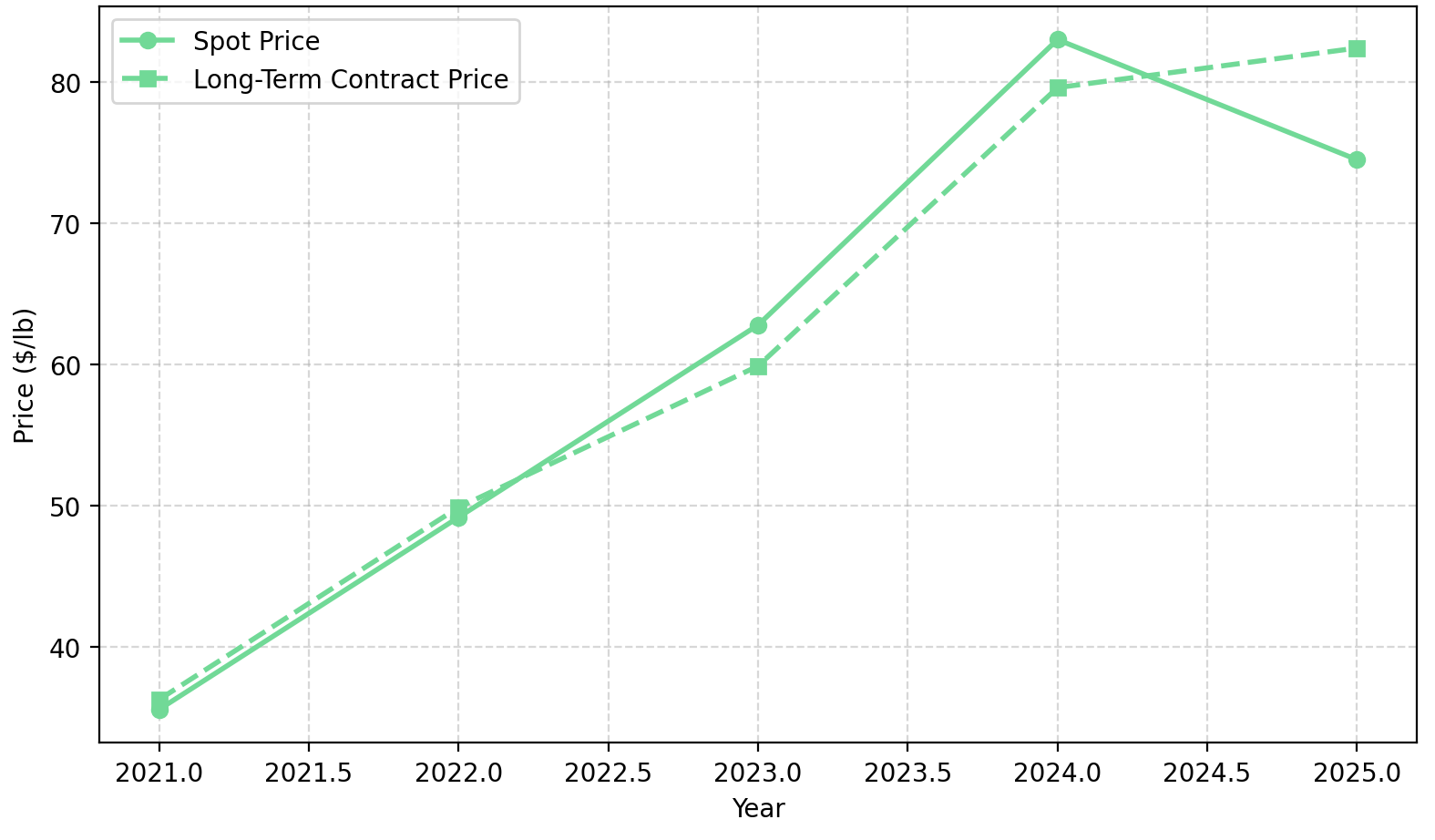

- Uranium spot prices reached $85.25/lb as of January 20, 2026, reflecting tightening physical markets rather than speculative momentum.

- US regulatory easing and $2.7 billion in federal support are reshaping the global nuclear fuel supply chain away from Russian dependence.

- Structural demand from AI-driven data centres and grid baseload requirements is reinforcing long-term uranium demand visibility.

