Smart Money's Gold Mining Play: Why Miners Beat Bullion

Gold mining stocks offer leveraged exposure to rising gold prices through companies with strong cash flow, Tier-1 jurisdiction operations, and disciplined capital allocation strategies.

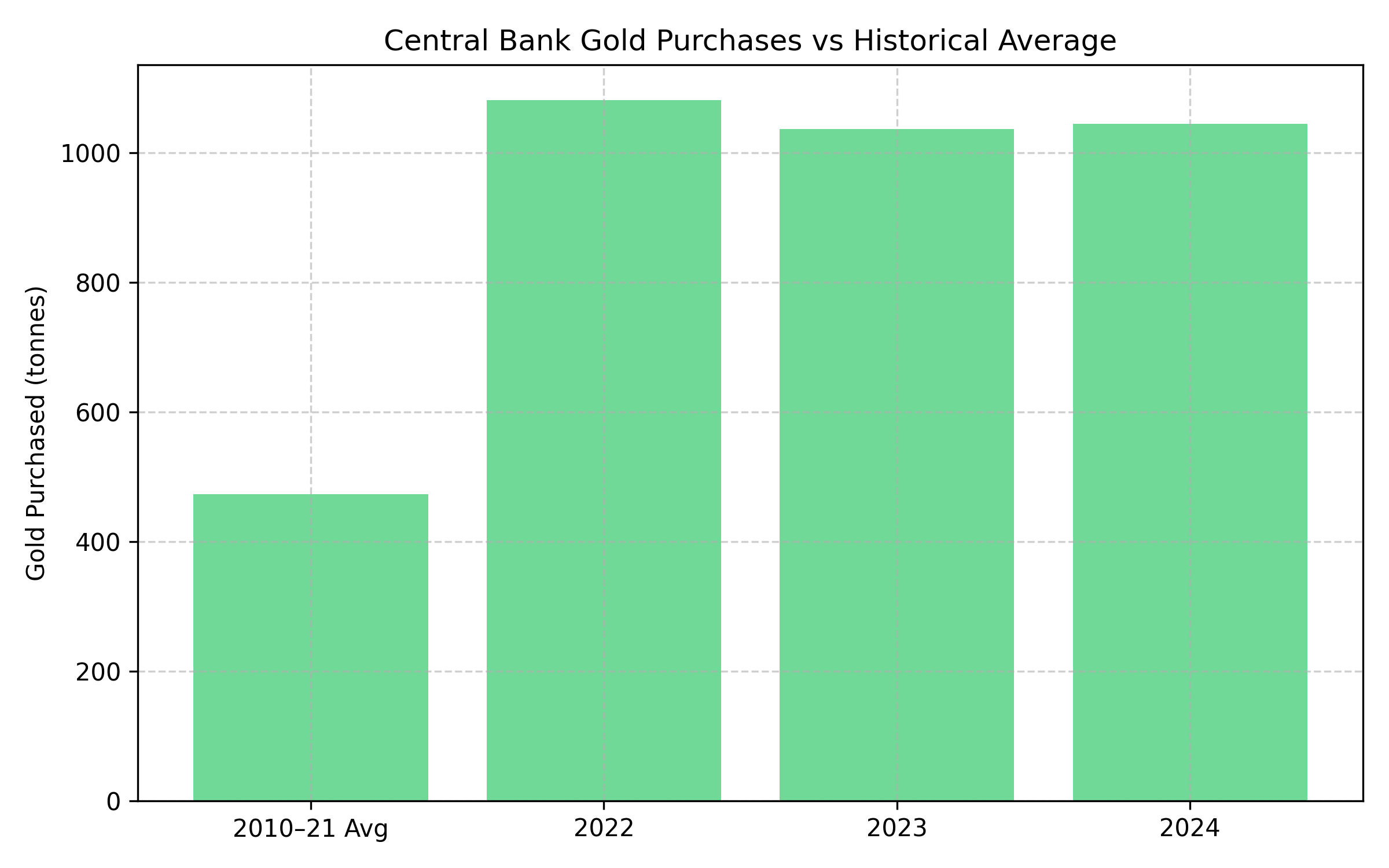

- Central banks purchased 1,037 tonnes in 2023 and 1,045 tonnes in 2024, following a record 1,082 tonnes in 2022 (World Gold Council), representing three consecutive years above 1,000 tonnes and far exceeding the 473 tonne annual average from 2010-2021, providing unprecedented institutional support for gold prices.

