Gold Falls to US$4,520/oz on Forced Liquidation: Persistent Inflation, Slowing Growth, and Fed Constraints Hold

Gold drops to US$4,519.69/oz on forced institutional liquidation amid cross-asset margin calls, stagflation conditions and technical support levels intact.

- Gold declined to US$4,519.69/oz per the World Gold Council spot price chart dated March 30, 2026. Cross-asset margin calls forced institutional investors to liquidate gold to cover losses elsewhere, a process that suppresses price regardless of underlying fundamentals.

- Cross-asset margin calls forced institutional investors to liquidate gold — a pattern observed during the March 2020 and 2008 stress events before gold resumed its advance in both instances.

- Elevated energy prices are transmitting persistent inflation into global production and transportation costs, reinforcing stagflation conditions that historically correlate with sustained gold demand.

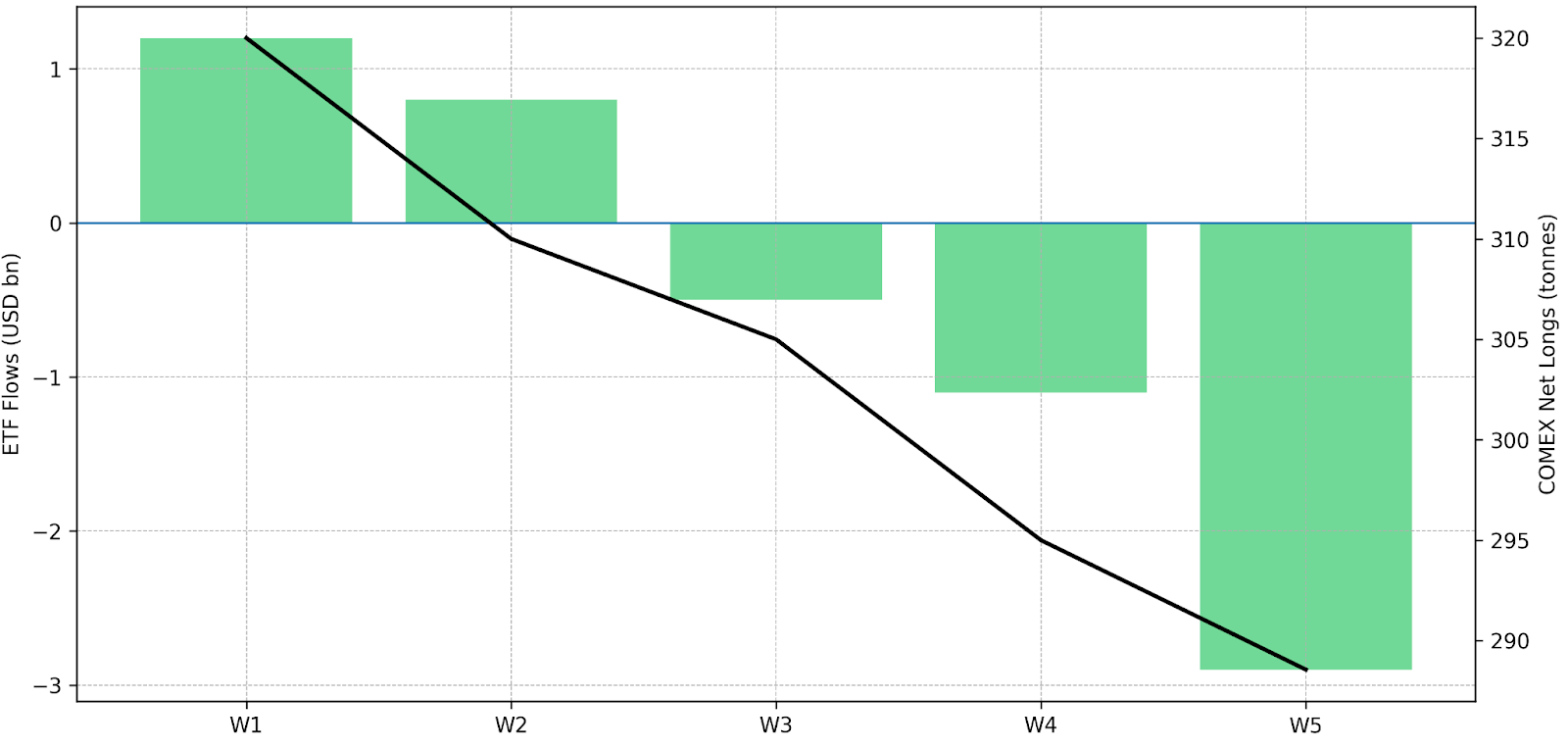

- North American and European gold ETF outflows exceeded US$2.9 billion in the week ending March 27, 2026; COMEX money manager net longs stood at 288.56 tonnes as of March 24, consistent with de-risking rather than bearish conviction.

- Key technical support sits at US$4,074.92 and US$4,113.54; a sustained weekly close below US$4,074.92/oz would signal a correction toward the October 2025 lows at US$3,887/oz.

Understanding the Sell-Off: Liquidity Mechanics

This dynamic recurred during the March 2020 COVID liquidity crisis and the 2008 Global Financial Crisis, with gold resuming its advance in both instances once liquidity conditions stabilized. ETF outflows exceeding US$2.9 billion in the week ending March 27, 2026 reflect liquidity management rather than a directional allocation shift. COMEX money manager net longs at 288.56 tonnes as of March 24 show reduced exposure without a buildup of active short interest. A genuine fundamental sell-off would require sustained real yield increases, reaccelerating economic growth, or meaningful geopolitical de-escalation, none of which are currently in place.

Stagflation Risk & Gold Demand

The University of Michigan Survey of Consumers recorded a 1-year inflation expectation of 3.6% and a 5–10 year expectation of 3.5% as of the most recent release, reflecting persistent inflation in consumer expectations even as growth indicators weaken. Brent Crude at US$112.57/bbl as of March 27, 2026, sustains elevated input costs across global production and transportation, feeding through to consumer prices independent of Federal Reserve policy settings.

Elevated energy costs feed directly into production and transportation costs globally, generating sticky consumer inflation even as growth weakens. The Federal Reserve faces a direct trade-off: cutting rates risks re-accelerating inflation while holding rates elevated risks contracting an already slowing economy. This policy constraint prevents the sustained real yield increases that would erode gold's carry advantage.

Positioning & Flows: Caution, Not Capitulation

Institutional flow data points to a consolidation phase rather than a reversal. ETF outflows reflect short-term liquidity management rather than a reallocation away from gold as an asset class.

For producers, operating cash flow provides a buffer against tighter capital markets. Integra Resources operates Florida Canyon in Nevada and is targeting 80,000-90,000 ounces per year in 2027 and 2028. President and Chief Executive Officer George Salamis on the company's current financial position:

"In terms of our current cash position for the company, it now sits at over $110 million in the treasury."

That treasury position enables project advancement without requiring dilutive financing through the current capital market cycle.

i-80 Gold is a Nevada producer advancing the Lone Tree autoclave refurbishment, targeting end-2027 first production from that facility and a ramp to 150,000–160,000 oz/year in 2028. Chief Operating Officer Paul Chawrun on the production timeline:

"We'll have the Lone Tree plant producing gold by the end of 2027 with a bit of a ramp-up in 2028 and in the range of about 150,000, depending on the grade, to maybe 160,000 ounces per year."

Mining Equities: Margin Resilience, Project Economics & Asymmetric Upside

New Found Gold's Queensway PEA reports a life-of-mine AISC of US$1,256/oz at a US$2,500/oz gold base case generates a margin that renders gold price consolidation operationally irrelevant at Queensway. Chief Executive Officer Keith Boyle on margins at the run-of-mine level:

"The cost of trucking plus processing is about a gram, we're shipping 9 to 10 gram material, you make lots of money at an all-in sustaining cost of $1,300."

Hycroft Mining's 2026 Mineral Resource Estimate confirms 16,414,000 ounces gold and 562,575,000 ounces silver measured and indicated in Nevada. President and Chief Executive Officer Diane Garrett on the company's balance sheet positioning through prior volatility:

"We eliminated all debt, brought in 85% institutional shareholder investment, and allowed the company to have $200 million in cash."

Serabi Gold produces from the Palito Complex and Coringa Mine in Brazil's Tapajós province, generating EBITDA of US$48.2 million year-to-date through Q3 2025 at an AISC of US$1,816/oz.

Developers: Project Economics Through Volatility

Tudor Gold's Treaty Creek in British Columbia holds an indicated resource of 24.9 million ounces at 0.85 g/t gold per the January 2026 resource estimate, with 4.0 million inferred ounces. President and Chief Executive Officer Joseph Ovsenek on Tudor Gold's development strategy:

"A smaller, higher-grade underground mine with a small footprint is really the way to move forward quickly in the Golden Triangle… A capex of a billion to a billion and a half is something we can handle."

U.S. Gold Corp's CK Gold in Wyoming holds four active state permits with no federal permitting required, targeting production by 2027 or 2028 subject to feasibility study completion. President, Chief Executive Officer and Director George Bee on the concentrate product:

"We take copper and gold ore, put it through a concentrator, and sell a copper-gold concentrate, it's very clean, very much in demand, keep it simple is my maxim."

Cobra Resources is drilling a copper-gold system showing 1.6 kilometres of mineralisation at a management-estimated 500,000 tonnes of contained copper metal, with two rigs currently mobilising.

Cabral Gold targets Q4 2026 first gold pour at Cuiú Cuiú, Brazil; the July 2025 prefeasibility study shows an IRR of 78%, NPV5 of US$73.9 million, and AISC of US$1,210/oz.

Exploration Optionality

P2 Gold is advancing the PEA-stage Gabbs gold-copper project in Nevada, ranked second globally in the Fraser Institute 2024 survey, toward a feasibility study in 2026 to 2027.

Conditions That May Undermine the Bull Case

A sustained geopolitical de-escalation compressing energy price risk premium, particularly in Brent Crude, would reduce gold's defensive bid while removing the inflation persistence underpinning the stagflation case. An unexpected economic reacceleration supported by strong labor market data and declining inflation would enable the Federal Reserve to maintain elevated rates without recession risk, lifting real yields and increasing the opportunity cost of holding gold. A weekly close below US$4,074.92/oz on a sustained basis would invalidate current technical support and signal a more significant correction toward the October 2025 lows at US$3,887/oz. These represent active falsification tests against the core thesis, to be reviewed against each major economic data release.

The Investment Thesis for Gold

- Liquidity-driven sell-offs create price dislocations without altering structural demand drivers, establishing defined re-entry points at confirmed technical support levels of US$4,074.92/oz and US$4,113.54/oz.

- Stagflation conditions constrain Federal Reserve policy flexibility and sustain gold's carry advantage relative to real yields, supporting medium-term demand independent of short-term flow dynamics.

- Producers operating below US$1,300/oz all-in sustaining cost generate margins exceeding US$3,200/oz at current spot, supporting capital returns and balance sheet strength through the consolidation phase.

- Developers holding prefeasibility-supported project economics in premier jurisdictions retain financing resilience through tighter capital market conditions, particularly where state-level permitting is already complete.

- Nevada, ranked second globally by the Fraser Institute 2024 Annual Survey of Mining Companies, reduces jurisdictional and regulatory risk for projects advancing toward construction and feasibility decisions.

- Early-stage copper-gold assets with confirmed mineralisation dimensions offer portfolio optionality within the same macro theme, providing exposure to both monetary demand and critical mineral supply constraints.

Gold's retreat to US$4,519.69/oz reflects a liquidity event that forced selling to cover cross-asset losses. This scenario has recurred across prior cycles, and in each precedent the metal recovered once liquidity conditions normalized and underlying macro drivers reasserted. The conditions sustaining gold's advance remain intact: monetary policy is constrained, central bank demand is structurally continuous, and real yields have not risen to levels that would prompt systematic institutional liquidation.

TL;DR

Gold's decline to US$4,519.69/oz is a liquidity-driven event, not a fundamental reversal. Cross-asset margin calls forced institutional selling — a pattern seen in March 2020 and 2008, both followed by recoveries once liquidity stabilized. ETF outflows of US$2.9 billion reflect short-term cash management, while COMEX net longs at 288.56 tonnes show reduced exposure without active short conviction. Stagflation conditions persist: Brent crude at US$112.57/bbl sustains sticky inflation while constraining Federal Reserve policy flexibility. Technical support holds at US$4,074.92 and US$4,113.54. Producers with sub-US$1,300/oz AISC retain margins exceeding US$3,200/oz, and developers in premier jurisdictions maintain financing resilience through the consolidation phase.

Analyst's Notes

Subscribe to Our Channel

Stay Informed