- Institutional capital and physical funds are re-entering the market, with Sprott Physical Uranium Trust recently adding 100,000 pounds to holdings.

- Select uranium producers, developers, and explorers with jurisdictional clarity and permitting leverage are increasingly positioned as strategic assets rather than cyclical trades.

Why Uranium's Move Above $85/lb Matters More Than the Price Level

Uranium spot prices trading above $85/lb represent more than a technical resistance level being cleared. Unlike prior rallies driven largely by retail speculation or policy headlines, the current price action reflects structural supply tightening that has been building across the nuclear fuel cycle for several years. The uranium market operates under constraints that amplify macro shocks in ways that most commodity markets do not, creating both risks and opportunities for investors who understand the mechanics.

The uranium supply chain is characterised by long contracting cycles, typically extending five to ten years, and significant bottlenecks at the conversion and enrichment stages that sit between mine production and reactor consumption. When utilities or governments prioritise security of supply over spot pricing, which they increasingly are, price signals propagate through a system with limited near-term elasticity. This creates a market where policy decisions have outsized effects on pricing dynamics, and where supply responses lag demand signals by years rather than months.

US Policy Intervention & the Global Nuclear Fuel Map

The United States government has initiated one of the most significant policy shifts in the nuclear fuel sector in recent decades, ending dependence on foreign nuclear fuel and re-establishing domestic, high-assay low-enriched uranium (HALEU) production. This intervention extends beyond mine permitting into the downstream processing infrastructure that converts mined uranium into reactor-ready fuel. Understanding the scope of this policy shift is essential for evaluating which companies stand to benefit from the structural changes underway.

Regulatory Acceleration & the Strategic Reversal Away From Russian Supply

The US has moved to deregulate permitting and construction for domestic converters and enrichers while strictly enforcing a ban on Russian uranium imports. The $2.7 billion in federal contracts awarded to domestic enrichers and producers represents a substantial commitment to nuclear fuel supply chain reshoring, aimed at filling the approximately 25% supply gap previously filled by Russian sources. Critically, the binding constraint on uranium supply is not mine production alone but enrichment and conversion capacity, where Russian services historically held significant market share in Western supply chains.

This policy intervention positions uranium alongside semiconductors, rare earths, and critical minerals in the broader US industrial policy framework. Companies with domestic processing capabilities or exposure to non-Russian supply chains are being re-evaluated as strategic infrastructure assets rather than commodity producers subject to cyclical price risk.

Energy Fuels has positioned itself at the intersection of uranium production and downstream processing, operating two producing mines and the only conventional uranium mill in the United States. Mark Chalmers, Chief Executive Officer of Energy Fuels, notes:

"We are like no other company in the critical mineral space where we're building a critical mineral hub using our longstanding uranium processing capabilities but also the ability to mine and recover rare earth into oxides."

New Demand Signals Shifting Uranium From Cyclical to Structural

The demand side of the uranium equation is undergoing a transformation that distinguishes the current cycle from prior uranium bull markets. While reactor restarts and new construction contribute to demand growth, the emergence of AI-driven electricity consumption is creating a new category of baseload power demand that favours nuclear over intermittent generation sources.

AI, Data Centres & the Return of Baseload Power Economics

Data centre electricity consumption is projected to grow at rates that exceed grid capacity expansion in multiple jurisdictions. Unlike residential or commercial load growth, data centres require continuous power with high reliability standards that intermittent renewable sources cannot guarantee without substantial storage investment. Nuclear generation offers the baseload reliability that hyperscale computing facilities require, and major technology companies are increasingly evaluating long-term power arrangements with nuclear operators.

This shift from speculative demand to utility-backed physical procurement changes the nature of uranium price support. When infrastructure-scale computing facilities anchor capacity commitments, the demand visibility extends across contracting cycles rather than trading horizons. Nuclear capacity growth is now being driven by non-discretionary infrastructure investment, which provides a fundamentally different demand foundation than prior cycles driven by emerging market reactor construction that was often delayed or cancelled.

Capital Movement & Institutional Positioning

Institutional capital tends to move before utilities re-contract aggressively, and recent fund flow data suggests that sophisticated investors are positioning for sustained supply tightening. Physical fund accumulation has resumed, with the Sprott Physical Uranium Trust recently increasing holdings by 100,000 pounds, indicating fresh buying activity in a market trading at premium to net asset value.

