India's Gold Import Duty Hike Cuts Demand 50-60 Tonnes & Shifts Investor Focus to Project Execution

India's 15% gold import duty could cut demand by 50-60 tonnes, shifting investor focus toward project execution, permitting, and resource growth.

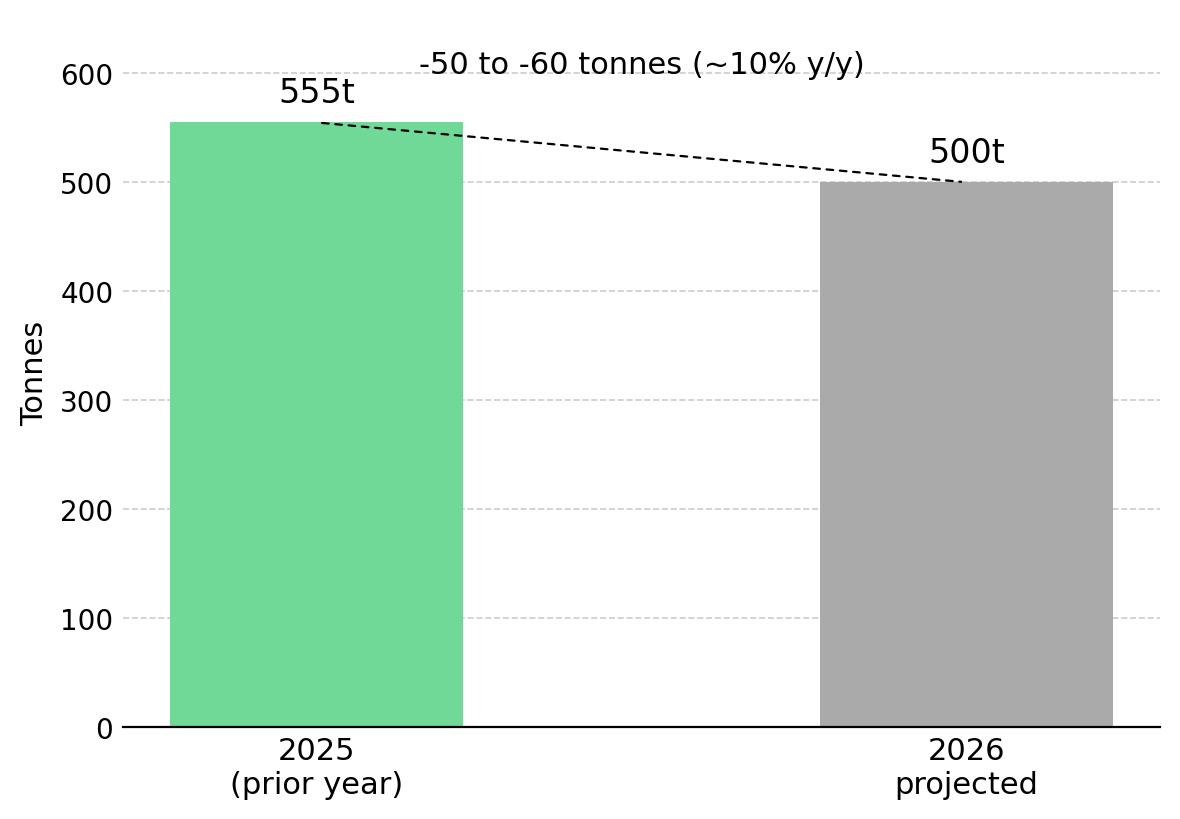

- India raised its gold import duty from 6% to 15% in May 2026, and the World Gold Council projects the increase will reduce 2026 jewellery and bar-and-coin demand by 50 to 60 tonnes, or roughly 10% year on year.

- Major Indian mutual fund houses imposed temporary limits on large Gold Exchange Traded Fund investments, signalling weaker retail demand following the duty increase and gold price rally.

- Global gold investment demand fell 17% week on week to US$15.28 billion, while India recorded its first month of net Exchange Traded Fund outflows in the past year.