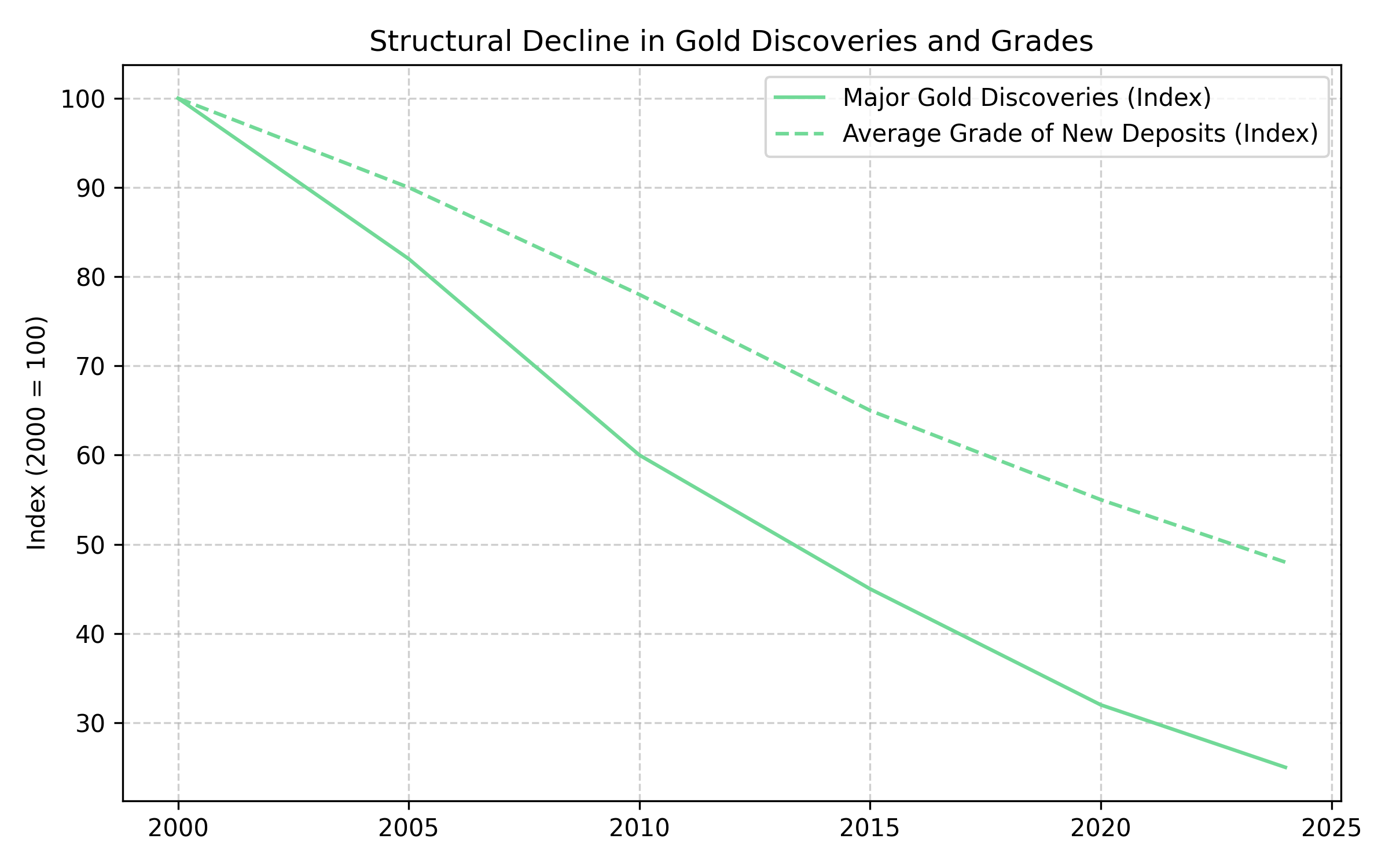

- Major gold discoveries have declined precipitously over two decades with average grades falling consistently, while easy to find, high grade deposits have been largely exhausted, forcing producers toward increasingly complex geological environments and creating structural supply challenges that favor existing producers.

- Companies operating exclusively in Tier 1 jurisdictions (US, Canada, Australia) trade at substantial premiums reflecting political stability, regulatory predictability, and ESG compliance, with this premium widening as institutional investors increasingly prioritize operational security over pure resource scale.

- Leading companies like Cabral Gold (78% IRR, $75M annual cash flow by Q4 2026), Integra Resources (70,927 oz production funding $60M reinvestment), and i-80 Gold (targeting 600,000 oz annually) demonstrate how operational excellence and capital allocation discipline create sustainable competitive advantages over growth at any cost strategies.

- Modern mining technology including ore sorting, automated processing, and improved metallurgy (exemplified by i-80 Gold's autoclave facility increasing recovery from 55-60% to 92%) enables economic extraction from previously unviable deposits while companies controlling processing infrastructure enjoy cost advantages and scheduling flexibility during volatile markets.

Why Smart Money Is Buying Gold Mining Stocks: The Case for Leveraged Precious Metals Exposure in 2026

The gold mining sector stands at an inflection point that hasn't been seen in decades. With central banks accumulating bullion at record rates, supply constraints tightening across major producing regions, and mining companies demonstrating unprecedented capital discipline, the investment case for quality gold miners has rarely been more compelling.

Unlike the speculative frenzies of previous cycles, today's gold mining investment thesis rests on fundamental supply demand dynamics and operational excellence rather than hope and hype. The companies emerging as winners are those that have learned hard lessons from past boom bust cycles, prioritizing cash flow generation, jurisdictional quality, and measured growth over aggressive expansion.

Global Gold Market Dynamics: A Perfect Storm for Mining Equity Outperformance

Central banks purchased 1,037 tonnes in 2023 and 1,045 tonnes in 2024, following a record 1,082 tonnes in 2022 (World Gold Council), driven by currency diversification strategies and geopolitical risk management. This institutional buying provides a price floor that didn't exist during previous gold rallies, creating a more stable environment for mining company planning and investment. The three year total of 3,164 tonnes represents the third consecutive year demand surpassed 1,000 tonnes, far exceeding the 473 tonne annual average between 2010-2021.

Gold's supply side faces challenges that extend far beyond typical mining cycles. Major discoveries have declined precipitously over the past two decades, with the average grade of new deposits falling consistently. The easy to find, high grade deposits that built the industry have largely been exhausted, forcing producers toward increasingly complex geological environments.

Modern mining technology is enabling the economic extraction of gold from deposits that would have been uneconomical just a decade ago. Ore sorting technology, automated processing systems, and improved metallurgical techniques are expanding the universe of mineable resources while reducing environmental footprints.

The Jurisdictional Quality Premium: Why Geography Matters More Than Ever

The concentration of quality gold mining assets in stable jurisdictions has created a scarcity premium that continues to widen. Companies operating exclusively in the United States, Canada, and Australia trade at substantial premiums to their resource bases compared to peers with exposure to higher risk regions.

This premium reflects not just political stability, but also regulatory predictability, established permitting frameworks, and access to capital markets. In an environment where ESG considerations increasingly drive institutional investment decisions, jurisdictional quality has become a key differentiator.

Company Case Studies: Brazilian District Scale Development: Cabral Gold

Cabral Gold represents disciplined development in Brazil's prolific Tapajós region, demonstrating how strategic financing eliminates dilution risk while building toward district scale production. The company secured $45M in non-dilutive financing delivering 78% IRR and $75M annual cash flow by Q4 2026, with all-in costs of $1,210/oz providing $1,400+ margins. Carter noted that with $75 million in annual free cash flow, "it opens all sorts of doors" for exploration funding.

Alan Carter, the President and CEO commented operations:

"We are delighted with the results from the Updated PFS on the Oxide Starter Operation at Cuiú Cuiú, which reflects the dedication of our team and consulting advisors".

Historical placer gold production at Cuiú Cuiú was 10 times greater than Tocantinzinho (Brazil's third-largest gold mine), providing a district scale opportunity funded by near term cash flow generation.

Nevada's Emerging Mid Tier Producer: Integra Resources

Integra Resources exemplifies the cash flow discipline model, operating the Florida Canyon mine while advancing two significant development projects without shareholder dilution. George Salamis, President, CEO and Director commented their cash flow:

"2025 marked a pivotal year for Integra as the Company successfully completed its first full year of production at Florida Canyon, while executing a deliberate and capital-intensive reinvestment strategy".

The DeLamar project demonstrates Nevada development potential, with total production of 1.1 million ounces over a 10-year operating mine life, generating an after-tax NPV of approximately $774 million with 46% IRR at base case prices. The project's selection for the FAST 41 permitting program reduces development timeline risk.

Nevada Scale & Processing Control: i-80 Gold

i-80 Gold represents the ultimate Nevada consolidation play, controlling 14 million ounces of gold resources across five projects and one of only two autoclave processing facilities in the state.

Tyler Hill, Vice President Geology mentioned their processing control:

"The 2025 infill drilling results at Granite Creek Underground successfully support our geological model, confirming the continuity and high-grade nature of the deposit."

The processing advantage provides substantial value creation, as the autoclave facility will increase payability on refractory material from 55-60% to approximately 92% recovery when commissioned. With 6.5Moz in Measured & Indicated resources and a production target of 600,000 ounces annually by the early 2030s, i-80 Gold is positioned to become Nevada's second-largest gold producer.

Golden Triangle Scale & Discovery: Tudor Gold

Tudor Gold's Treaty Creek project represents one of the largest undeveloped gold resources in North America.

Joe Ovsenek, President and CEO commented on their discovery:

"The 2026 MRE increased Indicated Mineral Resources of gold at Treaty Creek's Goldstorm Deposit by 15% over the 2024 Mineral Resource estimate."

The updated resource contains 24.9 million ounces of gold, 148.7 million ounces of silver and 3.048 billion pounds of copper.

The company's strategic focus targets higher grade underground mining potential, with recent financings totaling approximately $24.5 million funding development of what Ovsenek describes as "the most straightforward, economically attractive development path to gold production at Treaty Creek."

Nevada Large Scale Gold Development: Hycroft Mining

Hycroft Mining controls one of the world's largest undeveloped gold deposits in Nevada's Tier 1 mining jurisdiction, with a massive 64,000-acre land package representing significant untapped potential. The company is transitioning from historical oxide heap leach operations to unlocking the much larger sulfide ore resource through advanced processing technology.

CEO Diane Garrett emphasized their transition:

"Vortex and Brimstone are emerging as two high-grade silver systems of significant size and consistency -- an evolution that is fundamentally reshaping Hycroft's value proposition."

With these discoveries supporting the broader gold development strategy. The combination of massive scale, established infrastructure, and transition to higher recovery processing positions Hycroft as a potential major Nevada gold producer.

Diversified Portfolio Opportunities: New Found Gold's Canadian Transformation Play

New Found Gold exemplifies successful transformation from exploration to production in Newfoundland, completing its evolution into an emerging Canadian gold producer through strategic acquisitions and operational advancement. Keith Boyle, CEO stated their opportunities:

"Commencing EPCM work is a key milestone in advancing Queensway. We believe our rapid timeline from initial mineral resource in early 2025 to a planned first gold pour in late 2027 is supported by a unique combination of factors."

The company controls multiple assets in Newfoundland and Labrador, including the producing Hammerdown operation and the flagship Queensway development project. The strategic transformation includes completion of a C$63M bought deal financing and C$20M private placement, strengthening the balance sheet while advancing toward the targeted production timeline.

Multi-Jurisdiction African Producer: Perseus Mining

Perseus Mining represents the multi jurisdictional African gold producer model, operating three producing mines across Ghana, Côte d'Ivoire, and Tanzania while building a fourth project. The company projects annual output between 515,000 and 535,000 ounces from 2026 through 2030, establishing it among the world's better performing mid tier gold producers. Craig Jones, the new Managing Director and CEO, brings extensive operational experience from Newcrest Mining to lead the next phase of expansion. Perseus has demonstrated consistent delivery against production and cost guidance while generating substantial operating cash flow in a strong gold price environment.

Brazilian Underground Specialist: Serabi Gold

Serabi Gold has achieved a remarkable transformation from capital constrained explorer to cash generating underground producer, tripling its share price from £0.60 to £2.40 while building toward 60,000 ounce annual production.

CEO Mike Hodgson stated being the underground specialist:

"We are very pleased with the performance of the Palito Complex and Coringa Mine during the fourth quarter, concluding yet another positive year with many milestones achieved for Serabi."

The company delivered record annual production of approximately 44,000 ounces in 2025, setting 2026 guidance at 53,000-57,000 ounces.

Canadian High-Grade Restart: West Red Lake Gold Mines

West Red Lake Gold Mines achieved a major milestone with commercial production at the Madsen mine as of January 1, 2026, marking the successful restart of one of Canada's high grade underground operations.

Shane Williams, President and CEO stated their high-grade restart:

"We are delighted to announce commercial production at the Madsen Mine, achieved only seven months after completion of the bulk sample."

The operation averaged 689 tonnes per day in December 2025, representing 86% of permitted throughput, with strong mill recoveries of 94.6% enabling production of 3,215 ounces of gold.

US Permitted Development: U.S. Gold Corp

U.S. Gold Corp represents the rare combination of a fully permitted, shovel ready gold copper project with institutional backing and an 18 month timeline to production. Luke Norman, Executive Chairman, outlined the strategic importance of recent developments:

"2026 is a whole new kind of turning point for us. Definitive feasibility is going to set the pathway immediately to project finance."

The company completed a $31.2 million financing with institutional validation from major funds including VanEck, Goehring & Rozencwajg, and Libra Capital, marking the first significant institutional capital raise during the current bull cycle.

Investment Strategies: Positioning for Different Market Scenarios

Established producers with consistent operating cash flow offer exposure to gold price appreciation while providing income through dividend payments. These companies typically trade at premiums to development stage assets, reflecting reduced execution risk and immediate cash generation capability.

Companies advancing high quality development projects offer leveraged exposure to gold price appreciation, though with higher execution risk. Near term producers companies within 12 24 months of first production often provide optimal risk adjusted returns for investors seeking leveraged gold exposure.

Regional consolidation strategies create substantial value through infrastructure sharing, operational efficiencies, and reduced administrative costs. The most successful consolidators focus on specific geological settings where they have developed operational expertise and competitive advantages.

Gold mining remains inherently risky, with operational challenges that can significantly impact financial performance. Investors can mitigate risks by focusing on companies with diversified asset bases, strong technical teams, and proven track records. Portfolio diversification across different company stages and geographical regions helps manage volatility.

The Investment Thesis for Best Gold Mining Stocks

- Focus on companies with consistent operating cash flow that can fund growth internally while returning capital to shareholders through dividends and buybacks.

- Pay premiums for companies operating exclusively in Tier 1 jurisdictions (US, Canada, Australia) as political and regulatory risks increasingly drive valuation differentials.

- Companies owning processing facilities and regional infrastructure enjoy cost advantages and scheduling flexibility that become more valuable during volatile markets.

- Allocate capital across producing miners, near term developers, and quality exploration plays to capture different types of leverage to sustained higher gold prices.

- Underground mines typically offer superior unit economics, longer mine lives, and lower environmental impacts compared to large scale open pit operations.

- Companies with net cash positions and minimal debt can pursue growth opportunities without shareholder dilution, particularly valuable during periods of capital market volatility.

The gold mining investment landscape has fundamentally shifted toward operational excellence, capital discipline, and jurisdictional quality. Successful investing requires understanding that today's winners generate consistent cash flow, operate in stable jurisdictions, and maintain strong balance sheets rather than pursuing growth at any cost. The combination of supply constraints, central bank demand, and improved operational efficiency creates a compelling environment for quality gold mining investments.

TL;DR

Central banks purchased over 1,000 tonnes annually (2022-2024) creating unprecedented price support, while supply constraints from declining discoveries favor quality miners in Tier 1 jurisdictions who prioritize cash flow discipline over growth-at-any-cost, with companies like Cabral Gold (78% IRR) and i-80 Gold demonstrating operational excellence through strategic financing and processing control.

FAQs (AI-Generated)

Central banks purchased over 1,000 tonnes annually for three consecutive years (2022-2024) driven by currency diversification and geopolitical risk, creating an institutional price floor that provides mining companies with more stable revenue planning and supports premium valuations for quality producers.

Tier 1 jurisdictions (US, Canada, Australia) offer political stability, regulatory predictability, and ESG compliance that commands substantial market premiums as institutional investors prioritize operational security over pure resource scale.

Look for companies that generate consistent operating cash flow, fund growth internally without excessive dilution, maintain minimal debt, and return capital to shareholders rather than pursuing growth at any cost.

Underground operations offer superior unit economics through selective mining of higher-grade ore, longer mine lives, greater production flexibility, and lower environmental impacts with smaller surface footprints.

Focus on established cash flow producers for stable prices, diversify across development stages for rising prices, and prioritize companies with processing control and strong balance sheets for volatile markets while always emphasizing jurisdictional quality.

Analyst's Notes

Subscribe to Our Channel

.jpg)

%20(1).jpg)

.jpg)

Stay Informed