The pattern of capital flows into uranium mirrors positioning in other policy-supported commodities such as copper and rare earths, where supply constraints are structural rather than cyclical. Institutional investors are treating uranium exposure less as a commodity trade and more as a policy-driven infrastructure allocation. This re-rating of uranium equities from cyclical to strategic is reflected in valuation multiples that remain elevated relative to historical norms despite spot price volatility.

How Different Uranium Business Models Respond to a Higher Price Deck

The uranium value chain contains distinct business models that respond differently to sustained price increases. Understanding these distinctions is essential for portfolio construction, as producers, developers, and explorers offer different risk-return profiles and exposure characteristics to the underlying commodity thesis.

Producers: Immediate Leverage & Contract Reset Optionality

Established uranium producers benefit from price increases through contract repricing rather than pure spot exposure. Most production is sold under long-term contracts with pricing mechanisms that reset periodically, providing leverage to higher price assumptions while maintaining cash flow visibility. Producers with all-in sustaining costs meaningfully below current price levels generate substantial operating margins that support capital returns, balance sheet strengthening, or expansion investment.

Energy Fuels exemplifies the producer model with integrated processing capabilities that extend beyond conventional mining margins. The company's Pinyon Plain operation maintains production costs between $23 to $30 per pound against sales prices exceeding $75, providing significant margin expansion at current price levels. Contract deliveries are ramping from 300,000 pounds in 2025 to between 620,000 and 880,000 pounds in 2026. The White Mesa Mill is also producing separated rare earth elements, with Phase 1 heavies separation planned for 2026 and a dedicated circuit targeted for 2028.

In-situ recovery assets are increasingly favoured under environmental and regulatory scrutiny because they involve minimal surface disturbance and lower capital intensity than conventional mining. enCore Energy operates as a US producer using ISR methods, with two licensed processing facilities in South Texas that provide production flexibility as wellfield development progresses. The company has demonstrated substantial operational improvement, with well installation time reduced from seven days to approximately 1.3 days, supporting production rate increases of 200% to 300% depending on measurement period.

William Sheriff, Executive Chairman of enCore Energy, quantifies the operational progress:

"Our production rate on a daily basis has gone depending on what time frame you're measuring it against from up 200% to up 300%."

Developers: Permitting Visibility & Valuation Sensitivity

Development-stage uranium companies benefit disproportionately as price assumptions move toward $90/lb because project economics improve non-linearly with commodity price increases. Internal rates of return on feasibility studies expand significantly as revenue assumptions rise while capital costs remain relatively fixed, creating valuation torque that attracts investor capital. The key variables for developers are permitting timelines, jurisdictional risk, and extraction methodology.

IsoEnergy represents a different development profile with both high-grade discovery potential and near-term production optionality through its Tony M mine in Utah. The company is advancing a bulk sampling programme extracting approximately 2,000 tons for processing at the White Mesa Mill under existing tolling agreements, while planning a winter 2026 drill programme of approximately 5,200 metres at the Hurricane deposit. Hurricane hosts the world's highest-grade published Indicated uranium resource at 34.5% U3O8, and the company has entered into a definitive agreement to acquire Toro Energy, with closing expected in the first half of 2026.

Philip Williams, Chief Executive Officer of IsoEnergy, explains the strategic positioning:

"We want to be one of those producers and be able to deliver material into a rapidly rising uranium price environment which we think is coming in the United States."

Explorers: Scarcity Value & Strategic Optionality

Exploration-stage uranium companies represent optionality on future supply gaps rather than near-term production. In a constrained supply environment, high-quality exploration assets become potential strategic acquisition targets for larger producers seeking to replenish depleted resource bases. The variables that matter most for explorers are geological grade, jurisdictional quality, and land position scale.

ATHA Energy controls approximately 7 million acres of exploration ground, including 3.8 million acres in the Athabasca Basin and 3.1 million acres in Nunavut. Recent drilling at the RIB North target returned 1.1 metres at 4.814% U3O8 and 0.5 metres at 8.160% U3O8, with the company pursuing a fully funded 10,000-metre diamond drill programme targeting the 31-kilometre RIB-Nine Iron Structural Corridor.

