Central Bank Gold Buying & US Fiscal Pressures Support Higher Gold Prices & Equity Valuations

Central bank purchases of 244 tonnes of gold in Q1 2026 and rising US fiscal pressures are supporting gold prices and improving valuations across equities.

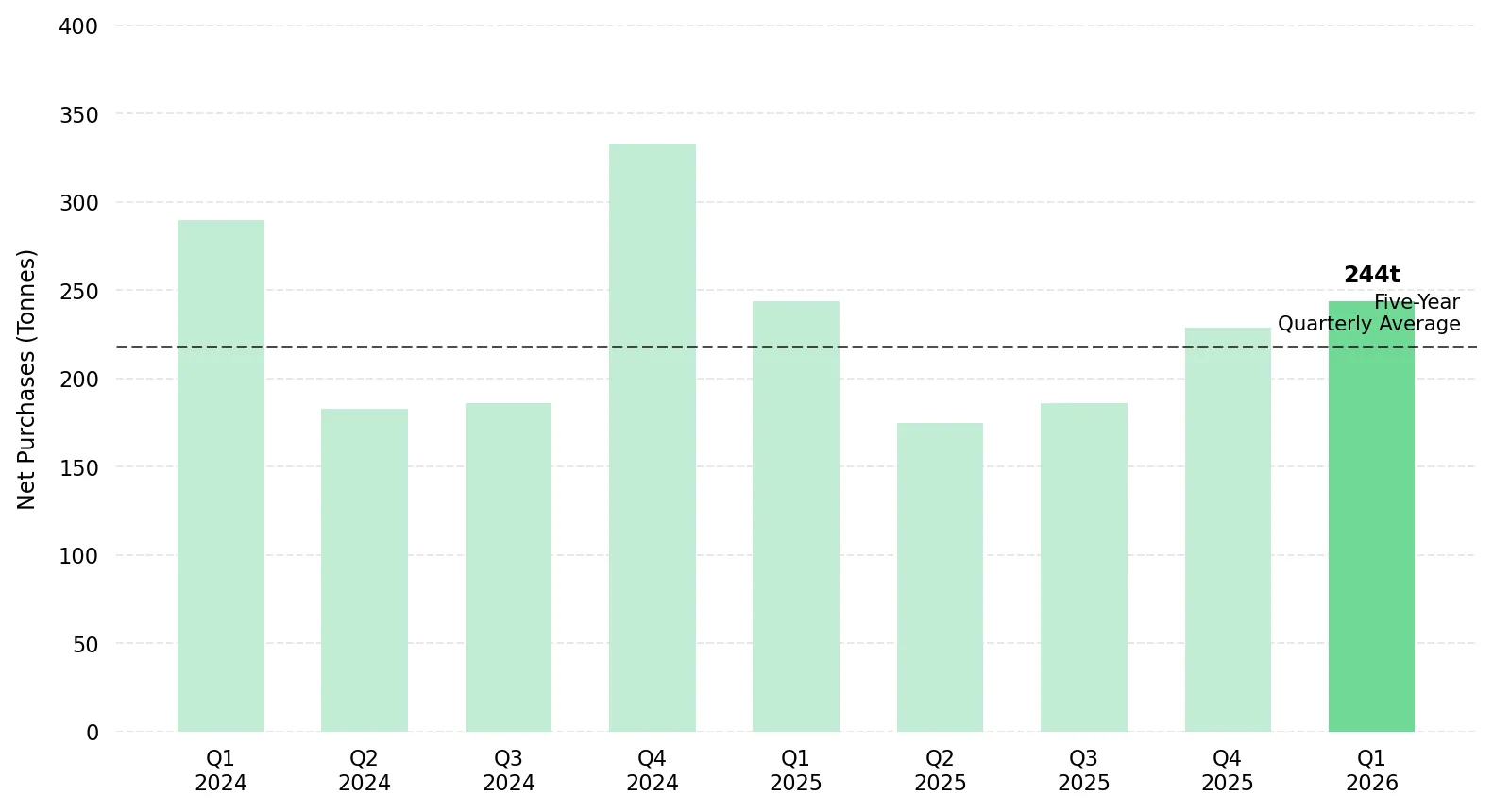

- Central banks purchased a net 244 tonnes of gold in Q1 2026, the highest quarterly total in more than 25 years, as sovereign institutions diversified reserves away from US dollar assets, increasing demand for gold and supporting higher valuations for development-stage projects.