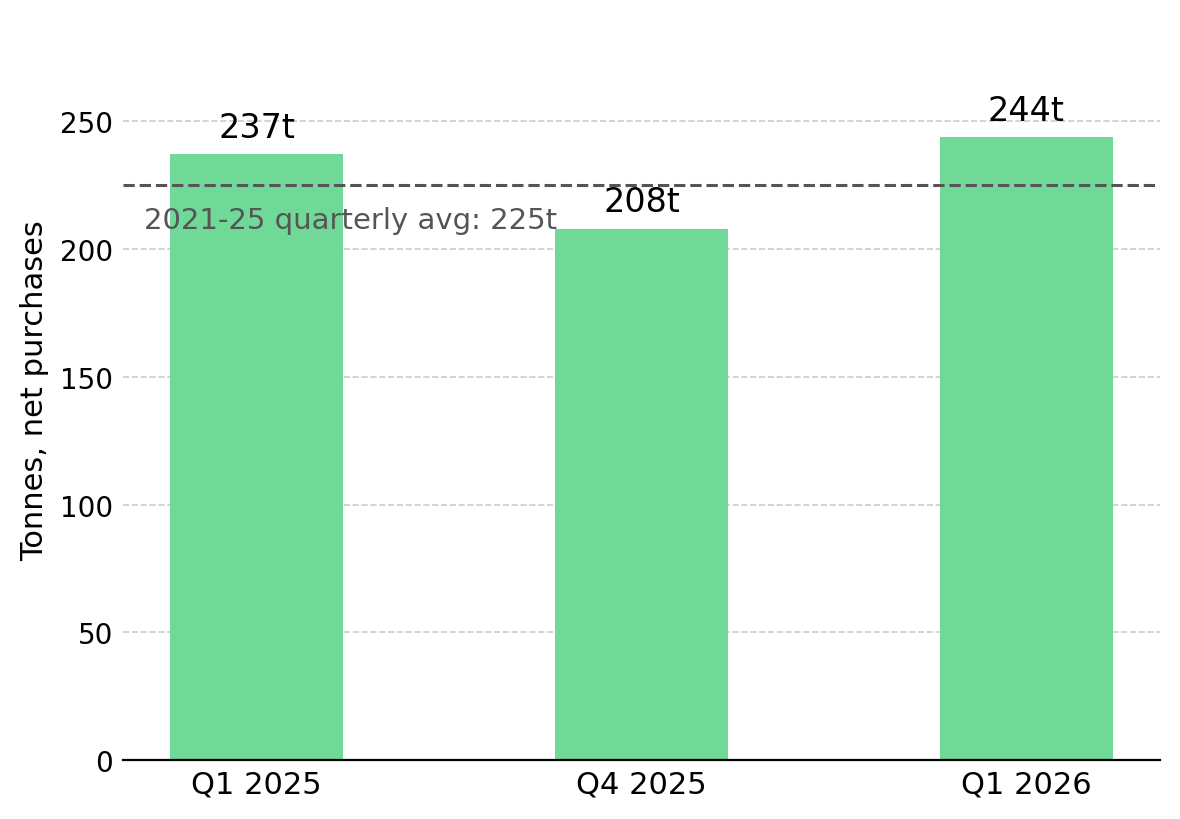

- Central banks bought 244 tonnes of gold in the first quarter of 2026 while Asian retail demand weakened, increasing the relative appeal of developers with near-term production catalysts and low-cost projects in Tier-1 jurisdictions.

- Gold developers with near-term production catalysts offer more direct exposure to cash flow generation, while earlier-stage projects provide longer-term leverage to resource growth and project advancement.

Weaker Indian Demand Shifts Attention to Institutional Flows

In May 2026, India raised its basic customs duty on gold imports from 6% to 15%, increasing the cost of imported gold by nine percentage points. India implemented the increase after the rupee fell more than 7% year to date, targeting gold imports to reduce pressure on foreign exchange reserves.

Domestic gold prices have not yet fully reflected the higher duty because inventory imported at the previous 6% rate remains in the supply chain. As a result, the World Gold Council's projected 50 to 60 tonne reduction in 2026 demand is not yet visible in current trade data. For investors, weaker Indian demand may become more visible as higher-duty inventory replaces existing stock.

India and China have historically accounted for roughly half of global gold demand across jewellery, bar-and-coin investment, and Exchange Traded Fund flows. A decline in Indian demand increases the relative importance of central bank buying and Western institutional investment, favouring developers with near-term production and strong project economics.

Central Banks Buy 244 Tonnes as Indian Demand Weakens

Central bank buying remained strong despite weaker Indian demand. According to the World Gold Council, central banks purchased 244 tonnes of gold in the first quarter of 2026, exceeding both the previous quarter and the five-year average. Poland added 31 tonnes during the quarter as part of its stated objective to increase gold reserves to 700 tonnes, while Uzbekistan added 25 tonnes, increasing gold to approximately 87% of its total reserves.