Troy Boisjoli, Chief Executive Officer of ATHA Energy, describes the geological context:

"We're seeing grades and thicknesses analogous to the Athabasca Basin style mineralization which was our thesis the whole time."

Risk Factors Investors Need to Underwrite

Despite favourable macro conditions, uranium investments carry specific risks that require careful evaluation. Permitting timelines remain extended despite regulatory support, with multi-year approval processes that can delay production schedules and capital deployment. The gap between spot price volatility and long-term contract pricing creates cash flow timing risks for companies transitioning from development to production.

Capital discipline and dilution risk warrant monitoring at higher price decks, as elevated valuations may encourage expansion projects or acquisitions that destroy shareholder value. Jurisdictional and environmental scrutiny continues across uranium projects, with Indigenous consultation requirements, water use restrictions, and reclamation obligations adding complexity to development timelines. Currency effects and geopolitical escalation risk remain relevant for companies with international operations or exposure to non-US production.

The Investment Thesis for Uranium

The strategic case for uranium exposure rests on several reinforcing factors that distinguish the current environment from prior cycles.

- US deregulation and sanctions have structurally constrained non-Russian fuel availability, creating policy-driven supply tightness that is unlikely to reverse within current contracting cycles.

- Data centre expansion and grid reliability requirements are driving long-term baseload power investment that favours nuclear capacity growth.

- Uranium holding above $85/lb with analyst models pointing toward sustained levels near $90/lb improves project economics across the development curve.

- Physical fund accumulation signals institutional confidence in sustained market tightening rather than speculative positioning.

- Producers, developers, and high-quality explorers in Tier-1 jurisdictions are increasingly being valued as strategic infrastructure assets rather than cyclical commodity exposures.

The uranium price move above $85/lb reflects systemic market tightening driven by policy intervention and structural demand growth, not cyclical enthusiasm that will dissipate with shifting sentiment. For investors evaluating uranium exposure, differentiating between business models across the value chain is essential. Producers offer margin expansion and cash flow visibility, developers provide valuation leverage to improving economics, and explorers represent optionality on supply scarcity.

The variables that matter most have shifted. Jurisdiction, permitting visibility, and contract exposure now outweigh pure resource size in determining which assets benefit from the current environment.

TL;DR

Uranium spot prices have moved above $85/lb, driven by structural supply tightening rather than speculation. The US government's $2.7 billion commitment to domestic nuclear fuel production—combined with sanctions on Russian uranium imports—is reshaping global supply chains. Meanwhile, AI-driven data center expansion is creating new baseload power demand that favors nuclear generation. Institutional capital is returning, with physical funds accumulating material. The investment case now hinges on jurisdiction, permitting visibility, and contract exposure rather than pure resource size. Producers offer margin expansion, developers provide valuation leverage, and explorers represent optionality on future supply scarcity.

FAQs (AI-Generated)

Unlike previous rallies driven by retail speculation, current prices reflect structural supply constraints across the nuclear fuel cycle. Policy interventions, including US sanctions on Russian uranium and $2.7 billion in federal support for domestic production, have created supply tightness that cannot be quickly resolved due to long contracting cycles and bottlenecks at conversion and enrichment stages.

Data centers require continuous, reliable baseload power that intermittent renewable sources cannot guarantee without substantial storage investment. Nuclear generation offers the reliability hyperscale computing facilities need, driving long-term power arrangements between technology companies and nuclear operators—shifting demand from speculative to utility-backed physical procurement.

Producers benefit through contract repricing and margin expansion at current price levels. Developers gain disproportionately as project economics improve non-linearly with rising prices. Explorers represent optionality on future supply gaps and may become acquisition targets for larger producers seeking to replenish resource bases.

Key risks include extended permitting timelines, cash flow timing mismatches between spot volatility and contract pricing, potential dilution from aggressive expansion at elevated valuations, jurisdictional and environmental scrutiny, and geopolitical factors affecting international operations.

Jurisdiction, permitting visibility, and contract exposure now outweigh pure resource size. Companies in Tier-1 jurisdictions with regulatory clarity, domestic processing capabilities, or exposure to non-Russian supply chains are being re-evaluated as strategic infrastructure assets rather than cyclical commodity plays.

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

Stay Informed