- The US debt ceiling increased to $41.1 trillion, rising Treasury issuance, and Moody's 2025 sovereign downgrade have increased concerns about long-term fiscal sustainability, supporting demand for gold as a reserve asset and portfolio hedge.

- Gold declined approximately 10% while Brent crude rose 37% following the February 2026 Iran conflict, as investors focused on the risk of higher inflation and Fed rate hikes, creating a potential buying opportunity if energy prices moderate and rate expectations weaken.

- Development-stage gold companies with low AISC profiles, advancing permits, and near-term production milestones can benefit from higher gold prices, as EV/oz discounts to producers narrow and project economics improve.

- The June 16-17, 2026 FOMC meeting and updated dot plot will provide the market's clearest signal on the future rate path, with implications for gold prices and the valuation of development-stage projects.

Reserve Allocation Shifts Continue to Support Gold Demand

Central banks, rather than retail investors or futures traders, are the largest source of gold demand supporting prices in 2026. According to the World Gold Council's Q1 2026 data, central banks purchased a net 244 tonnes of gold, exceeding both the previous quarter and the five-year quarterly average. Central bank gold purchases accelerated after Russia's foreign-currency reserves were frozen in 2022, highlighting the appeal of gold as a reserve asset that is not exposed to foreign sanctions.

The National Bank of Poland purchased 20 tonnes of gold in February 2026, increasing its reserves to 570 tonnes, or 31% of total reserves, against a stated target of 700 tonnes. China holds less than 10% of its reserves in gold, compared with approximately 70% for the US, Germany, France, and Italy, indicating potential for further central bank gold purchases. Central bank net purchases now absorb approximately one-third of annual global mine production, supporting gold demand through reserve management policies rather than investor sentiment.

The IMF's April 2026 World Economic Outlook forecast global growth of 3.1% for 2026 and warned that fiscal policy remains too loose in many advanced economies, while IMF management highlighted the risk of inflation expectations becoming unanchored, conditions that can support demand for gold as a non-liability asset.

Iran Conflict Drives Energy Inflation & Weighs on Gold

Gold hit an all-time high of approximately $5,602 per ounce on January 28, 2026. By late May, following US-Israeli military operations against Iran on February 28, spot gold had fallen to approximately $4,540, about 10% below its January high, while Brent crude had risen approximately 37%. Rising oil prices increased inflation expectations and concerns about additional Fed rate hikes, weighing on gold despite the geopolitical conflict. April CPI rose 3.8% year-over-year, while the April PCE deflator increased 3.8% headline and 3.3% core, contributing to a market-implied 46% probability of a December 2026 rate hike.

On May 28, 2026, gold fell below its 200-day moving average intraday and reached a weekly low of $4,366.23 before recovering to close above $4,500, suggesting continued buying interest despite concerns about inflation and higher interest rates.

Elevated Gold Prices Strengthen Project Economics Across Gold Developers

Development-stage projects trading below feasibility-study valuations can benefit from higher gold prices, as fixed-cost AISC structures increase project NPV and EV/oz multiples. The World Bank's April 2026 Commodity Markets Outlook projects its precious metals price index to rise 42% in 2026 relative to 2025 averages. Goldman Sachs maintains a $5,400 year-end gold price target; J.P. Morgan holds its forecast at $6,000.

Higher Gold Prices Can Expand Project NPV and Investment Returns

U.S. Gold Corp's CK Gold Project in Wyoming demonstrates how higher gold prices can increase project value. The company's March 2026 Feasibility Study, completed under the SK-1300 standard by Halyard Micon International, delivered an after-tax NPV of $632 million at a $3,250 per ounce base case, rising to $1.4 billion at $4,500 per ounce. The project contains 1.598 million gold-equivalent ounces of proven and probable reserves, is fully permitted on State of Wyoming land, and does not require approvals from the Bureau of Land Management or Army Corps of Engineers.