Unlike jewellery demand and ETF flows, central bank purchases are typically driven by reserve management objectives rather than short-term price movements. For investors, official-sector demand can offset weaker retail demand, supporting gold prices and reducing reliance on any single consumer market.

Gold Investment Demand Falls 17% as Indian ETF Flows Reverse

Several of India's largest mutual fund houses, including HDFC, ICICI Prudential, Tata, and Nippon India, imposed temporary limits on large Gold ETF investments following the duty increase. The restrictions followed a gold price rally and accelerated profit-taking among Indian investors.

Global gold investment demand fell 17% to US$15.28 billion from US$18.46 billion, while India recorded its first month of net ETF outflows in the past year after generating inflows through much of 2025 and early 2026.

Asian retail and ETF flows respond more quickly to price and policy changes than central bank buying and Western institutional allocations. As a result, gold equity valuations are more likely to be supported by long-term capital flows than short-term shifts in retail demand.

Execution-Driven Developers Gain Valuation Support

Developers targeting near-term production provide a clearer execution-driven investment case than companies dependent on changes in regional demand. Cabral Gold's Phase 1 gold-in-oxide heap leach operation is targeting commercial production in the fourth quarter of 2026, while recent infill drilling, including 25 meters at 7.47 grams per tonne gold from surface, supports resource conversion ahead of production. The project's value depends primarily on converting resources into production and cash flow rather than changes in Indian jewellery demand. Alan Carter, President and Chief Executive Officer of Cabral Gold, describes how initial cash flow could fund district growth:

"We are building an initial gold-in-oxide heap leach project which should mine about 3,000 tonnes a day. That will provide a significant amount of cash to allow us to develop the larger district, explore the larger district, grow the global resource base within the Cuiú Cuiú district, and ultimately allow us to demonstrate the economic viability of the much larger phase two project."

Projects capable of funding future growth internally reduce reliance on external capital during periods of demand uncertainty. New Found Gold's Hammerdown project is targeting commercial production in the second half of 2026, with mill throughput already exceeding its 700-tonne-per-day design rate. Hammerdown's projected US$40-50 million in annual free cash flow is expected to fund corporate overhead and exploration at Queensway, reducing reliance on future equity financing. Keith Boyle, Chief Executive Officer of New Found Gold, discusses the company's funding position:

"We've got 185 million dollars in funding available to advance the Queensway project. Our PEA capex was 155 million dollars, and so we are fully funded to advance Queensway through to production."

Permitting & Infrastructure Strengthen Project Economics

Tier-1 mining jurisdictions can reduce project risk through established permitting frameworks and existing infrastructure. Hycroft Mining Holding Corporation's June 2026 S-K 1300 Technical Report Summary reported a post-tax net present value of US$4.3 billion at a base case of US$3,600 per ounce gold and US$48 per ounce silver, rising to US$10.0 billion at spot prices across a 51-year mine life. Hycroft's existing crushing circuits, heap leach pads, and Merrill-Crowe processing facilities reduce initial capital requirements relative to a comparable greenfield project.

Projects that have completed major permitting milestones face fewer development risks and financing uncertainties. U.S. Gold Corp's CK Gold project reported an after-tax net present value of US$632 million and an internal rate of return of 27% at a base case gold price of US$3,250 per ounce, while remaining net present value positive at US$2,000 per ounce. With its major permits secured and access road construction underway, CK Gold's remaining catalysts are financing-related rather than regulatory. Luke Norman, Chairman of U.S. Gold Corp, discusses the financing options for CK Gold:

"The permits that are awarded to us are not reversible or revocable, we're ready to go, and we have seen indicative term sheets of as high as 80% debt with 20% equity, with equity showing at premiums to market."

Resource Expansion Drives Long-Term Gold Equity Value

Earlier-stage developers offer greater leverage to resource growth but depend more heavily on exploration success. Tudor Gold's 2026 drill program at Treaty Creek is focused on expanding the resource beyond the 24.9 million ounce indicated Goldstorm deposit, with future value tied to drilling results and completion of a preliminary economic assessment. Joe Ovsenek, President and Chief Executive Officer of Tudor Gold, discusses the scale of the higher-grade opportunity at Treaty Creek:

"At the US$175 per tonne NSR cutoff, we still have 3.4 million ounces of gold in the indicated category and 2.4 million ounces in the inferred category. The indicated resource grades 2.33 grams per tonne gold and the inferred resource grades 4.02 grams per tonne gold."

