Central Banks Buy Gold Through Worst Quarter Since 2013, Signaling Long-Term Reserve Demand Remains Intact

Gold's worst quarter since 2013 failed to stop central bank buying, reinforcing long-term reserve demand despite higher real yields.

- Gold fell 14.1 percent in the second quarter of 2026, its steepest quarterly decline since 2013, as Fed policy uncertainty and the renewed US-Iran conflict lifted real yields, increasing the opportunity cost of holding non-yielding gold.

- China's central bank purchased 15 tonnes of gold in June, its largest monthly purchase since October 2023, as spot gold traded near an eight-month low, indicating official-sector buying continued despite the second-quarter correction.

- The European Central Bank's June 2026 review of the international role of the euro confirmed that gold now accounts for roughly 27 percent of global reserve assets, compared with 22 percent for US Treasuries, marking the first time since 1996 that gold's share has exceeded Treasuries.

- Development-stage companies such as U.S. Gold Corp are using gold-price assumptions of $3,250 an ounce or lower in their feasibility studies, leaving project economics well below current spot prices despite the second-quarter correction.

Higher Real Yields Drive Gold Lower & Official Reserve Buying Holds Firm

Gold posted its worst quarterly performance since 2013 between April and June 2026, falling 14.1 percent over the period. Spot gold briefly traded below $4,000 an ounce on June 24, its first move beneath that level since November 2025, before recovering to close the quarter at $4,008.

The more important signal than the 14.1 percent decline was that central banks continued adding to gold reserves throughout the correction. Gold prices weakened as higher real yields weighed on demand, even as central banks continued increasing official gold reserves. The cyclical driver was higher real yields as Fed policy uncertainty and the renewed US-Iran conflict raised the opportunity cost of holding non-yielding gold. At the same time, central banks continued adding gold to official reserves despite lower prices, indicating that reserve allocation decisions were driven by long-term policy rather than short-term market moves. The following analysis distinguishes these macro drivers and examines how development-stage gold companies are designing projects to remain profitable across both scenarios.

Fed Policy Uncertainty & Middle East Conflict Lift Real Yields

The second-quarter decline reflected two identifiable drivers, Fed policy uncertainty and the renewed US-Iran conflict, both of which raised real yields and increased the opportunity cost of holding non-yielding gold.

Fed Policy Uncertainty Supports Higher Real Yields & Weighs on Gold

At its June 17 meeting, the Fed held rates at 3.50 to 3.75 percent, while Chair Kevin Warsh declined to submit a dot-plot projection, becoming the first Fed chair to withhold one since the tool was introduced in 2012. Nine of the eighteen voting participants projected a rate hike before year-end, while the July 8 meeting minutes cited tariffs, higher energy prices, and supply disruptions linked to the Strait of Hormuz as upside risks to inflation. Limited forward guidance and a hawkish policy outlook increased uncertainty over future interest rates, supporting higher real yields and weighing on gold prices.

Middle East Conflict Fuels Inflation Expectations & Weighs on Gold

The ceasefire between the US and Iran broke down in early July after attacks on commercial vessels in the Strait of Hormuz, prompting US retaliatory strikes and a broader Iranian military response across the Gulf. Brent crude climbed toward $79 a barrel, its highest level since June 19, while tanker traffic through the strait slowed to near-standstill levels. The transmission mechanism to gold ran through inflation expectations: higher oil prices increased the risk of inflation remaining elevated, reinforcing expectations of tighter Fed policy, supporting higher real yields, and raising the opportunity cost of holding gold. This backdrop limited gold's rebound between July 8 and July 10 as higher real yields offset support from safe-haven demand.

Official Reserve Buying & Gold's Rising Reserve Role Support Long-Term Demand

While higher real yields weighed on gold prices during the second-quarter correction, central banks continued adding to official reserves, indicating that reserve allocation decisions remained unchanged despite lower prices.

China Buys Gold Into Price Weakness, Reinforcing Official Reserve Demand

China's central bank added 15 tonnes of gold in June, its largest monthly purchase since October 2023 and its twentieth consecutive month of reserve growth, according to the State Administration of Foreign Exchange. The purchase coincided with spot gold trading near an eight-month low of about $4,002, indicating that reserve accumulation continued during price weakness rather than after higher prices. China's gold reserves now total 2,346 tonnes.