Luke Norman, Chairman of U.S. Gold Corp, highlights how higher gold prices can significantly expand project economics at the CK Gold Project:

"Even at $4,500 gold, you're dealing with a $1.4 billion NPV and an IRR of just under 50%. Realistically, $4,500 gold is where we're looking right now and below spot. This project is so well leveraged to the price of gold."

Early Cash Flow Can Fund Resource Growth and Reduce Dilution

Cabral Gold is advancing the Cuiú Cuiú Gold District through a phased development strategy designed to unlock district-scale value. The company's planned Phase 1 oxide heap leach project carries a projected AISC of $1,210 per ounce, providing significant leverage to higher gold prices while creating a potential source of internally generated capital for exploration, resource growth, and future development.

Alan Carter, President and Chief Executive Officer of Cabral Gold, explains the strategy behind Phase 1 development:

"We think the best way of advancing that gold district is not to rely on continually diluting the share structure, but to develop an initial project to mine the near-surface oxide material. That will provide a significant amount of cash to allow us to develop the larger district, explore the larger district, and grow the global resource base within the Cuiú Cuiú district."

Higher Gold Prices Are Increasing the Value of Grade and Margin

Higher gold prices create larger valuation gains for projects with high grades and low operating costs. As gold prices rise, high-grade, low-cost projects generate larger increases in cash flow because revenue rises faster than operating costs. Higher cash flow expands operating margins and shortens payback periods, increasing project NPV.

Central banks purchased a net 244 tonnes of gold in Q1 2026, while concerns about US fiscal sustainability continue to support demand for gold as a reserve asset. Elevated interest rates have increased financing costs across the mining sector. Higher financing costs increase the appeal of projects that can generate cash flow at current gold prices and reduce reliance on equity financing. High-grade deposits, low AISC profiles, existing infrastructure, and phased development plans can help companies fund resource growth without additional equity issuance.

Goldman Sachs and J.P. Morgan maintain gold price forecasts above current spot levels, supporting the case for projects with strong cash-flow generation. If gold prices remain elevated, projects that can fund growth from cash flow may command higher valuations than projects that rely on external financing.

Multiple Paths to Margin Expansion in a Higher Gold Price Environment

Higher-grade deposits support lower unit costs and stronger cash flow generation, particularly when combined with disciplined capital management. For development-stage companies, this combination can reduce financing requirements, support self-funded growth, and improve project economics at current gold prices.

New Found Gold is advancing the Queensway Gold Project in Newfoundland and Labrador toward production in late 2027, with high grades and a low projected cost structure. Queensway's initial production years target ore grades of 10 to 12 grams per tonne gold, five to ten times the global mine average, with a PEA-defined AISC of $1,300 per ounce. The company secured $220 million in total capital through a $105 million facility and a $115 million equity raise with anchor investors including Eric Sprott, fully funding the project to production.

Keith Boyle, Chief Executive Officer of New Found Gold, explains how Queensway's grade profile translates into margins and future cash flow generation:

"Queensway in the first couple of years will be processing 10 to over 12 g/t material. We're targeting 100,000 oz from Queensway alone. At an all-in sustaining cost of $1,300 per ounce, based on the PEA we put out last year, you're looking at more than $2,300 of free cash flow at today's prices."

Higher-Grade Mine Sequencing Can Improve Capital Efficiency

Tudor Gold holds an 80% interest in Treaty Creek in British Columbia's Golden Triangle, where the Goldstorm Deposit contains 24.9 million indicated ounces of gold grading 0.85 grams per tonne, 148.7 million ounces of silver, and 3.048 billion pounds of copper. Management is evaluating a higher-grade underground mining scenario as an alternative to a large-scale open-pit development.

Joseph Ovsenek, President and Chief Executive Officer of Tudor Gold, explains the proposed underground development approach:

"We currently have a preliminary economic assessment underway looking at an underground mine through longhole stoping, a higher cut-off grade, and paste backfill. The goal is to mine 10,000 tonnes a day and create a 200,000 to 300,000 ounce gold producer for 20 years plus."

Existing Infrastructure Can Enhance Discovery Value

Hycroft Mining Holding Corporation's mine in Nevada contains a Measured and Indicated resource of 16.4 million ounces of gold and 562.6 million ounces of silver, alongside $189 million in cash, no debt, and more than $1 billion of existing site infrastructure.