Multi-commodity projects can provide gold exposure alongside broader resource growth opportunities. At Cobra Resources' Manna Hill project, recent drilling returned 74 meters at more than 1% copper and approximately 0.25 grams per tonne gold, alongside 84 meters at 0.6% copper and 0.14 grams per tonne gold, supporting efforts to define a multi-million tonne porphyry system.

The key consideration is that gold remains an important component of the Manna Hill system. As drilling expands the scale of the porphyry system, the associated gold inventory could also grow, providing additional leverage to a supportive gold price environment. This makes resource definition and project advancement more important to valuation than short-term changes in regional gold demand.

Exploration Success Could Expand Future Project Scale

Exploration-stage projects can create value through resource growth and the conversion of exploration success into larger future development opportunities. P2 Gold's Gabbs project continues to advance drilling across the Lucky Strike and Sullivan zones, with both areas remaining open for expansion and an updated mineral resource estimate targeted for the third quarter of 2026. Ongoing drilling results and resource growth could support a larger future operation as the project advances toward a feasibility study. Joe Ovsenek, President and Chief Executive Officer of P2 Gold, outlines the production growth potential being evaluated at Gabbs:

"It was a 9-million-ton-per-year mine producing roughly 110,000 ounces of gold per year. We're looking at studies now that could increase that to 12 million tons a year because we'd like to get closer to 150,000 ounces of gold a year."

Milestones Matter More Than Regional Demand Trends

With Indian demand weakening and central bank buying remaining uneven, companies with near-term paths to production offer the clearest gold equity catalysts. For these companies, valuation depends more on execution, including grade delivery, cost control, and resource conversion, than on short-term shifts in retail demand. As demand trends become less predictable, execution becomes a more important driver of near-term valuation.

Projects approaching production are typically evaluated against measurable milestones such as permitting progress, construction schedules, throughput targets, and resource conversion. These milestones influence valuation because they determine when revenue generation begins and whether project targets are achieved.

The Investment Thesis for Gold

- India's import duty increase highlights the importance of project execution, jurisdiction, permitting, and cost structure when evaluating gold equities.

- Companies generating cash flow from production are less exposed to regional demand fluctuations than earlier-stage projects, even as India's projected 50 to 60 tonne reduction in gold demand affects the 2026 market outlook.

- Projects in Nevada and Wyoming remain economically viable at gold prices well below current spot levels, with at least one project maintaining a positive net present value at US$2,000 per ounce.

- Fully permitted projects with existing infrastructure face fewer regulatory delays, making financing timelines more predictable and potentially improving financing terms.

- Infill drilling ahead of production decisions can create near-term valuation catalysts driven by company execution rather than regional demand trends.

- Multi-commodity projects and district-scale exploration offer longer-term exposure to gold through resource growth, exploration success, and project advancement.

- Developers and explorers offer different combinations of execution risk and commodity price exposure, and investors should allocate capital accordingly.

India's gold import duty increase is a useful reminder that gold demand is not a single, undifferentiated number. The World Gold Council projects the duty increase will reduce Indian jewellery, bar, and coin demand by 50 to 60 tonnes in 2026, but central banks purchased 244 tonnes of gold in the first quarter alone, illustrating how different demand channels can move in opposite directions. For equity investors, this means valuation depends not only on the gold price but also on company-specific milestones such as feasibility studies, permitting decisions, resource conversion, and financing. Companies that advance these milestones can reduce execution risk and improve valuation regardless of whether demand growth comes from Indian consumers, central banks, or institutional investors.

TL;DR

India's decision to raise its gold import duty from 6% to 15% is expected to reduce 2026 gold demand by 50-60 tonnes, weakening one of the world's largest sources of retail consumption. However, central banks purchased 244 tonnes of gold in the first quarter of 2026, helping offset softer retail demand. The article argues that gold equity investors should focus less on short-term demand shifts and more on company-specific catalysts such as permitting, financing, feasibility studies, resource conversion, and project advancement. Developers approaching key milestones may offer clearer valuation catalysts, while earlier-stage companies provide longer-term exposure to resource growth and exploration success.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed