How Serabi Gold's Cost Structure Turns a Record Gold Price Into a Growth Engine

Serabi Gold turns a stable cost base and high gold prices into cash flow, funding expansion boosting capacity, and restarting growth assets ahead of 2026 output.

At a camp-style underground operation in northern Brazil, the relationship between a flat cost base and a rising gold price is generating free cash flow that finances expansion, retires debt, and now funds a shareholder return simultaneously.

Company Overview

Serabi Gold (AIM: SRB, TSX: SBI, OTCQX: SRBIF) delivered record group production of 44,200 ounces in 2025, ending the year with US$54.3 million (including US$5.1 million received in early January 2026 for December 2025 sales) in cash after funding a US$12 million exploration programme. Debt of US$7.1 million was retired in January 2026. The company's March 2026 operational update confirmed 2026 production guidance of 53,000 to 57,000 ounces. It announced the installation of a fourth ball mill at the Palito Complex in Pará State, Brazil, targeting processing capacity of 330,000 tonnes per annum before the fourth quarter of 2026. The announcement is operationally straightforward. Its significance becomes clearer when placed against the company's cost structure and the current gold price environment.

A Fixed Cost Base in a Rising Revenue Environment

The Palito Complex is an underground mining system operating in a remote area of Pará State. Both Palito and Coringa are camp operations where the company accommodates, feeds, and transports its workforce on site. Labour, power, and diesel represent the dominant share of operating costs, and each is structurally controlled in a way that distinguishes Serabi from producers whose cost bases move with commodity prices, currency fluctuations, or contractor markets.

Labour costs are governed by annual collective agreements with Brazil's national mine workers union, with percentage increases set through a nationally structured process each year. Diesel is regulated and subsidised at the federal level, insulated from the fuel volatility that affects peers in other jurisdictions. Power is transitioning further: a dedicated grid line replacing diesel generation at the Palito Complex is expected to be operational in 2026, a change projected to reduce both unit cost and carbon intensity. Serabi recorded a carbon intensity of 0.53 tonnes of carbon dioxide equivalent per ounce in 2024, against an industry average of approximately 0.90 tonnes per ounce.

The implication is direct. When gold rises, incremental revenue flows almost entirely to the margin. The cost base does not respond in kind.

What the Margin Gap Looks Like in Practice

The margin expansion is visible in reported figures. In 2024, the group reported all-in sustaining costs (AISC) of US$1,700 per ounce, compared with cash costs of US$1,326 per ounce. Through the first three quarters of 2025, AISC had moved to US$1,816 per ounce and cash costs to US$1,429 per ounce: modest increases consistent with the predictable escalation pattern described above.

The revenue picture is substantially different. Earnings before interest, taxes, depreciation, and amortisation (EBITDA) for full-year 2024 were US$35.9 million. Through the first three quarters of 2025 alone, EBITDA had already reached US$48.2 million, while post-tax profit rose from US$27.8 million for full-year 2024 to US$34.3 million over the same period, with one full quarter still to report.

Serabi closed 2025 at US$54.3 million in cash, having funded a US$12 million brownfield drilling programme across both assets during the year. That cash generation, produced at a gold price that spent significant portions of 2025 well below where gold has traded through early 2026, illustrates the operating leverage embedded in the cost structure. What Serabi is now doing is using that margin to fund structural change.

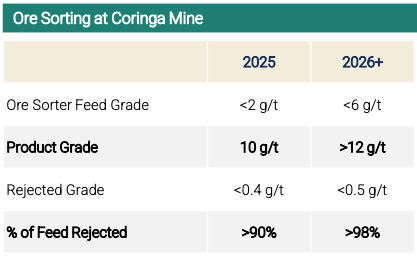

Ore Sorting as a Haulage Cost Decision

At Coringa, ore sorting has fundamentally changed the economics of the 200-kilometre road haul to the Palito processing plant.

Coringa ore exits in the mine at a feed grade of less than 2 grams per tonne. After passing through the ore sorter, more than 90% of the feed mass is rejected on site, with the product grading approximately 10 grams per tonne. What is trucked to Palito is a pre-concentrated product representing roughly 10% of the original mass. The grade improvement is a consequence of that mass rejection, not the primary objective.

As mining at Coringa transitions from selective open stoping to longhole open stoping (also referred to as sublevel open stoping), a process the company began trialling in late 2025 and is progressing through 2026, the ore sorter's role expands. The mechanised method results in greater waste dilution in the run-of-mine feed, which the sorter absorbs before haulage, preserving the transport economics even as the mining method changes.

Chief Executive Officer of Serabi Gold, Mike Hodgson, addressed the transition directly in the March 2026 operational update:

"The huge advantage of this is greater mine output, reduced mining costs, and safer operations, as sublevel open stoping is a non-entry method."

Under the longhole method, feed grade is expected to rise to less than 6 grams per tonne, with product grade projected above 12 grams per tonne and the rejection rate above 98%. Every tonne of waste rejected on site is a direct reduction in haulage cost and processing load at Palito.

The Ball Mill as a Fixed Cost Dilution Decision

The fourth ball mill installation is framed as a capacity expansion. In the context of the cost structure, it is more precisely a decision to spread a fixed cost base across more ounces. The ball mills were acquired with the Coringa asset in 2018, and rather than construct a standalone Coringa processing plant, the company elected to install one of the dormant mills at Palito, avoiding greenfield procurement costs. The capital expenditure required is the installation cost, not equipment procurement. The operation's fixed cost base does not change materially when a dormant mill is commissioned. What changes is the number of ounces produced against which those fixed costs are measured.

Hodgson framed the rationale:

"With gold prices at record highs and viable stockpiles on hand, plant capacity constraints have become more pressing than ever."

The historical cost of plant constraint is visible in the production record. The Palito Complex has consistently delivered between 30,000 and 40,000 ounces annually for approximately a decade, a range that reflects not geological limitation but processing ceiling. São Chico, the satellite mine suspended in 2023, was closed for precisely this reason. The geology was not exhausted. The plant had no capacity for ore that was viable on its own terms but marginal relative to higher-grade feed from Palito and Coringa.

Hodgson addressed the economic shift directly:

"Times have changed, and today São Chico ore, even without ore sorting, is viable."

With expanded capacity expected before the fourth quarter of 2026, São Chico is back under active review. Incremental ounces from an asset already developed, with existing underground access and no requirement for a new process plant, carry a fraction of the capital cost of new production elsewhere.

What to Watch Next

Three near-term milestones will determine whether the cost and margin story continues to develop as the company's strategy anticipates.

The updated Mineral Resource Estimate for both Palito and Coringa, expected in the first quarter of 2026, will indicate whether the 38,400 metres of drilling completed in 2025 has grown the combined inventory toward the Phase 2 target range of 1.5 to 2.0 million ounces, with 1.6 million ounces identified as a working milestone for supporting expanded throughput. Resource growth is not incidental to the cost story. Commissioning of the fourth ball mill is targeted before the fourth quarter of 2026, with the second half of the year expected to deliver stronger output than the first, and any schedule movement directly affects when the fixed-cost dilution benefit of higher throughput begins to show in reported costs per ounce.

Coringa permitting remains the external variable that the cost and margin story cannot resolve internally. The current Guia de Utilização (GUIA) licence expires on January 29, 2027, and full licence approval requires authorisation from the Instituto Nacional de Colonização e Reforma Agrária (INCRA) for a change of land use and approval of the Estudo de Componente Indígena (ECI) from the Fundação Nacional dos Povos Indígenas (FUNAI), before the Secretaria de Estado de Meio Ambiente e Sustentabilidade (SEMAS), the state environmental agency, can issue the full mining licence (LI). Management has targeted INCRA approval in the first half of 2026 and describes the FUNAI process as progressing through consultation with the indigenous community. Without the full licence, the ceiling on Coringa's long-term production contribution remains in place, and with it the ceiling on how far the fixed cost base can ultimately be diluted across a larger group output.

FAQs (AI-Generated)

Labour is governed by annual collective agreements with Brazil's national mine workers union, diesel is regulated and subsidised at the federal level, and power is transitioning to a dedicated grid line in 2026. These inputs are structurally controlled rather than exposed to global commodity prices or contractor market rates.

Cash costs cover direct mining and processing expenses, while all-in sustaining costs (AISC) add sustaining capital, royalties, and allocated corporate costs on a per-ounce basis. Serabi reported cash costs of US$1,326 per ounce and AISC of US$1,700 per ounce for 2024.

The ore sorter rejects more than 90% of run-of-mine mass on site before the 200-kilometre haul to Palito, reducing haulage cost and processing load per ounce recovered. As Coringa transitions to longhole stoping, the rejection rate is projected to exceed 98% at an improved product grade.

São Chico was suspended in 2023 because limited processing capacity at Palito forced prioritisation of higher-grade feed, not because the deposit was depleted. With additional capacity from the fourth ball mill and a higher gold price environment, previously marginal ore is now being reassessed for economic viability.

The fourth ball mill increases processing throughput without materially increasing the fixed cost base, allowing more ounces to be produced from the same infrastructure. As output rises toward the 330,000 tonnes per annum target, fixed costs are spread across a larger production base, reducing unit costs per ounce. This effect becomes more visible once the mill is fully commissioned and operating at sustained capacity levels.

Analyst's Notes

Subscribe to Our Channel

.jpg)

%20(1).jpg)

.jpg)

Stay Informed