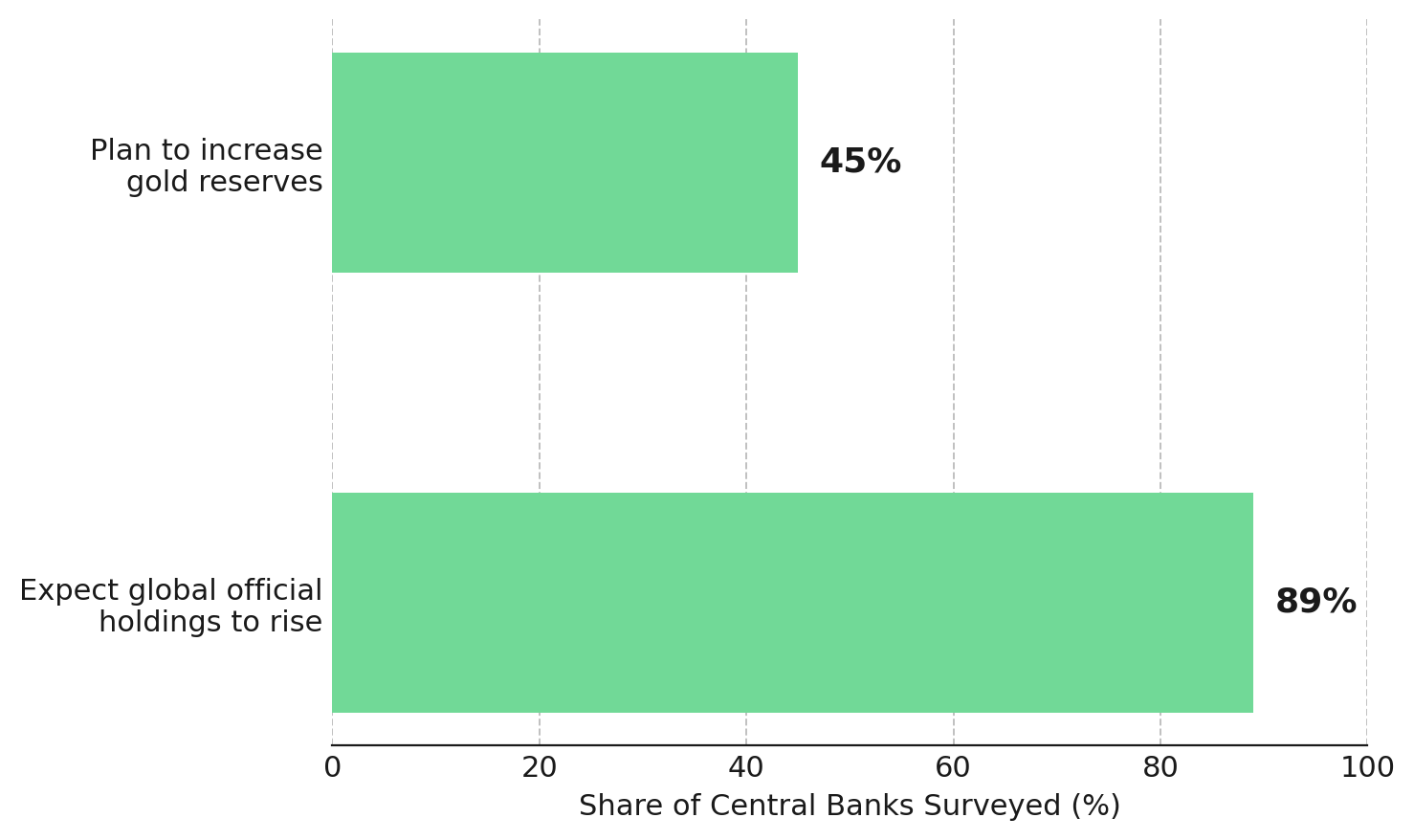

The World Gold Council's 2026 Central Bank Gold Reserves Survey, published in June, found that a record 45 percent of the 76 central banks surveyed plan to increase gold reserves over the next 12 months, while 89 percent expect global official holdings to rise.

Gold Overtakes US Treasuries in Global Reserves

The European Central Bank's June 2026 review of the international role of the euro found that gold accounted for roughly 27 percent of global reserve assets, up from 20 percent at the end of 2024, while the share held in US Treasuries fell to 22 percent from 25 percent over the same period. It marks the first time since 1996 that gold's share has exceeded US Treasuries, with the ECB attributing the shift to higher gold prices and continued diversification by reserve managers away from dollar-denominated assets. The ECB's three-decade dataset suggests that long-term reserve allocation decisions are driven by strategic diversification rather than short-term price movements.

Official Reserve Buying Supports Gold & Conservative Feasibility Assumptions Protect Project Economics

Continued central bank buying during the second-quarter correction shifts the focus to development-stage companies using conservative gold-price assumptions in their feasibility studies, allowing projects to remain economic even if gold trades below recent highs.

Conservative Gold Price Assumptions Preserve Project Economics

US Gold Corp, a development-stage company advancing the fully permitted CK Gold Project in Wyoming, based its definitive feasibility study on a gold price of $3,250 an ounce, which the company described as conservative relative to prevailing market prices. At that gold price, the study generates an after-tax net present value of approximately $630 million and an internal rate of return of about 30 percent, with copper contributing roughly 30 percent of project value.

US Gold Corp Executive Chairman Luke Norman frames the gap between that base case and where gold has traded since:

"We ran $3,250 as our base case, which is significantly below consensus. At $3,250, you see an after-tax NPV of $630 million, just under 30 percent IRR. Well, we start pushing up towards the spot price in gold and you can see a tremendous shift, clearly most good deposits do in a higher gold price environment."

Higher Project Costs Increase Gold Price Sensitivity While Preserving Project Value

Development-stage projects differ significantly in their sensitivity to lower gold prices because operating costs and feasibility assumptions vary by asset. Hycroft Mining Holding Corporation's June 2026 independent economic study for its Nevada project estimated total costs of just over $2,100 per gold-equivalent ounce, making project economics more sensitive to lower gold prices than projects with lower operating costs. Even so, the study estimated an after-tax net present value of $4.3 billion under its base-case metal prices, increasing to $10.0 billion using spot prices.

Project Optimization Accelerates Cash Flow & Reduces Gold Price Dependence

Cabral Gold, also development-stage, offers a different kind of cushion through its Cuiú Cuiú district in Brazil, a low-cost heap-leach operation that was more than 70 percent built as of April 2026 and is targeting commercial production in the fourth quarter of 2026, with financing already in place. Where Hycroft's economics lean on a higher price persisting, Cabral's near-term timeline is designed to generate cash flow largely independent of where gold trades over the next two quarters, a distinction President and Chief Executive Officer Alan Carter ties directly to current pricing:

"There's still a healthy margin at today's gold price, about $4,300 US dollars a ton. We still expect to make about $3,000 US dollars an ounce that we produce."

Company-Specific Execution & Project Milestones Drive Valuation Beyond Gold Prices

Gold prices are only one driver of valuation for development-stage mining companies, alongside project permitting, resource quality, and operating costs. Permitting milestones, resource updates, and by-product exposure can change project valuations independently of gold prices, requiring each development-stage company to be assessed on its own operating and technical progress.

Permitting Timelines Drive Project Value Beyond Gold Prices

New Found Gold, a development-stage company advancing the Queensway project in Newfoundland, received a decision letter on July 3, 2026 requiring an Environmental Preview Report before advancing through the provincial environmental review process, extending the timeline to a construction decision by six to nine months under the province's published regulatory calendar. The revised project timeline reflects regulatory review requirements rather than changes in gold prices, making permitting progress the primary near-term driver of project value.

Resource Updates & Legal Developments Drive Company Value Beyond Gold Prices

Tudor Gold, a development-stage company advancing the Treaty Creek project in British Columbia's Golden Triangle, has seen its Goldstorm deposit recalculated across indicated and inferred categories, from approximately 15 million ounces of gold equivalent in 2021 to approximately 28 million ounces on an open-pit basis in 2024 to approximately 25 million ounces of gold alone, reported separately from silver and copper, on an underground basis in 2025. Those swings reflect changes in mining method and reporting convention as much as new drilling.

Multi-Commodity Exposure Reduces Reliance on Gold Prices Alone

P2 Gold, an exploration-stage company advancing the Gabbs project in Nevada, is developing a copper-gold porphyry deposit with exposure to both central bank demand for gold and industrial demand for copper, providing commodity diversification within a single project. Management is optimizing the project ahead of a feasibility study by targeting annual throughput of 12 million tonnes, up from 9 million in the preliminary economic assessment, while advancing mill start-up from year six to year three to improve project economics.

President and Chief Executive Officer Joseph Ovsenek, ties the updated resource estimate directly to that feasibility schedule:

"We'd like to get a resource estimate out by the end of the summer, and that will feed right into our schedule to have that feasibility done by year end."

Cobra Resources offers a similar multi-commodity profile through its Manna Hill project in South Australia, where reverse-circulation drilling at the Blue Rose prospect returned intercepts of up to 74 meters grading 1.02 percent copper and 0.25 grams per tonne gold, prompting a follow-up six-hole, 1, 800-meter diamond drilling program launched in June 2026 to test for a larger porphyry system at depth. The London-listed company sold its separate Wudinna gold assets to Barton Gold in 2025 to concentrate on copper and, at its Boland project, ionic rare earths extracted through in-situ recovery, with a maiden rare earth resource estimate targeted for mid-2026.

Core Inflation & Central Bank Demand Shape Gold's Outlook

The June CPI report matters less than whether core inflation extends its recent trend, rising from 2.6 percent in March to 2.8 percent in April and 2.9 percent in May. Lower gasoline prices following the temporary US-Iran ceasefire may reduce headline inflation, but core inflation will carry greater weight for Fed policy. Higher-than-expected core inflation, combined with the Fed's hawkish policy signals and renewed conflict in the Gulf, would strengthen expectations of a rate hike at the Fed's July 28–29 meeting, supporting higher real yields and extending pressure on gold prices.

These pressures have not altered the long-term shift in central bank reserve allocation toward gold. China added to its reserves while gold traded near an eight-month low, the European Central Bank confirmed that gold's share of global reserve assets exceeded US Treasuries for the first time since 1996, and the World Gold Council's June 2026 survey found record central bank interest in increasing gold reserves. The companies discussed above reflect different ways of positioning for this environment. U.S. Gold Corp and Cabral Gold have based project economics on conservative gold-price assumptions, while Tudor Gold and P2 Gold provide exposure to longer-term project development that depends more on execution milestones than on a single inflation release.

The Investment Thesis for Gold

- Gold's expanding role in central bank reserves extends beyond a single quarter, as official-sector purchases continued during the second-quarter correction and World Gold Council survey data indicate that reserve managers plan to keep increasing gold holdings over the next 12 months.

- Development-stage projects using conservative base-case gold prices in their feasibility studies remain economically viable despite the second-quarter correction.

- Development-stage companies with near-term production timelines and conservative project economics are generally less dependent on sustained high gold prices than earlier-stage projects that have yet to complete feasibility studies or permitting.

- Published permitting timelines and established regulatory processes improve visibility on project development schedules, even when environmental reviews extend construction decisions.

- Copper-gold porphyry projects provide exposure to both central bank demand for gold and industrial demand for copper, reducing reliance on a single commodity market.

- Resource updates, feasibility studies, and permitting decisions are company-specific catalysts that affect project valuations independently of short-term gold price movements because each follows its own development and regulatory timeline.

Gold's second-quarter decline was real, but continued central bank reserve allocation toward gold was equally significant. Central banks continued buying throughout the correction, while the European Central Bank confirmed that gold's share of global reserve assets exceeded US Treasuries for the first time since 1996. Development-stage companies will continue to respond differently depending on their project economics, permitting progress, and development milestones. While inflation data and Fed policy will influence gold prices over the coming months, continued central bank reserve accumulation remains the longer-term driver identified throughout this analysis.

TL;DR

Gold fell 14.1 percent in the second quarter of 2026 as Fed policy uncertainty and renewed Middle East conflict pushed real yields higher, increasing the opportunity cost of holding bullion. Despite the correction, central banks continued accumulating gold, with China making its largest monthly purchase since October 2023 and the European Central Bank confirming gold has overtaken US Treasuries in global reserve assets for the first time since 1996. The article concludes that long-term reserve allocation remains intact, while development-stage gold companies using conservative feasibility assumptions and advancing project milestones are better positioned to withstand short-term price volatility.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

Stay Informed