Diane Garrett, President and Chief Executive Officer of Hycroft Mining, explains why the Brimstone and Vortex discoveries have attracted institutional interest:

"Nobody thought there was high-grade at Hycroft. This is the game-changer. It's attracting the attention of the market and becoming the focus of institutions. They agree with our vision and our plan."

Near-Surface Mineralization Can Expand Development Options

Cobra Resources is advancing the Manna Hill Project in South Australia's Nakara Arc, where its 2026 RC drilling at the Blue Rose copper-gold system intersected 74 meters grading more than 1% copper and approximately 0.25 grams per tonne gold from near surface, with skarn mineralization mapped across 1.6 kilometres of strike.

Where the Next Generation of Gold Supply Can Be Defined

P2 Gold's May 2026 drilling at the Lucky Strike Zone returned 183 grams per tonne gold and 4.0% copper over 1.52 metres within a broader interval of 1.04 grams per tonne gold and 0.35% copper over 53.34 metres, extending mineralisation 100 metres into previously undrilled ground. The company is completing a feasibility study based on a 12 million tonne per year operation targeting annual production of approximately 150,000 ounces of gold and 45 to 50 million pounds of copper.

US Fiscal Pressures Increase Gold's Appeal as a Reserve Asset

Gold demand in 2026 is being influenced by both geopolitical risks and US fiscal conditions. In July 2025, the One Big Beautiful Bill Act raised the US debt ceiling by $5 trillion to $41.1 trillion, the largest debt-limit increase in US history. According to CBO fiscal year 2026 projections, annual federal interest payments are approaching $1 trillion, increasing the fiscal cost of higher interest rates. Moody's downgraded US sovereign credit in 2025, citing concerns about the country's fiscal position. Higher interest rates increase federal borrowing costs, while lower real yields improve the relative appeal of non-yielding assets such as gold. The April 2026 FOMC vote was 8-4, the most dissents since October 1992, highlighting growing disagreement over the future path of interest rates.

The Investment Thesis for Gold

- Central banks purchased a net 244 tonnes of gold in Q1 2026, absorbing approximately one-third of annual global mine production and supporting demand through reserve management policies rather than investor sentiment.

- The US debt ceiling of $41.1 trillion, approximately $1 trillion in annual federal interest payments, and Moody's sovereign downgrade support demand for non-liability assets such as gold.

- Development-stage projects with completed feasibility studies, low AISC profiles, and permits in jurisdictions including Wyoming, Nevada, Newfoundland, and British Columbia can benefit from higher gold prices, which increase project NPV and can narrow EV/oz discounts to producers.

- High-grade projects generating strong cash flow at current gold prices can help fund exploration and reduce dilution risk, while exploration-stage assets targeting resource growth ahead of feasibility studies offer exposure to potential project expansion.

- Development timelines of 18 to 36 months position new projects to enter production during a period when Goldman Sachs and J.P. Morgan forecast gold prices at or above current spot levels, while the June 16-17 FOMC meeting could influence near-term valuations across the sector through its impact on interest-rate expectations.

Gold demand in 2026 is being supported by central bank purchases that absorbed a net 244 tonnes in Q1 and by concerns over US fiscal sustainability. Higher gold prices increase project NPV for developers with completed economic studies, improve cash flow potential for low-cost projects advancing toward production, and can justify larger resource inventories at exploration-stage assets. For investors, the key differentiator is execution: companies that convert higher gold prices into resource growth, feasibility-study upgrades, permitting milestones, or production cash flow are more likely to capture valuation gains than companies relying solely on commodity-price appreciation.

TL;DR

Central banks purchased a net 244 tonnes of gold in Q1 2026, absorbing roughly one-third of annual mine supply and reinforcing gold's role as a reserve asset amid rising US debt and fiscal concerns. Although gold fell after the Iran conflict as higher oil prices increased inflation and rate hike expectations, major institutions including Goldman Sachs and J.P. Morgan continue to forecast elevated gold prices. Higher gold prices improve project economics, particularly for companies with low AISC profiles, high-grade deposits, secured permits, existing infrastructure, and resource growth potential, creating opportunities across both development and exploration-stage gold equities.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed